Disclaimer: This article discusses various aspects of Real-World Asset (RWA) tokenization, including the involvement of major financial institutions, the integration of blockchain technology, and the potential benefits and challenges. It is important to note that the legislative and regulatory landscape surrounding RWA tokenization is rapidly evolving. Current laws and regulations are still being shaped, and future developments may significantly impact the theses and outcomes discussed herein. The information provided in this article is based on the current understanding and state of the market as of the date of publication. Readers are advised to stay informed about ongoing legislative changes and consult with legal and financial experts when considering investments in tokenized assets.

RWA Tokenization involves converting tangible assets like cash, equity, bonds, loans, real estate, commodities or fine art into digital tokens on a blockchain, making them more accessible, liquid and transparent. The concept has recently gained significant traction, offering a bridge between traditional financial instruments and the world of digital assets.

We previously covered the topic of Tokenized Real Estate. This segment was mostly dormant throughout the second half of 2023. RWA tokenization has faced many false starts due to technical, regulatory and market challenges. As a result, real estate tokenization has now become a smaller segment within the broader RWA market.

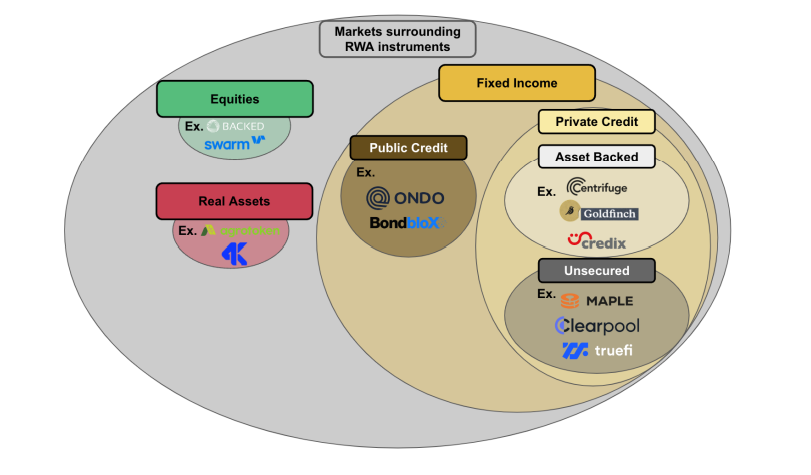

RWAs, however, became the second biggest digital asset narrative in Q2 2024, accounting for 11% of web traffic among narratives tracked by CoinGecko. The industry now represents a rich and diverse landscape, encompassing a variety of markets and including stakeholders from both Decentralised Finance (DeFi) and Traditional Finance (TradFi).

Source: Binance Research, Real World Assets: The Bridge Between TradFi and DeFi

In this article, we explore the latest trends in RWA tokenization and highlight successful pilot projects that define the state of RWA in Q2 2024. We will also summarize the current narratives around the RWA market and look at possible future waves of tokenization.

Increased Institutional Participation Nudges the Dormant Market

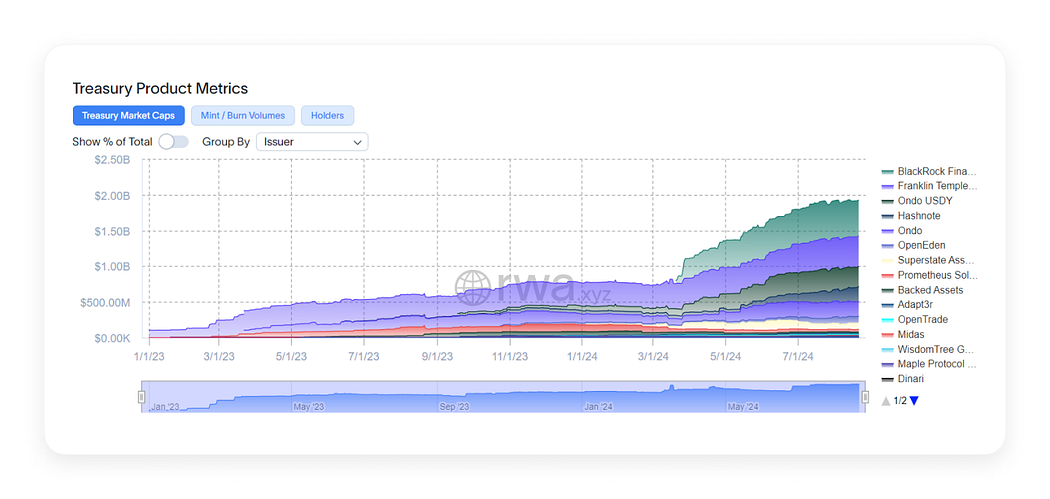

Several major financial institutions made their first strategic moves into RWAs in 2024. The increased attention devoted to RWA tokenization likely followed successful pilot initiatives launched by giants of traditional finance such as BlackRock and Franklin Templeton as well as leading DeFi players like Ondo Finance.

