Abstract

According to whether their centralized risks are isolated, stablecoins can be classified as centralized stablecoins and decentralized stablecoins. As long as they are not completely decentralized, stablecoins will always expose to the whole default risks brought about by the centralization.

In an era where centralized regulation is threatening to the crypto industry, decentralization is a pivotal attribute of stablecoins.

The vast majority of stablecoins cannot become the basic currency of the crypto world. Most stablecoins are only equivalent to commercial papers, exercising the functions of mainstream stablecoin borrowing and lending through exchange transactions.

A stablecoin mechanism should include creating its own demand scenarios, not just being a general equivalent (which is difficult for small-scale stablecoins), but also considering some unique economic activities (such as clearing and high-yield bonds).

The result of the race for centralized stablecoins has almost been clear, with USDT and USDC neck and neck, others fall behind. Although CrvUSD contains centralized risks, its stablecoin function module is complete so it has a good perspective. The realm of decentralized stablecoins is almost a desert currently. There is a concrete demand for specific users in this field and there are potential development opportunities in the future.

Introduction

Starting in 2018, countless investment institutions and media outlets have referred to stablecoins as the holy grail of cryptocurrencies. However, the process of approaching to the holy grail has not been smooth.

The giant stablecoin project, Libra, which began in 2018, has been constantly interfered with by national authorities from the very beginning and died before it was even born.

According to the Wall Street Journal, on July 20, 2021, Circle paid $104 million to settle with the SEC.

On October 15, 2021, Tether was fined $41 million by the US government for false statements.

On February 13, 2023, in order to avoid SEC prosecution, Paxos stopped issuing BUSD.

I have no intention of discussing the right and wrong of these penalties and regulations. Listing these things only serves to show that all centralized stablecoins face the risk of centralization and must accept interference from centralized forces. If stablecoins are the faucet, and the liquidity of the crypto world relies entirely on centralized stablecoins, then the asset pricing power of the crypto world will no longer be within the crypto world. At present, the decentralized power in the stablecoin race is in danger. No one wants a decentralized world to be held by the power of centralization. However, the current situation is contrary to our wishes:

Centralized stablecoins such as USDT, USDC, and BUSD occupy the vast majority (91.6%) of the stablecoin market, while decentralized stablecoins such as DAI and FRAX are still using centralized stablecoins as collateral.

Graph 1: The crypto stablecoin industry is dominated by the centralized stablecoin

Risk always follows Murphy’s Law.

The U.S. court resolution on BUSD once again demonstrates the centralized risks inherent in USD-pegged stablecoins. With a current market cap of $15.7 billion, the market share of BUSD will be contested by other stablecoins as Paxos announces the cessation of further issuance of BUSD. Compared to similar stablecoins such as USDT and USDC, purely on-chain decentralized stablecoins have relatively better resistance to regulatory scrutiny.

Why do Stablecoins need decentralization

Stablecoins can be operated in a centralized way. Centralized-operated stablecoins already exist and can not be ignored. From USDC and USDT to DCEP, these centralized stablecoins not only dominate in terms of scale and cost, but also benefit from traditional world empowerment and guarantees. 0xhankerster.eth believes stablecoins can be classified into centralized stablecoins and decentralized stablecoins based on their issuance mechanisms. The classification at that time focused on the form of centralization, rather than the essence of facing centralization risks. This article categorizes stablecoins into centralized and decentralized based on their centralization risks exposure.

Like all other Web3 projects, questioning the original intention is necessary when launching. Why does a stablecoin have to decentralized?

We choose a decentralized stablecoin, because several decentralized currencies existed in history.

The Feasibility of Decentralized Currency

The currency starts in the form of decentralized way, the private debts became to the original currency in human’s early history. Whether it is the barter theory of currency, or the theory of debt-based currency formation, centralized credit did not participate in the currency generation process from the beginning.

As early as 4000 BC, on the Mesopotamian plain, people invented clay tablets to record events. Important things were recorded, such as debts. Debt records included the content of the debt, the payment method for repayment, and penalty measures for overdue payments. These debts could be used as a means of payment.

