TL;DR

- The market structure for NFTs looks quite different than that of fungible tokens. In the NFT market, there tend to be more frequent capital formation events (mints), lower secondary volumes, challenges with bid liquidity, and a large number of orderbooks that exist offchain.

- As a result of these differences, the NFT MEV landscape also looks different. In particular, fewer arbitrage opportunities exist and more MEV gets extracted during mints. We’ve also identified several forms of MEV unique to the NFT market: sweeping and re-listing floors into bid walls (artificially creating the high volumes for arbitrage), trait sniping, and extraction from inactive listings.

- Viewing the DeFi market as more mature — and using it as a proxy for where NFTs may be headed — helps illuminate the gaps that exist today and areas of infrastructure that can address those challenges. Such opportunities include MEV-aware minting solutions, more open pricing data, dynamic onchain orderbooks, experimentation with new auction styles, and additional communication channels for traders.

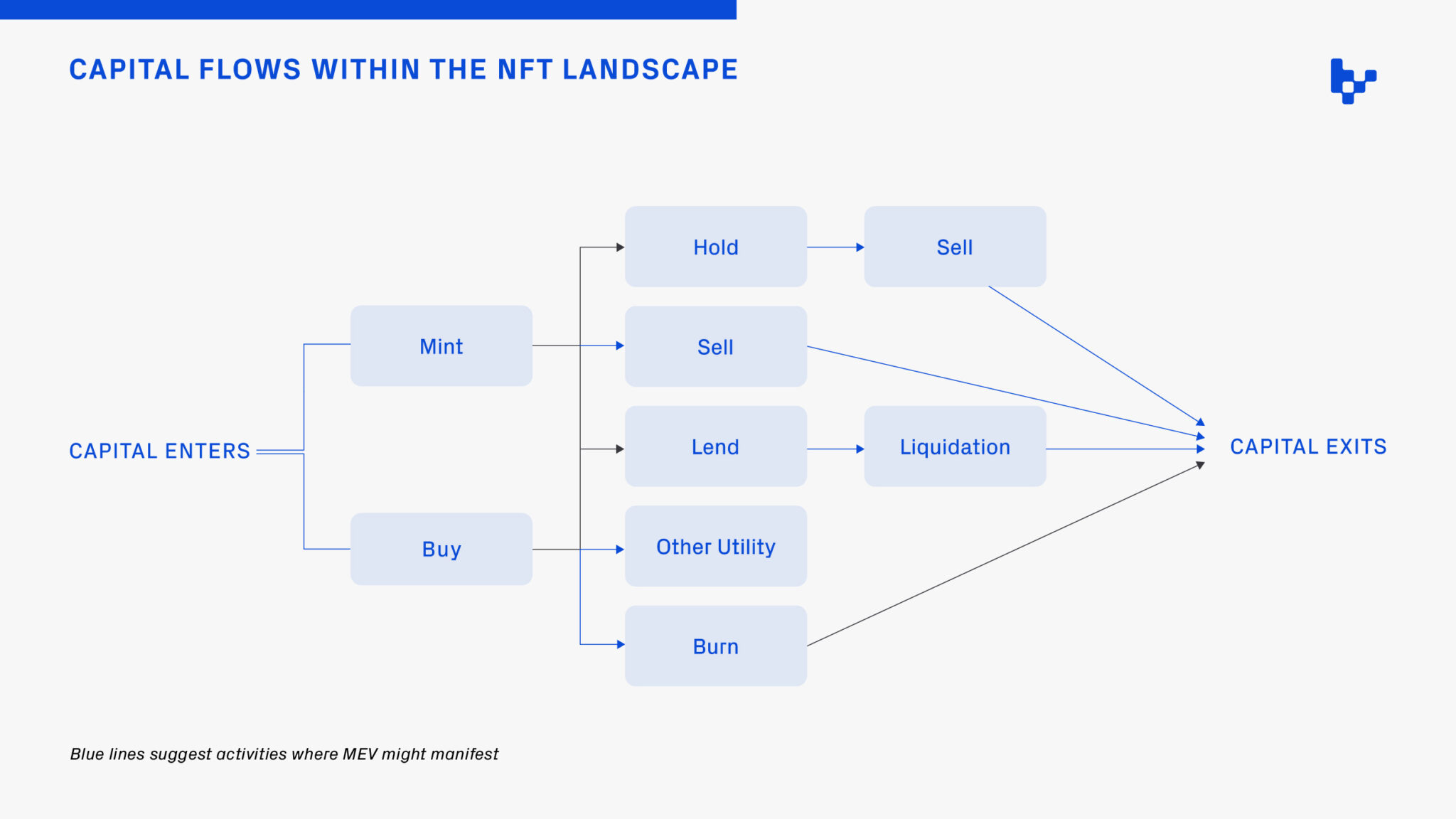

At present, the flow of value around NFTs generally happens at inception when an NFT is minted, and when it’s traded or lent out in a secondary marketplace. Both of these value flows are potentially laden with MEV, i.e. economic inefficiencies that get extracted from users when transacting onchain. How that MEV is handled can impact the business models and beneficiaries of market activity – from traders, to marketplaces, to wallets, to creators.

Yet MEV within the NFT landscape feels a largely underexplored topic. My sense is that this is because the structure of the NFT market looks quite different than that of DeFi. Importantly, those fundamental differences – including greater primary activity, smaller token supplies, and less secondary liquidity – influence the flow of value.

This piece will attempt to lay out some of the emerging MEV opportunities within the NFT market, how evolving market dynamics might impact these opportunities, and infrastructure that can be built with such considerations in mind.

The current state of the NFT market