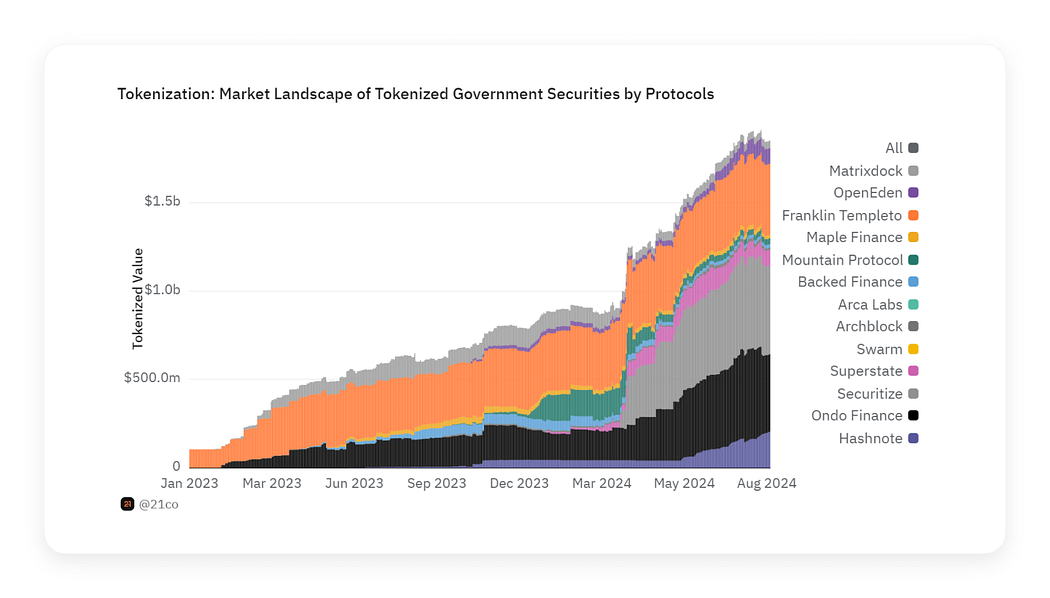

Source: RWA.xyz. Accessed on August 22, 2024.

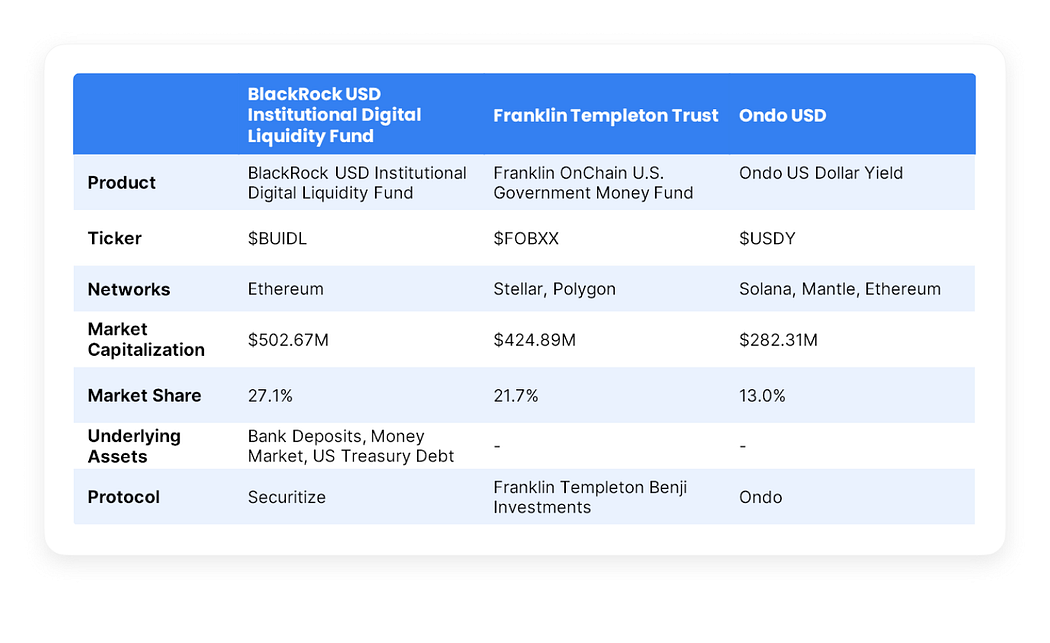

BlackRock, Franklin Templeton and Ondo’s own tokenized financial products account for more than 60% of the total market capitalization of tokenized government securities:

Source: RWA.xyz, Dune.com. Accessed on August 22, 2024.

BlackRock’s BUIDL, officially known as the BlackRock USD Institutional Digital Liquidity Fund, is a tokenized fund on the Ethereum network launched on March 20, 2024. The BUIDL fund is backed by a mix of cash, U.S. Treasury bills, and repurchase agreements, and is designed to provide qualified investors with the opportunity to earn U.S. dollar yields by subscribing to the fund through blockchain technology.

As of July 2024, BUIDL grew to become the largest tokenized treasury fund, surpassing $500 million in assets under management.

Three projects participating in BUIDL are among the top Tokenized Government Securities Protocols (Ondo Finance, Securitize, Maple Finance). Source: Dune.com. Accessed on August 22, 2024.