According to the description of anthropologist David Graeber, from 3100 BC to 2686 BC, Egypt was an agricultural society where grain lending was common. People would repay the grain during the harvest season of the new year. The grain lending information was recorded on clay tablets, including the borrower, quantity, time, and so on. These clay tablets were called “Henu”. People used these clay tablets as currency in commodity circulation.

Whether it is gold, silver, or debt, it is a type of decentralized credits.

The merit brought about by the decentralized stablecoin is unique, which is reason the epoch echos the decentralized stablecoin.

The Merit of Decentralized Stablecoins

The purpose of issuing currency is to increase credit, but centralized stablecoins do not have the power to mint coins. What we are seeking is the alchemy in the information age, hoping to create stable credit without centralized power. Cryptocurrency purists the believe that the issuance of currency is stolen by centralized institutions. The party with the right to issue has the seigniorage tax, and the issuing party has sufficient motivations to issue or overissue currency. Once centralized stablecoins are issued in a decentralized network, those who control the issuance of stablecoins are no different from those who issue currency in the traditional world, unless the power to mint coins is taken away from the government and central bank. The issuer of stablecoins can only become a commercial financial institution issuing letters of credit.

Centralized stablecoins face the threat of centralization. Centralized stablecoins are always threatened by the risk of centralization, and the credit of stablecoins may be questioned due to the credit defects of the center, and the value of stablecoins may be challenged. The trust of centralized stablecoins is not natural. Both USDC and USDT have faced runs due to market rumors and gossip. Behind them, the US financial regulatory system backs their credit. Centralized stablecoins will inevitably be subject to constraints from the US government. When Tornado Cash was treated unfairly by the US government, Circle marked USDC that interacted with Tornado Cash without any democratic process. Similarly, authoritarianism will harm the rights of any holder of centralized stablecoins. Decentralized stablecoins offer everyone an alternative choice.

The decentralized stablecoin has its own market

Like any other product, different products have their own target users. In traditional thinking, there is no organization that is not centralized. Centralized risks may be hidden among other risks, such as the risk of single point failure in operational risks. Any organization will choose its own risk strategy based on its risk preference. Centralized risk is different from other traditionally defined risks. For users sensitive to centralized risks, other costs and risks are a necessary cost.

Stablecoins: The Wings of Icarus

Since Adam Smith create his economics religion, it seemed natural for money to be generated through national credit. It wasn’t until the rise of Hayek that the de-nationalization of money was clarified. Algorithmic stablecoins continue on the path of BTC, exploring the direction of decentralized credit generation. Unlike fiat-collateralized stablecoins such as USDT and USDC, algorithmic stablecoins were intended from the beginning to replace the central bank’s role in creating credit. Algorithmic stablecoins do not help fiat currencies capture the value created in the crypto world and compete with centralized stablecoins issued based on fiat currencies. Therefore, algorithmic stablecoins are difficult not to conflict with the interests of central banks or governments. However, a sustainable stablecoin has to reach a scale threshold.

Stablecoin is a scale economic business

As a stablecoin, in the long run, it must break through a certain scale limit to achieve a positive ecological cycle.

In addition to price stability and no market risk, stablecoins need higher interest rates and lower transaction costs to increase their value.

Table 1: small-scale stablecoins do not have advantages

When the scale of a stablecoin is not large enough, it must be settled through other tokens when exchanging for most non-stablecoins. Even when creating trading pairs, a large amount of stablecoin will be absorbed by pegged trading pairs, limiting the amount of credit available for direct connection with other risky assets. Not only are there few direct trading pairs, but the fees are also high. The use of stablecoins with low market size will also face higher trading slippage, which is not conducive to whale entry. Taking the example of exchanging various stablecoins for WETH, using 1inch’s trading route, the slippage of $100,000 worth of LUSD is 1.78%, while that of FRAX is 0.36% and DAI is 0.2%.

All of these disadvantages in scale will increase the trading costs of stablecoins. In order to offset trading costs, the project party needs to increase the operating costs of the project and provide higher returns to the stablecoin. Therefore, stablecoins are a business of scale economy.