Understanding the current structure of the NFT market is a useful foundation for identifying how MEV manifests within the market.

The cycle starts with a user minting an NFT. I call this a capital formation event, loosely analogous to an airdrop or launch for fungible tokens (whereby a new asset is created onchain). The difference in fungible vs. non-fungible markets, though, is at least threefold:

- Capital formation events are more frequent in non-fungible markets than in fungible markets.

- The ordering of mints for non-fungible markets can matter, as the mint number can assume financial value (via classification as a rarity trait or status symbol).

- Non-fungible collections tend to have much smaller supplies; a collection may mint 10k NFTs, whereas a fungible token often launches with a supply of 1 billion or more. This can impact liquidity on secondary markets.

When a user decides they no longer want to own their NFT, they can sell it in a marketplace (e.g., OpenSea, Blur, many of the ones Reservoir supports, etc). Those orders typically get listed in offchain orderbooks, where the listing sits until it’s either fulfilled or canceled. For these offchain orderbooks, there are several touchpoints for actual onchain activity: listing for the first time (i.e., setting listing approvals), canceling, and fulfilling orders. Changing the price of a listing requires the seller’s signature, but no additional gas fees (Appendix 1). There are also a number of orderbooks that operate directly onchain, like Zora and Sudoswap.

Beyond primary mints and secondary trading, it’s worth noting that there’s an emerging segment of the market around NFT utility. Onchain utility might involve staking NFTs for rewards, delegating the rights to an upcoming airdrop, burning (destroying) NFTs when using it as an in-game asset, or something else. But to put “emerging” in perspective: in February, nearly $2b of volume transacted in primary & secondary markets vs. a couple hundred million of borrow volume in NFT lending markets. Utility segments beyond lending are even more nascent. As such, mints and trading will remain the focus of this piece.

What does NFT MEV look like?