Several blockchain projects contributed to the success of BUIDL. Securitize played a role in compliance and investor management, ensuring the tokenized products met regulatory standards. Maple Finance offered an on-chain credit marketplace, facilitating the creation and trading of credit products. Swarm Markets, a licensed DeFi platform, facilitated the tokenization and trading of RWAs within a regulated framework. Boson Protocol enabled BlackRock to explore new avenues for tokenizing and trading RWAs through a blockchain-based e-commerce market. Polytrade provided a marketplace for managing RWAs, supporting the democratization of investment opportunities and improving asset liquidity. Finally, Ondo Finance, an issuer of OUSG, a tokenized short-term U.S. Treasuries fund, deployed the majority of its assets on BUIDL, contributing to its utility for traditional investors (BeInCrypto) (CoinDesk) (CoinMarketCap) (The Defiant).

Franklin Templeton’s tokenization project, known as the Franklin OnChain U.S. Government Money Fund (FOBXX) is another example of integration between traditional finance and DeFi. Launched in 2021, this fund is the first US-registered mutual fund to use blockchain for processing transactions and recording share ownership. The project leverages the Stellar and Polygon blockchains to support the BENJI token, which represents shares of the FOBXX fund. This initiative allows peer-to-peer transfer of tokenized shares and aims to provide steady yields to investors, enhancing the liquidity and accessibility of U.S. government money funds. Franklin Templeton developed this project in-house but collaborates with blockchain networks to implement the technology (Franklin Templeton, BeInCrypto).

Franklin Templeton’s RWA strategy differs from that of BlackRock, which primarily relies on partnerships with existing blockchain projects. While BlackRock’s BUIDL focuses on integrating various DeFi platforms to tokenize U.S. Treasury bills and other fixed-income products, Franklin Templeton’s approach centers on leveraging public blockchains to enhance the transparency and efficiency of traditional money market funds.

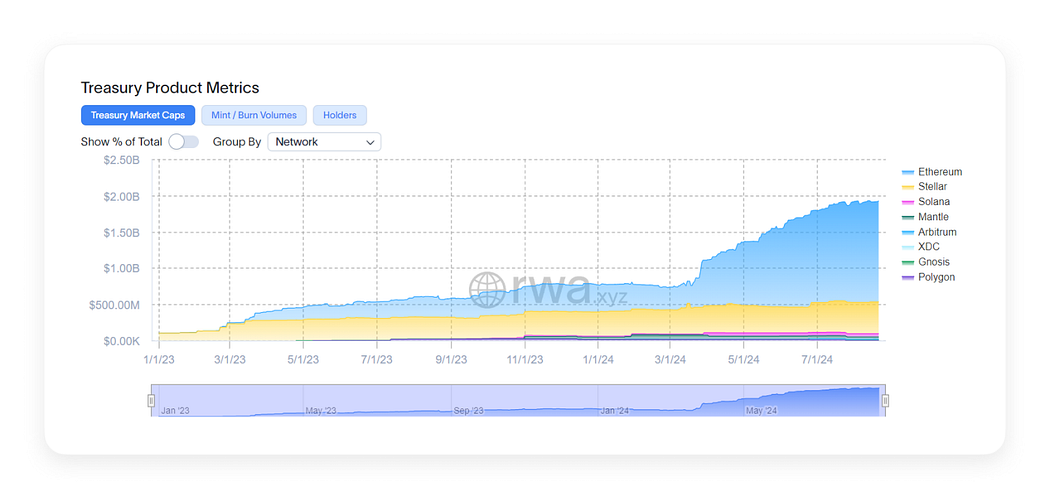

More than 90% of the market capitalization of tokenized U.S. Treasury assets comes from Ethereum and Stellar. Source: RWA.xyz. Accessed on August 22, 2024.

Ondo Finance is an example of a successful non-institutional tokenized U.S. Treasury asset issuer. Ondo Finance’s USDY project, launched in late 2023, is designed as a yield-bearing stablecoin backed by U.S. Treasuries and bank deposits. USDY represents a stable and interest-bearing digital asset, offering yields to its holders through the integration with traditional financial instruments. Unlike typical stablecoins, USDY generates yield from the underlying U.S. Treasury assets, making it an attractive option for both DeFi users and institutional investors seeking stable returns.

Ondo Finance’s Short-Term US Government Bond Fund (OUSG) represents tokenized short-term U.S. Treasury bills and complements USDY by providing a secure and yield-bearing alternative for investors seeking exposure to U.S. Treasuries within the DeFi ecosystem. Together, they offer diversified investment options, balancing stability with attractive yields for DeFi users.