When the scale of stablecoins cannot be reached, the income generated by stablecoins (transaction fees, interest, liquidation fees, derivative income) will not cover the costs of maintaining the scale. In the long run, this stablecoin will inevitably face collapse.

The stablecoin is a business that is tabooed by traditional powers.

If decentralized stablecoins want to achieve its scale, they will inevitably attract attentions from traditional powers.

What is more, traditional institutional power have always had a negative view of cryptocurrency.

Not only did the US government cause Libra to be stillborn, but the International Monetary Fund has also had a hostile attitude towards cryptocurrencies. As various central banks lead the charge with the DCEP, who will be the ragtag army that should be eliminated? On February 23, 2023, the IMF Board of Directors declared that cryptocurrency should not be granted legal tender status. We cannot know whether the scale advantage of stablecoins is lower than the threshold of attention from traditional powers.

Without scale, it is impossible to sustain economic operations, and with scale comes the risk of interference from centralized powers. This is the Icarus’ Wings of stablecoins.

The way out for stablecoins is either to become a lackey of traditional powers or to prepare thoroughly for decentralization and complete separation from the world.

The industry structure of stablecoins

At present, the stablecoin industry is dominated by USDT and USDC, which hold the vast majority of the market share. However, there are over a hundred types of stablecoins. What kind of business model is this for stablecoins?

Monetary Base and Board money

In macroeconomics, we divide currency into different levels based on their liquidity, ranging from M0 to M3. This liquidity difference is widely present in tokens, and token liquidity itself is an important component of token value. Users prefer to hold tokens with high liquidity, and they are willing to use high-liquidity tokens as the counterparties in transactions. As an example, if you’re a project creator looking to price your token, you’d naturally choose USDC or USDT. Who would use Alt-stablecoins with fewer holders, higher slippage, and fewer token amounts as a benchmark and trading counterpart? BTC and ETH are more reliable compared to these small-scale stablecoins.

The current situation is that, apart from USDC and USDT, the vast majority of stablecoins find it difficult to obtain “passive” opportunities to establish trading pairs (here, “passive” refers to opportunities where other project creators aside from the stablecoin project creator establish liquidity and trading pairs). Therefore, most stablecoins must rely on converting into high-liquidity tokens like USDT, USDC, BTC, and ETH before trading with the target token. This situation is similar to depositing money in a bank, where you have a fixed-term deposit with a certain amount. You can’t use the fixed-term deposit directly for consumption, but you can sell it on the secondary market and use high-energy currency for consumption.

To use this analogy, in fact, USDC and USDT have already occupied the position of high-energy currency in the stablecoin world. The vast majority of stablecoins, that rely on high-energy currency to provide liquidity, are actually providing a form of broad money similar to traditional financial markets.

Graph 2: The market structure of Stablecoins

A stablecoin issue system or a lending system?

Stablecoins of the broad money type have operating mechanisms for creating liquidity that are similar to borrowing and lending. Many Alt-stablecoins actually do not have trading pairs with many tokens. According to traditional definitions, these Alt-stablecoins cannot even be considered as general equivalents, and their external returns are almost zero, except for internal airdrops and mining, while creating and lending the token will also incur costs. Apart from maintaining relative stability in debt valuation, these Alt-stablecoins have no value. Therefore, the only way out for these Alt-stablecoins is to exchange them for mainstream trading currencies through trading pairs, and then participate in on-chain economic activities. In order to obtain opportunities for on-chain activities, stablecoin projects have to incentivize Alt-stablecoin to Main stablecoin trading pairs. And this incentive is actually a subsidy for interest rates on mainstream stablecoins.

Graph 3: Stablecoin equals lending

Assuming stablecoins cannot create on-chain economic activity, users who generate X stablecoins through stablecoin creation mechanisms can only exchange them for mainstream stablecoins that have multiple on-chain activities before engaging in economic activities. This process is equivalent to a mainstream stablecoin lending pool. In terms of functionality, Alt-stablecoin creation mechanism + trading pair = overcollateralized lending.