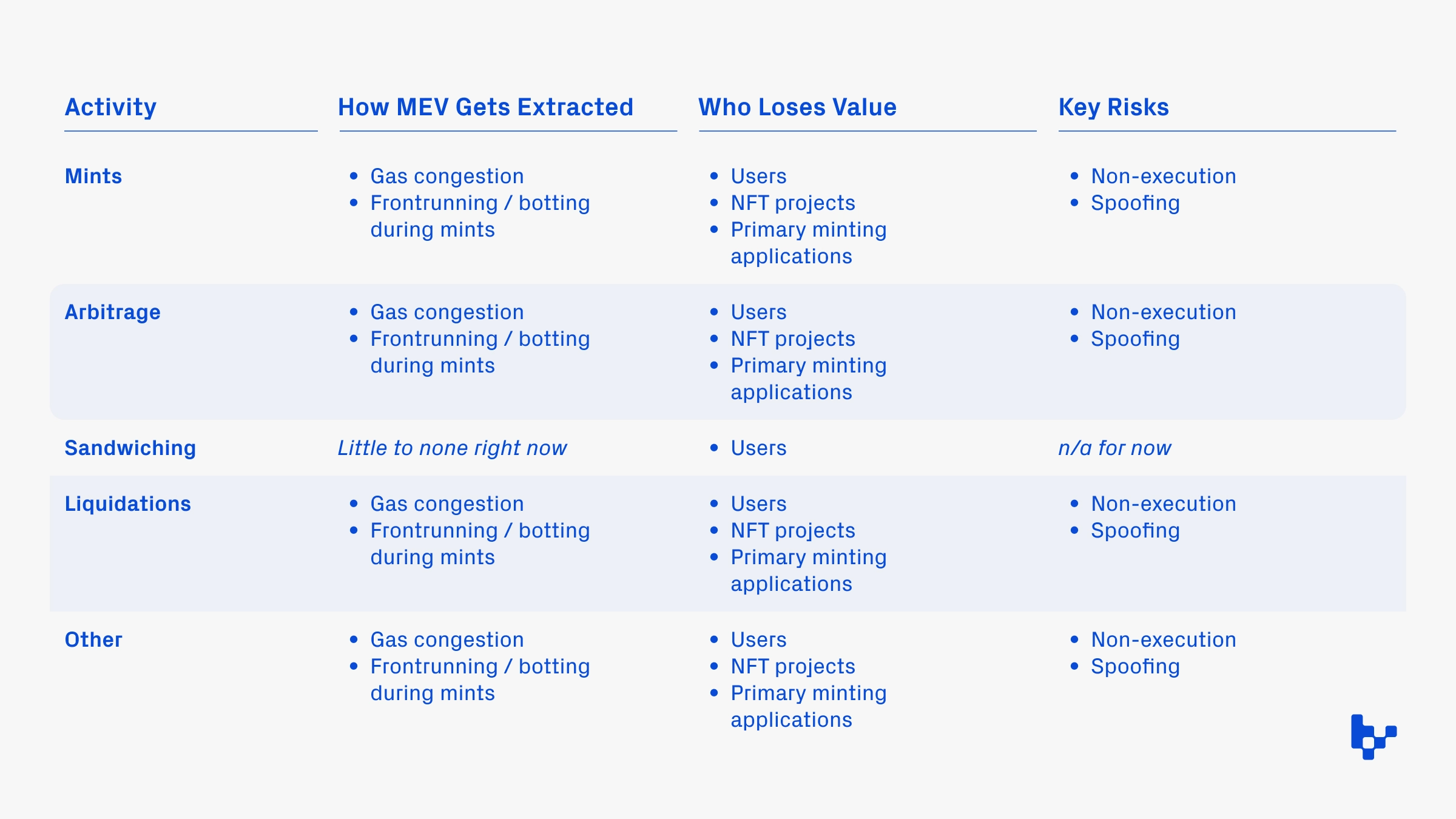

I classify MEV as any form of inefficiency within the market that results in transaction originators (users, wallets, applications) leaking value to third-parties down the stack (searchers, block builders, validators). It’s a loose definition, but the broadness helps when thinking about the different opportunities for value capture and/or value redistribution. Common forms of MEV include arbitrage, sandwiching, liquidations, and front-running.

Arbitrage

Arbitrage and sandwiching often require high volumes and deep liquidity, because spreads tend to be small and arbitrageurs want to move in and out of their positions quickly. NFT markets tend to have neither. Furthermore, there exists an illiquidity challenge: often, there’s no ready buyer on the other side of each listing. This means that even if someone spots an arbitrage opportunity, exiting (i.e., re-listing and selling) may be a risk.