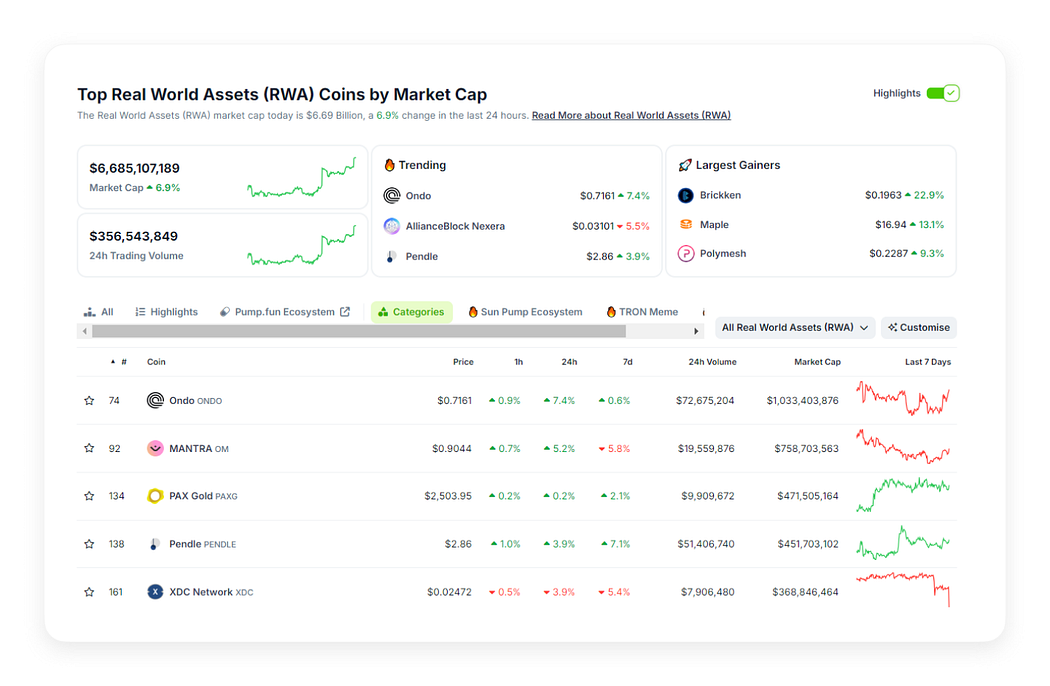

$ONDO is the largest RWA token by market capitalization. Source: CoinGecko. Accessed on August 22, 2024.

JPMorgan and Goldman Sachs are also working on similar initiatives in the tokenized U.S. Treasuries space, such as JPMorgan’s Onyx and Goldman Sachs’ concept of a RWA marketplace (J.P. Morgan | Official Website) (BeInCrypto).

These institutions have the resources, expertise and regulatory clout to navigate the complex landscape of tokenization and are likely to be the driving force in the RWA tokenization segment. BUIDL demonstrates how TradFi plays a role in accelerating the path to adoption for DeFi protocols like Ondo Finance while also incorporating some of these protocols for its purposes.

Notably, all of the instruments discussed in this section are fixed income instruments, currently the dominant segment in RWA tokenization, which we will delve into in the next section.

Shifting Trends in the RWA Landscape: From Equity to Fixed Income

Leadership in the RWA tokenization market has shifted towards the fixed income segment, which extends beyond U.S. Treasuries. Tokenized fixed income securities, such as private credit, have gained significant traction due to their stability and regulatory clarity. These assets offer predictable returns and are easier to integrate within the existing regulatory frameworks.

According to RWA.xyz, tokenized private credit accounts for the largest share of total RWA value:

Source: RWA.xyz. Accessed on August 22, 2024.

Tokenized private credit involves converting traditional debt instruments such as loans and bonds into digital tokens on a blockchain. This process is used by various entities, including investment funds, specialty finance companies and fintech startups. It generates returns through interest payments from the underlying loans.

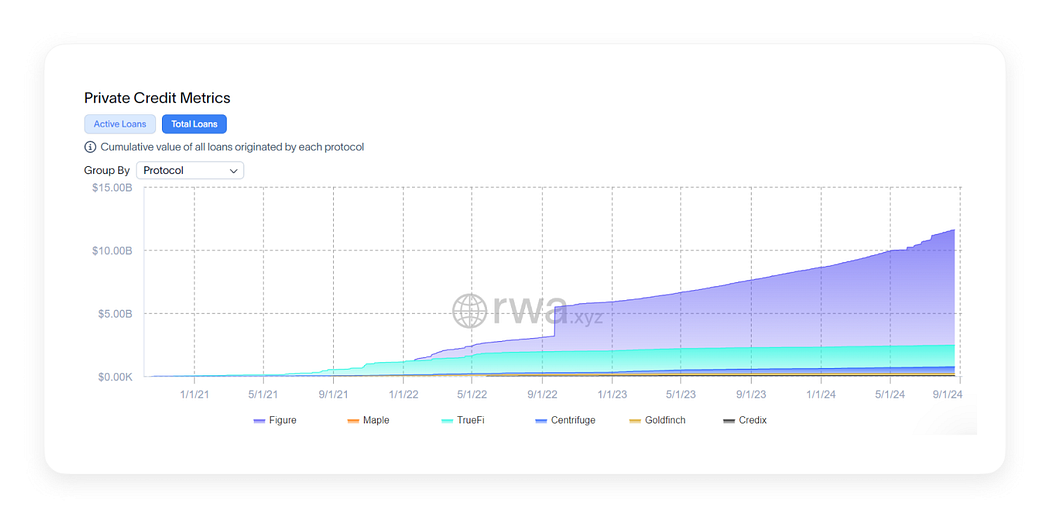

According to RWA.xyz, the top private credit tokenization protocols by total value of all loans originated are Figure, Maple and TrueFi:

Source: RWA.xyz. Accessed on August 22, 2024.