If X stablecoin has unique economic activities, then X will have differences compared to USDT and USDC. This will create motivation for USDC and USDT holders to exchange for X and participate in economic activities.

We can see from the trading pairs between many non-mainstream stablecoins and mainstream stablecoins on Curve that a large number of mainstream trading pairs are “borrowed out.”

Graph 4: Capital imbalance in trading pair: a lending system

Compared to obtaining mainstream stablecoins through lending pools, using non-mainstream stablecoin creation mechanisms + trading pairs results in more stable and controllable liquidity costs. In trading pair pools, in addition to mainstream stablecoins, non-mainstream stablecoins are needed to form trading pairs, which reduces system capital efficiency. If the non-mainstream stablecoins have unique economic activities that can allow mainstream stablecoins to be redeemed in reverse, it’s fine; otherwise, the trading pair becomes a lending pool. Currently, non-mainstream stablecoins like FRAX continue to incentivize trading pairs, which is a kind of implicit “interest subsidy”.

The realm of stablecoins

Since the creation of USDT in the fall of 2014, creators of stablecoins have made various attempts at creating stablecoins. Currently, the most mainstream method is still centralized, where one U.S. dollar is deposited into a designated real account, and one U.S. dollar of stablecoin assets is issued online. As government regulation has gradually improved, these centralized stablecoins have been regulated to prevent risks such as arbitrary inflation or inadequate collateral asset liquidity. Disclosure has also gradually increased. However, centralized risks have always been present. Recently, due to Silvergate Bank’s failure to submit reports to the SEC on time, concerns have arisen again as to whether USDC issued by Circle will default.

As a result, attempts to create stability and credit through algorithms have never ceased.

Methods of creating stability: There are several ways to use algorithms to create price stability for stablecoins:

Rebalancing stablecoins

AmpleForth created a stablecoin with a rebalancing issuance. The token has a target price and a market price. The quantity of AMPL (the stable token of the AmpleForth project) will increase or decrease based on the difference between the target price and the market price. This method stabilizes the price of AMPL, and for AMPL borrowers, the value is consistent when borrowing and repaying. However, assets priced in AMPL in the user’s asset portfolio still bear market risk. To address this, AmpleForth designed layered derivatives for market risk, with some derivatives bearing greater risk and others bearing relatively less risk. The market’s feedback was a failure. (There was no liquidity in Buttonwood.) The stability obtained through derivatives is no different from hedging market risks through futures.

Traditional rebalancing mechanisms have long lost market vitality. No new stablecoin projects are known to continue to use rebalancing mechanisms. However, the recent (3,3) reverse liquidity incentive strategy has shown some light. Liquidity incentives are essential for all stablecoins, and token deflation can effectively support the price of a single stablecoin. Is it possible to lock stablecoins and require them to be in a borrowing environment or flow into a liquidity pool? In other cases, deflation can support stablecoins so that they are not underwater.

Limiting-circulation stablecoins

In 2018, cangulr90 discussed with others on Ethresear about limiting users from buying tokens when the token price is higher than the target price and from selling tokens when the price is lower than the target price. This idea was later used in FEI’s system in a modified way. Compared with mandatory restrictions, FEI uses a gentle approach to increase costs to limit users’ buying and selling, like a “soft knife.” FEI’s failure cannot be solely attributed to the restriction of circulation. Franz Oppenheimer believes that FEI’s incentive and punishment mechanism violates market rules. When FEI’s price remains below the target price, which punishments will cause stablecoins to lose their basic demand? After all, who would hold a stablecoin with high transaction fees? The value of currency is reflected in its circulation. While stabilizing the coin price, if it loses liquidity, the gains do not outweigh the losses. Looking at the liquidity of stablecoins such as USDC and DAI, FEI’s daily trading volume is only about 1/8 to 1/10 of other stablecoins.