Some NFT-native forms of arbitrage – and the risks associated with each – are as follows:

- Sweeping and re-listing floors for higher prices. A number of traders have claimed to do this profitably, taking advantage of walls of bids that may sit just above floor prices. In these scenarios, traders are almost artificially creating the high volume necessary for arbitrage. Key risks associated with this type of arbitrage involve high capital costs and inventory requirements.

- Finding coincidences of wants that aren’t being treated as such. An example would be someone listing their CryptoPunk with red/blue glasses for 1 ETH, while someone else has placed a bid of 2 ETH for any CryptoPunk that has red/blue glasses. A searcher could come in, call Seaport’s MATCH function to fulfill the two orders, and claim the difference as a tip (reward). This strikes me as a low-risk arbitrage opportunity. Here, non-execution is the main risk searchers face.

Trait sniping, a form of arbitrage unique to the “non-fungibility” component of NFTs. If someone sees that an NFT with a particular trait is trading for X, but knows that other NFTs with the same trait trade for X+Y, they can buy it and relist it for the higher value. MEV is realized if the searcher pays a large amount of gas to ensure their bid gets prioritized. In these scenarios, searchers face exit risk: there may not be a bid waiting on the other side of their listing. The searcher thus has to underwrite holding the inventory for an unknown period of time, while also accepting exposure to longer-term price fluctuations in the price of those traits.

Sandwiching

At present, there doesn’t appear to be much sandwiching in NFT markets. This is in part because most NFTs don’t get dynamically repriced as available supply changes. In fungible markets, large orders move markets. With NFTs, someone buying 10% of floor NFTs doesn’t directly change the pricing on other floor NFTs. NFTs tend to be priced individually, rather than in aggregate. Notably, some dynamic pricing infrastructure – like Sudoswap, an NFT automated market maker (“Uniswap for NFTs”) – is emerging. Sudoswap helps tackle the painful problem of illiquidity in NFTs by ensuring there always exists at least some bid for a pooled NFT. The trade-off is that dynamic, automated pricing also expands the surface for sandwiches.

Liquidation MEV

Another common form of MEV exists within lending markets, called “liquidation MEV” – searchers profit by being the first to spot and claim a liquidation fee. A growing number of lending books are being built onchain (e.g. where the liquidation engine lives directly on a protocol like Seaport), with declining price auctions such that as soon as the price crosses a reserve collateral price, the liquidation is triggered. I imagine there will be a cohort of searchers that specialize in manipulating floor prices / prices of certain NFT collateral such that they can preempt or control when an NFT will get liquidated.

Additional forms of MEV

Other types of NFT MEV might include:

- Congestion during mints. Popular mints can result in users paying millions of dollars in gas fees; this is value that the NFT project creates, but ultimately gets extracted by validators.

- Botting during mints. A searcher could spot the first transaction of a mint in the mempool, check the supply of tokens set to be minted, and front-run part or all of the remainder of the mint.

- Accidentally leaving orders listed (often called inactive listings). Because canceling a listing costs a fee, sometimes users will simply transfer the NFT to a new wallet to end the listing. The tricky part is that this technically preserves the original order – if the person re-transfers the NFT to the original wallet, the listing reappears. By that point, the floor price could have moved above the original listing, and a savvy third-party could grab the underpriced NFT. MEV is created because a searcher may bribe validators with a high gas fee to ensure their bid on the listing gets prioritized.

- Arbitrage related to NFT rentals. We’re seeing a trend toward unbundling NFT rights / utility from the asset itself. In other words, AirBnb for NFTs is emerging: own the asset (the house) but let others pay to temporarily use / claim the benefits an owner would normally enjoy. Such liquid delegation is especially useful for arbitrage related to airdrops – buying the rights to a large number of NFTs (vs trying to purchase the NFTs themselves) in anticipation of an airdrop requires less capital, limits a steep rise in floor prices, and presents an opportunity to claim a significant portion of the airdropped supply. If we start to see greater qualifications for airdrops (as we’re already seeing in fungible markets), holders of those NFTs could have asymmetric information about the likely size of their NFT’s claimable airdrop.