Figure leverages blockchain technology to streamline and modernize the lending process, primarily focusing on home equity lines of credit (HELOCs), student loan refinancing, and mortgage refinance. The platform uses Provenance, its own blockchain, to facilitate these services, aiming to enhance efficiency, reduce costs, and improve transparency in loan origination, servicing, and trading. Figure’s unique approach lies in its comprehensive use of blockchain across the entire lending lifecycle, differentiating it from other traditional and tokenized credit platforms (Figure Lending).

Maple Finance provides a decentralized infrastructure for institutional lending, enabling the creation of loan pools. Their strategy involves leveraging digital asset collateral such as BTC and ETH, providing high-quality, risk-adjusted yields. The platform operates on Ethereum and Solana and has partnered with blockchain credit risk management firms to offer managed credit portfolios (Maple Finance).

TrueFi is a DeFi platform specializing in uncollateralized lending. Launched in November 2020, TrueFi operates on the Ethereum and Arbitrum, connecting lenders and borrowers through smart contracts governed by the TRU token. Borrowers undergo rigorous credit assessments, including KYC and AML checks, and are assigned on-chain credit scores to determine loan terms. This process allows TrueFi to offer loans without requiring collateral, enhancing accessibility and efficiency in the lending market (TrueFi | Docs).

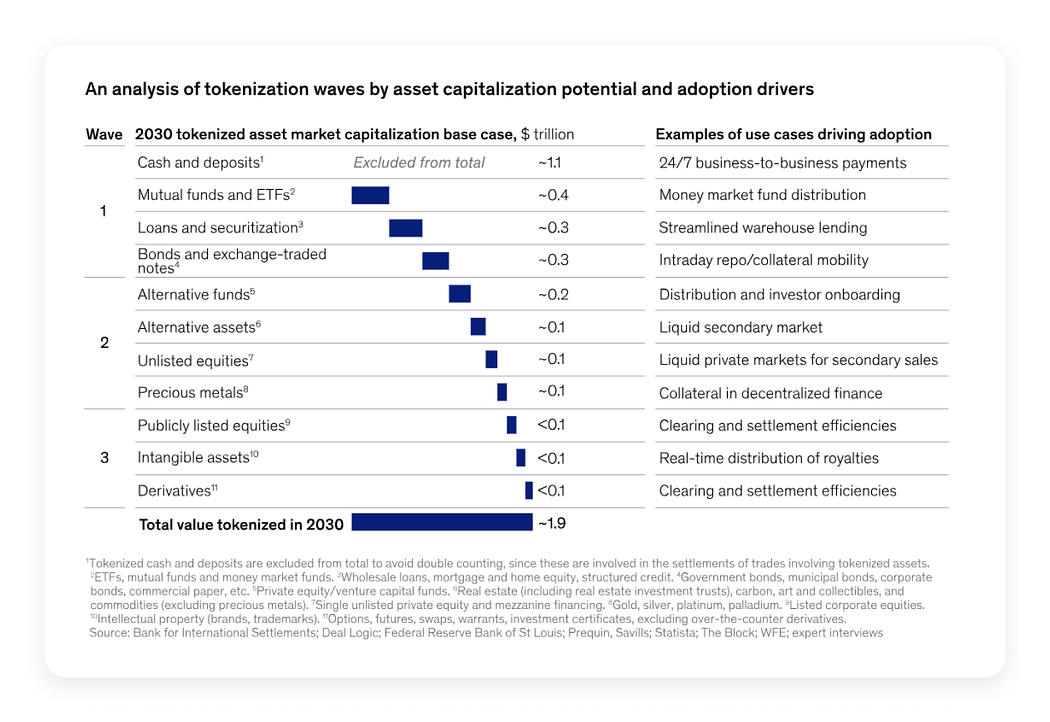

Private credit, along with U.S. Treasuries, is within the first wave of adoption of tokenized assets, according to McKinsey:

Source: McKinsey, “From ripples to waves: The transformational power of tokenizing assets”.

McKinsey’s report “From ripples to waves: The transformational power of tokenizing assets” suggests the appetite for investing in tokenization is influenced by the efficiency and profitability of current processes, the degree of outsourcing and the concentration of key players and their fees.

U.S. Treasuries and private credit both often involve high transaction volumes and relatively low margins, making the cost savings from blockchain’s efficiency and automation particularly attractive. The processes for these assets are typically more standardized and scalable, which reduces the barriers to tokenization and accelerates time to impact, enhancing the business case for early adoption. Since these activities are often outsourced to achieve economies of scale, there is also a strong incentive to adopt more efficient blockchain solutions to further reduce costs and improve returns.