seigniorage stablecoins

Seigniorage stablecoins are designed to maintain relative price stability of their assets and minimize market risks. Tokens that are not subject to control often exhibit volatility exceeding that of real assets. To achieve stability, some innovations have employed a risk layering approach, in which a volatile token that is subject to system control is incorporated into the stablecoin system. By linking the occurrence of redemption between stablecoins and volatile coins, price fluctuations caused by supply and demand of stablecoins can be transmitted to the volatile coin. There have been many projects attempting this approach. The most famous is UST-Luna, which uses the destruction of Terra, the underlying blockchain, to exchange for an equivalent stablecoin, UST. The destruction of UST can then be redeemed for Terra. Some other projects allow the purchase of bond coins when stablecoins are below the target value, and the purchase of stablecoins using bond coins when stablecoin prices are above the target value, which can then be sold on the market. However, the majority of such stablecoins have ultimately failed.

To allow volatile tokens to absorb the potential volatility of stablecoins, it is difficult to limit the issuance of volatile tokens. The volatility expansion of volatile tokens can ultimately erode confidence in stablecoins. Currently, the only surviving project is the linkage between FRAX and FXS. Moreover, FRAX is the second-largest algorithmic stablecoin. Its feature is to introduce USDC as the majority credit collateral, which significantly increases the protocol-controlled value PCV.

Although their stability is poor (most of such stablecoins have gone to zero), I still believe that this is the most crypto-designed stablecoin scheme: the value capture of issuing tokens is not through an income-profit model, but as a medium for transmitting system value, where the value of volatile tokens is positively correlated with the scale of stablecoins.

Over-collateral stablecoin

Overcollateralized stablecoin is currently the most mainstream and theoretically mature way of issuing stablecoins. The overcollateralized stablecoins represented by DAI and LUSD have been working well for a long time, and a new group of potential stablecoin competitors, GHO and CrvUSD, also adopt the overcollateralization method. Overcollateralized stablecoin projects are often classified as lending projects in DeFi’s classification. Essentially, it takes the debt of users and uses it as the cornerstone of stablecoin issue. It is not just modern central banks that use debt to issue currency, the method of issuing currency has stood the test of history.

The use of debt as a medium of payment and circulation always exists. Not only the previously mentioned historical precedent of using debt as a currency in circulation, the first paper money issued was the jiaozi of the Song Dynasty. The paper money originated from people depositing iron money in commercial banks, producing a debt certificate from the bank to the consumer. It gradually evolved into the debt of the country becoming the cornerstone of currency issuance.

The debt would form the basic demand for stablecoins, allowing them to gain an anchor of value. In the short term, users are induced to redeem additional issues for arbitrage, and interest rates are used to regulate the supply and demand for stablecoins to achieve price stability. Overcollateralized stablecoins have good stability because of the solid basic need: you can’t get back the overcollateralized assets without returning the stablecoins.

The shortcomings of the mechanism are also obvious: once the liquidation price of the collateral is lower than the lent stablecoin, users will not return the stablecoin. The project is required to take the initiative to liquidate the collateral and recover the lent stablecoin at the necessary time to realize the closed loop of stablecoin circulation. Once the liquidation of collateral to obtain purchasing power is not enough to buy back stablecoins, it will form a bad debt for the platform. Therefore, the over-collateralized stablecoin mechanism requires the collateral to have a broad consensus of value and good market liquidity.

Choice of Stable Anchor

What should be the anchor for a stablecoin is also a dimension for stablecoin to explore.