Finally, there are likely even more forms of NFT MEV that I’m missing, including spoofing, inefficiencies related to burn & redeem functionality, and front-running mints (to name a few). This list is meant to be generative and provocative, with the hope that outlining some of these sparks an idea / project related to mitigating or capturing NFT MEV opportunities.

Opportunities for Infrastructure

Based on the current state of the market, as well as where MEV seems especially present, the following could present interesting opportunities to build NFT-native infrastructure.

- MEV-aware minting solutions. In particular, auctions built for NFTs can help projects capture more of the value they’re creating: letting users bid for access & ordering in a mint can provide a way to help projects price discriminate while simultaneously mitigating high gas prices. If the ordering itself happens offchain and/or pre-mint, projects can spread out the mint over several days or select times when other onchain activity is low (Appendix 2).

- Enhanced pricing infrastructure. This could take a variety of forms – better data to show how traits are being priced (e.g., to help searchers identify trait sniping opportunities), dynamic pricing mechanisms (like Sudoswap) to help price NFTs in aggregate rather than individually, sequential auctions for improved price discovery, or something else.

- Infrastructure built to reduce exit (illiquidity) risk. I generally believe that it’s difficult to price an NFT and, because of that, fewer people are willing to make bids. Bargaining mechanisms could be one way to help. If a user has listed an NFT for 2 ETH and a buyer bids 1 ETH, there might exist a clearing price somewhere in the middle. Having a channel to negotiate could increase overall liquidity while also driving toward a better understanding of how to price NFTs. In fact, it’s likely that this category and the above (pricing infrastructure) will have significant overlap.

Increasingly efficient fulfillment protocols and tooling. As orders get more complicated (e.g., sellers starting to list multiple NFTs within a given order) and more active traders and/or market makers enter the space, finding efficient ways to match or fill orders can improve the trading experience. Seaport and Reservoir are good examples of complementary infrastructure in this category; both help facilitate shared liquidity among marketplaces, which allows for more efficient discovery and matching in environments of diverse preferences. Relatedly, the surface area for identifying coincidences of wants will continue to grow, with opportunities to build preference-aware matching solutions that specialize in partial fills across a web of orders. I also imagine there are ways to better cater to different types of traders: pro traders may want near-instant transfers, but more retail-oriented consumers may be fine for a bid to get accepted at time X but technically fulfilled / transferred a number of hours later, when gas costs are lower.

Concluding Thoughts

Looking toward the future, I strongly believe we’re going to see more of a spectrum develop around the non-fungibility of tokens. The current state is that most NFTs are heterogeneous and thus have difficulty serving as substitutes. Shared traits or floor tokens more closely resemble substitutes, but consumer preferences could still differ. Contrast that to NFTs that serve as ground pass tickets at a golf event – where heterogeneity might exist in that certain traits (such as date) create differences in preferences, but on the whole they act as near-substitutes because a consumer does discriminate between tickets on a set day (given that all provide equal access to the event). As the spectrum develops, and NFTs start to represent everything from onchain art to tickets, affiliate links, IP licenses, property titles, and more, I imagine we’ll see even more MEV emerge.

On the whole, it feels like we’re still in the early innings of NFTs. I enjoy thinking about NFTs because I find them a great way to bring exogenous capital into the crypto ecosystem, and I think the design space is wide open. But in the early stages of any market, there are always inefficiencies that exist. I’m hopeful that exploring how MEV persists throughout the market – and what opportunities such exploration highlights for building more delightful user experiences – will help pave the path for greater adoption.

Thank you to Carson Brown, Daniel Marzec, Jason Maier, 0age, Josh Doman, Jesse Walden, Ankit Chiplunkar, and Foobar for conversations and feedback on these ideas.

Appendix

- Technically, changing the price requires creating a new order. Seaport will always default to the lowest listing, and creating a new listing does not require gas fees (a new listing is distinct from setting an initial approval). If someone changes their listing to be at a higher price, the new order doesn’t require any additional gas. However, they do need to cancel the old order (to remove the lower-priced listing), and the cancellation does cost gas.

- Pikapool is the main player that I know innovating in this space; any NFT projects interested in re-capturing value during mints should check them out!

This piece was originally published in collaboration with Frontier Research.