The combination of high potential cost savings, quicker return on investment and the standardized nature of these financial products makes tokenized U.S. Treasuries and private credit prime candidates for early adoption in the tokenization landscape.

Tokenized Real Estate: Success Through Specialization

Real estate is a segment of RWA where the benefits of tokenization are particularly evident. Tokenization allows for fractional ownership, increased liquidity, and lower barriers to entry for investors, making real estate investment more accessible and democratizing opportunities. Despite its apparent benefits, the sector has remained relatively dormant so far and is expected to be part of future waves of adoption. Nonetheless, some companies have gained significant traction in this space. For example, RealT has emerged as a successful project that offers fractional ownership of U.S. real estate.

RealT is a blockchain platform that powers fractional ownership of real estate using tokenization. RealT’s marketplace represents a dynamic platform for investing in and trading of tokens that represent ownership shares in specific U.S. properties. These tokens provide both proportional ownership and rental income and can be traded on secondary markets.

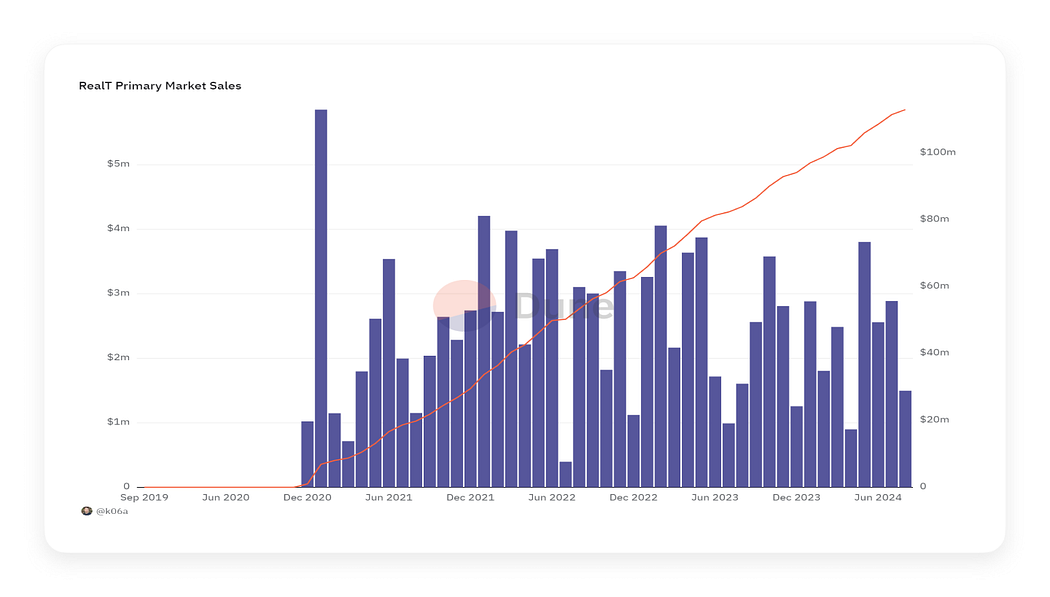

RealT’s monthly primary market sales now stand at around $2.9 million as of August 2024 with an all-time-high of $5.9 million:

Source: Dune.com. Accessed on August 22, 2024.

RealT’s $2.9 million in monthly primary market sales is significant, especially when compared to traditional real estate metrics. In the U.S., the median home price as of mid-2024 is at $412,300 (Federal Reserve Bank of St. Louis. (2024)). Traditional real estate companies typically facilitate the sale of individual homes, meaning each transaction could represent just one sale. For example, a real estate agent might close on a few homes per month, with each transaction contributing significantly to their total monthly sales volume. A typical real estate brokerage might handle monthly sales volumes that vary widely depending on the size of the market and the number of agents. For a small to mid-sized brokerage, reaching $2.9 million in monthly sales could be significant, equating to approximately 7 home sales at the median price. Larger brokerages with multiple agents might handle higher volumes, but this still underscores the scale of RealT’s achievement when considering the fragmented nature of traditional real estate sales.