Anchored by traditional world fiat currency

Common stablecoins use fiat currencies as an anchor. The underlying assumption is that mainstream fiat currencies are relatively stable in value in the short term and suitable as a benchmark of value. In the long term, airdrops that stand for interests needs to be given enough to sustain the growth of the stablecoin asset size. Gold, the world currency of the previous era, has also been held out as a benchmark of value. Whether it was the British pound as the world currency or the US dollar becoming the world currency, both used to anchor gold to enhance the acceptance of their currencies. Drawing on such practices, stablecoins can borrow directly from the influence that traditional world currencies have developed over time, reducing the difficulty of promotion. The vast majority of current stable coins are tied to the US dollar, euro or gold, and people trust more in the stability of the value of these currencies. The pain point of the algorithmic stablecoin is that it cannot do better than the centralized approach. Compared to the small pond of on-chain assets, the traditional financial world can be an ocean, and a little bit of liquidity can be distributed to nourish the entire blockchain world. If the centralized powers which have ruled the world for so long have the willing to regulate, ordinary defaults and fraud would disappear from the scene. The centralized stablecoin camp propped up by USDT, USDC, and BUSD back other stablecoins into corners. They are bigger, cheaper, and have better credit in most cases. Decentralized stablecoins have to accept worse service and higher costs in exchange for decentralized security.

Another problem, stablecoins anchored by traditional world currencies would lose their monetary policy independence and be reduced to a shadow of fiat money. Borrowing from Mundell’s Impossible Triangle Theory, exchange rate ~ free flow of capital ~ monetary policy independence cannot be achieved at the same time. On the blockchain, the free flow of stablecoins is not restricted, except for the self-defeating practice of restricting the circulation of stablecoins. When the stable coin has determined the free flow of capital and exchange rate, then the stablecoin easily becomes the shadow of the centralized fiat currency.

Customized Indexs as Anchors

This type of stablecoins achieves differentiation competitive from fiat currencies in terms of value anchoring. Because the infrastructure remains weak, off-chain prices are difficult to capture widely and reliably with cheap prices. In addition to anchoring a basket of commodity prices, index stablecoins also try to anchor on-chain asset prices, only to make smoothing of prices and reduce the volatility of assets. This type of index-anchored stablecoin is difficult to get market consensus. Even RAI, which was mentioned by Vitalik in his blog (and in a sense has gained the orthodoxy of ETH), is in fact difficult to scale up and develop scale advantages (today RAI only has a market cap of 6.6 million).

Algorithmic Stablecoins Competition

The Algorithmic Stablecoins Track that Contains the Risk of Centralization

The cost of financing in the traditional financial world continues to rise under the pressure of Fed tapering. Capital started to exit from the crypto world in an orderly manner. The total amount of stablecoins has dropped from 246.2 billion to 135.1 billion. The crypto market lacks liquidity, from AMM’s centralized liquidity algorithm, to margin and options trading, improving asset liquidity has been an immediate need for on-chain assets. Creating stablecoins is about providing liquidity. As the DeFi industry matures, a number of established DeFi institutions have joined the competition with their resources and brands. The catfish in the stablecoin blue ocean are Curve and AAVE.

Both Curve and AAVE are kings in the DeFi industry. Their TVL reached 502 million and 478 million respectively, ranked 3 and 4 in the DeFi protocol. The current stablecoins to be made by Curve and AAVE are over-collateralized stablecoins. The two protocols have such high protocol-controlled assets that they can reach the TVL size of FRAX, the second chair of stablecoins, if they can convert 30%. Furthermore, it is not known if Curve and AAVE will produce separate token incentive programs for their respective stablecoin projects. This is a condition that other stablecoin projects that grew up in the last cycle do not have.

Curve and AAVE bring more advantages than that.

Curve itself is the largest stablecoin exchange on the chain. Curve is particularly good at building multiple stablecoins into one pool, and Curve’s airdrop rights are held by veCRV holders. By channeling traffic for its own stablecoins through its own exchange, it can quickly build up sufficient liquidity. The core value of stablecoin is to provide liquidity, and Curve is a management tool for liquidity distribution, which can directly empower CrvUSD. In addition, Curve’s stablecoin will use clearing interval instead of clearing line. This serves as a backward-looking advantage that will reduce lender and protocol losses and eliminate liquidity risk in times of illiquidity. Finally, Curve will use its own oracle to quote collateral, which is more reliable compared to external oracle services.

Curve’s business is to cover the credit generation of currencies as well as the management of liquidity. Among the stablecoins that are not completely free from the cloud of centralization threat, I personally am most optimistic about Curve’s business. It has a bit more flexibility than USDT, USDC and can take the liquidity of other stablecoins in terms of exchanges. Because it gives up part of the pursuit of decentralization, it has certain advantages for fully decentralized stablecoins in terms of collateral selection, efficiency of credit generation, and stability of tokens.

AAVE has top 10 active users in DeFi ranking. Because it has been in the lending business for a long time, AAVE has a deep knowledge of collateral and risk. In the traditional lending business, AAVE has been able to limit the amount of lending given to the same collateral to be too high through governance. In the business of clarifying the market risk and liquidity risk of collateral, there is no difference between the AAVE committee in governing traditional lending and stablecoin creation. The ability of AAVE to generate stablecoins, on the other hand, can significantly reduce the cost of AAVE. GHO is designed to have multiple ways of generating stablecoins. This broadens the channel of stablecoin credit generation. As mentioned earlier, the stablecoin track is one with significant scale advantages, and if the blueprint of AAVE could be realized, it would be scary. But looking out from the blueprint, AAVE does not see centralization as a risk, and its competitors will eventually be centralized stablecoins like USDT, USDC, etc.

Currently lending on AAVE, for each token lent, AAVE has to pay a cost to its user. Aave is relatively only paying a cost for liquidity. This can be a good deal. Some stablecoins pay 0.5% to create a stablecoin liquidity pool on curve, which is considerably lower than the current minimum rate of 1.23% — the AAVE stablecoin deposit rate. There are many other benefits for AAVE to create its own stablecoin, GHO, such as the lack of fear of a liquidity run. The current AAVE design for interest rates is that when a token is lent out in large numbers and approaches its limit, the rate rises significantly. This is a barrier to prevent depositors from withdrawing without liquidity and incentivizes users to repay or deposit to provide liquidity. Owned stablecoin lending, on the other hand, is not limited by the size of the vault and does not affect the liquidity of other people’s deposits.

The old king of algorithmic stablecoins, MakerDAO faces fierce competition. In the case of not being able to cover its expense, the development of Spark, to provide DAI internal lending, savings and other application scenarios, is also an attempt to actively break through the scale bottleneck. The downside of DAI is very obvious: MakerDAO involves the RWA. MakerDAO buy realistic U.S. treasury bonds. Whether from the real world constraints or the purchase of Treasury bonds off-chain behavior is not subject to blockchain constraints so that there is a risk of default, DAI provided by MakerDAO are no longer trust-less stablecoins. DAI segmentation of users has no difference with USDT, USDC segmentation of users, and their users are not sensitive to the risk of centralization. According to MakerDAO’s own disclosure, it has a net loss of $9.4 million within a year.

The second ranked algorithmic stablecoin FRAX has the collateral assets USDC and USDC derivative assets. The centralization risk of FRAX is inherited to USDC, FRAX not only does not get rid of the centralized stablecoin, but also has the same risk as USDC do. FRAX issued 21,720,976 additional FXS in 2022, if according to the current market price of 9.78, then FXS financed $210 million from the market.

Conversely, according to Coinbase’s Q4 earnings report, USDC made $292 million in profits in one quarter in 2022. Tether gained $700 million in profits in Q4 2022.

The risk of stablecoins is that either the collateral can not cover the liabilities and be completely decoupled, or the collateral can completely cover the liabilities and stare at the dollar. A stablecoin is fully exposed to centralization risk as long as it is not fully decentralized. Both being exposed to centralization risk, one end of the spectrum is centralized stablecoin that does not shed its algorithm losing money at high cost year after year, making it difficult to scale up; the other end is a fully centralized collateralized stablecoin that is profitable year after year, gradually eating into the market share. The conclusion is obvious, fully decentralized stablecoins have completely incomparable advantages in terms of efficiency, business expansion. Algorithm stablecoin products which compete in the same track will die in the long run.

Some people imitate the blockchain impossible triangle to make a stablecoin trilemma for stable coins. It pits overcollateralized stablecoins, centralized stablecoins and algorithmic stablecoins against each other. The author is using tokens being minted as the boundary of the stablecoin system, and is dividing stablecoins by the method of minting them. Its capital efficiency only reflects in the collateral assets needed to mint a stablecoin.