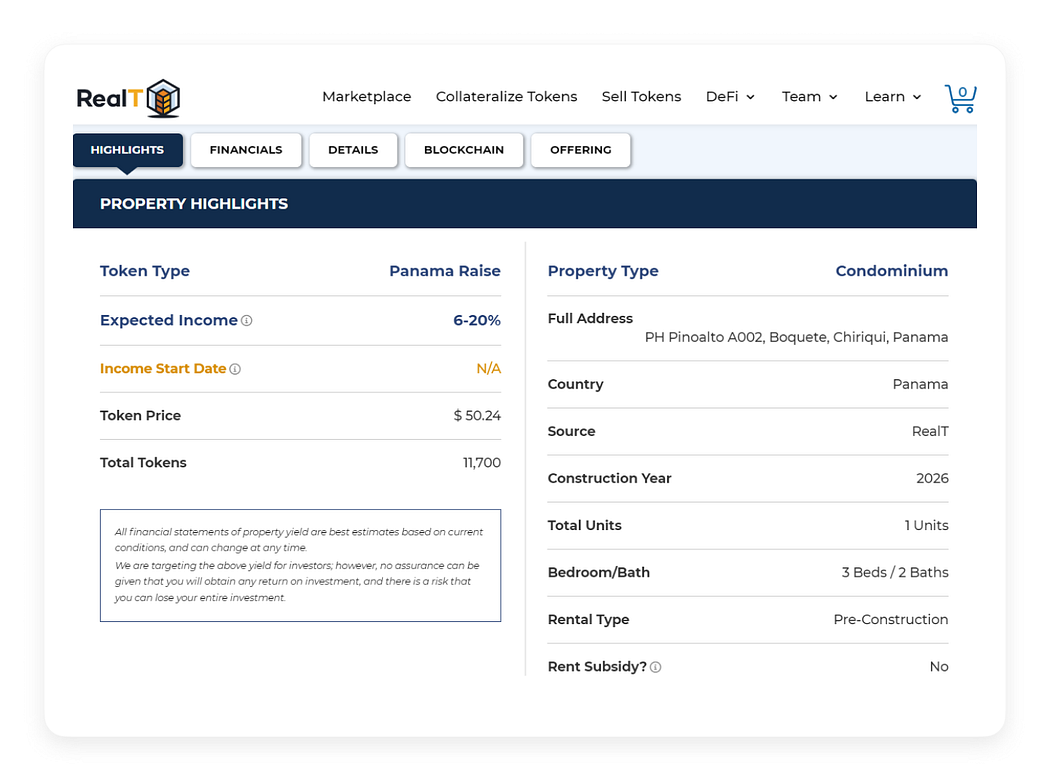

Example of an offering listed on RealT’s Marketplace. Source: https://realt.co/.

Large online real estate platforms like Zillow or Redfin facilitate billions in sales annually, but this is spread across vast markets with millions of listings. However, these platforms do not sell properties directly; they connect buyers and sellers, and their revenue comes from commissions, advertising and lead generation, not direct sales. For a company like RealT, which deals in direct sales of fractional property ownership, $2.9 million in monthly sales is significant given the more niche and emergent nature of the market.

In our previous report, we made an argument against the possibility of the mass adoption of real estate tokenization due to inability to tailor to the needs of individual investors, lenders, and tax authorities. RealT primarily deals with residential properties in the U.S. that are conducive to fractional ownership and tokenization. This implies that the platform might not be as versatile when it comes to more complex real estate transactions, commercial properties, or regions with less favorable legal frameworks for tokenization. Conversely, by focusing on a specific niche, RealT has been able to create a streamlined, scalable model that appeals to a particular segment of investors.

Tokenized Private Equity and Its Significance for TON

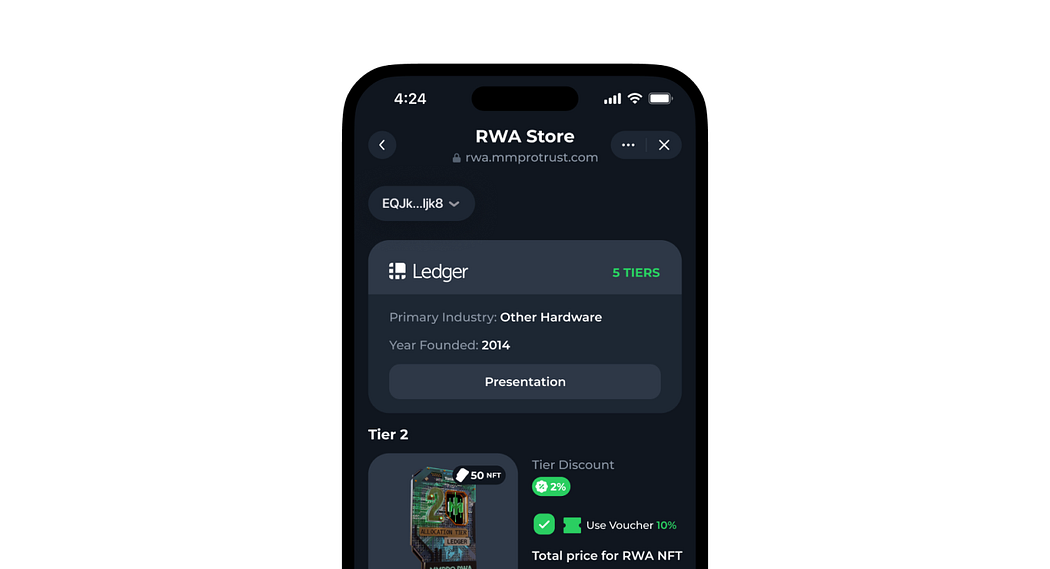

While the projects mentioned above focus on integrating RWAs with traditional financial institutions to attract institutional investors, TON’s approach to RWA is more DeFi-centric. Targeting regular DeFi users, TON enables them to diversify their portfolios by holding equity in private companies, a space that has traditionally been closed and opaque. MMPro exemplifies this by facilitating access and trading of tokenized private equity through the TON ecosystem.

MMPro is a new DeFi protocol on TON that offers tokenization of shares in companies like Ledger, Consensys (Metamask), Ripple, Circle, and Animoca Brands before they go public. Tokenized private equity involves converting shares of private companies into digital tokens on a blockchain, enabling fractional ownership and trading on digital platforms. This process makes private equity investments more accessible, liquid and transparent, aligning with the characteristics of the offerings provided by MMPro.

With MMPro Trust, investors can acquire fractional ownership in companies via RWA NFTs. These NFTs can then be traded on secondary markets, such as Getgems, and stored in Tonkeeper.

Source: https://rwa.mmprotrust.com/

While TON’s RWA landscape is still in the early stages, examples like MMPro Trust demonstrate the potential to mobilize various aspects of the ecosystem, including secondary markets, wallets and the companies involved. This approach is valuable for ecosystem participants who can now diversify their portfolios with equity, as well as for individuals outside the ecosystem who traditionally invest in public stocks and seek to diversify with private equity. By bridging these worlds, TON’s RWA initiatives create new opportunities for both DeFi users and traditional investors, promising a dynamic future for asset tokenization.

Nevertheless, tokenized unlisted equity is likely to have a longer path to adoption. The regulatory landscape for unlisted equities is still evolving, which creates uncertainty and poses significant compliance challenges. Private companies also often have less transparent financials and more complex ownership structures, making it harder to assess their value and risks accurately. Unlike fixed income instruments, which have predictable returns and established markets, unlisted equities require robust due diligence and investor protections, further slowing the adoption process.

However, protocols that successfully navigate these challenges and establish themselves early in the market for tokenized alternative asset classes can benefit from a first mover advantage. By building trust, setting industry standards, and creating a network effect, these early adopters can position themselves as leaders and capture significant market share as the ecosystem matures and regulatory frameworks solidify.

Future Outlook

RWAs have faced significant cold start problems, hindering their initial adoption. This problem manifests in several ways: there is a lack of established liquidity and market participants, limited trust and recognition from traditional investors, and regulatory uncertainties which slow down adoption.

There have been notable mismatches between the offered tokenized products and their target markets, often due to a lack of apparent benefits from tokenization and limited buy-side demand. These challenges have led to substantial shifts in the RWA landscape over the past year, with institutions like BlackRock and Franklin Templeton now driving the adoption of more feasible and attractive tokenized fixed income instruments, which offer clearer advantages and align better with market needs.

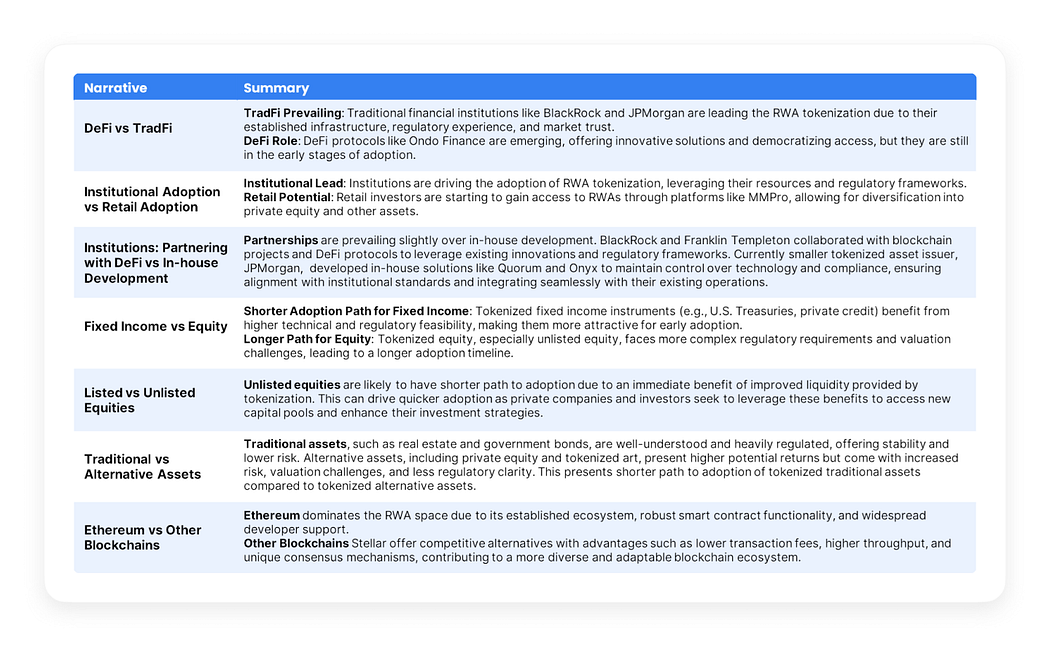

Overview of the current RWA narratives. Source: The Open Platform.

TON is well-positioned to participate in the further waves of adoption of tokenized assets, including unlisted and listed equities, commodities and real estate. By that time, the regulatory environment is expected to be more established, bolstered by the success of use cases currently pushed by large institutions. This evolving landscape will present TON and other blockchains with opportunities to gain a first mover advantage in these second- and third-wave markets, leveraging their innovative DeFi-centric approaches to offer new and compelling investment opportunities.