[Figure 5] The Impossible Triangle of Stable Coins

I agree with the basic framework of the stablecoin trilemma. Decentralization, security and efficiency are always the pain points of decentralized products, corresponding to the unique characteristics of stablecoins: decentralization, stability and capital efficiency, respectively. The difference is that as a stablecoin business, it is the due diligence of the stablecoin project to compete for cryptocurrency orthodoxy and expand the scenarios of stablecoin use. Capital efficiency has to encompass these scenarios, which is why stablecoins tend to subsidize trading pairs. Considering the capital efficiency of a project requires a holistic view of costs and benefits. For example, the efficiency of using stETH for collateral is definitely higher than using ETH. Similarly, using Curve to build stablecoin liquidity is more efficient than Uni V2. Finding a popular trading pair to build liquidity is more conducive to achieving capital efficiency than a unpopular trading pair to build liquidity.

Among those decentralized algorithm stablecoins which give up decentralization, the entry of DeFi successors is a descending blow. Of these, I am more bullish on CrvUSD than.

Fully decentralized algorithm stablecoin track

Today, the majority of stable coins are tainted with the risk of centralization. Let’s take a look at the few remaining decentralized stablecoin projects that are currently fruitful.

Liquity, which has only ETH as its collateral asset and liquid trading pairs only benchmark decentralized tokens like WBTC and ETH. It is completely isolated from the interference of centralization. Liquidation is considered to be done through an automatic clearing pool, eliminating the possibility of margin call liquidation due to liquidity shortage. However, Liquity is less stable and lacks mechanism-based incentives for LUSD liquidity. The project does not understand that the liquidity of the stablecoin is the core value provided by the project. Token distribution is approaching its end (91% of tokens have been issued.) , but the market size is still not monopolistically dominant.

[Figure 6] LUSD scale is difficult to expand

[Figure 7] LUSD supply and demand are not out of balance

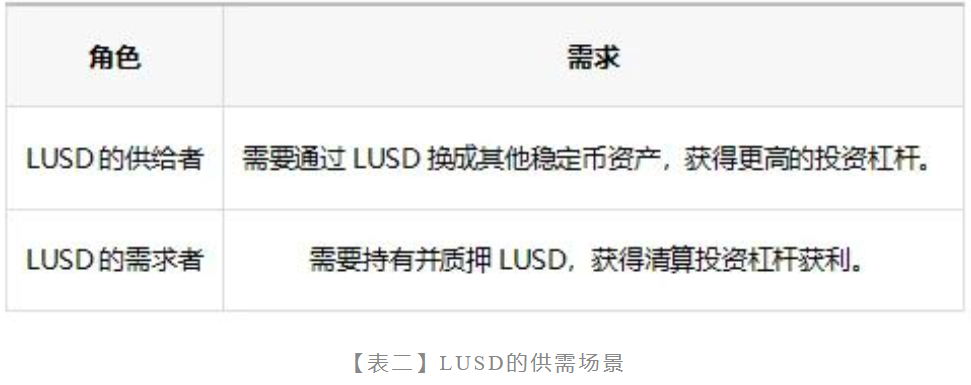

One of the highlights of Liquity’s design is the creation of additional demand for LUSD: LUSD adopts an overcollateralization mechanism. When the collateral is cleared, it is cleared through the LUSD in the collateral pool; while clearing, LUSD receives the collateral asset ETH at a discounted price. Historical data shows that the clearing is beneficial to LUSD collateralizers. Together with LUSD mining LQTY, 66.8% of LUSD goes into the collateral pool and the rest LUSD convert to other mainstream stablecoins via trading pairs. As a result, LUSD does not have the same “asset imbalance” in Curve’s trading pool as other smaller stablecoins.

[Table 2] LUSD supply and demand scenarios

Inverse.finance uses decentralized assets ETH and OETH as credit collateral to lend out USD stablecoins DOLA. The method used is also over-collateralization. The price stabilization mechanism still relies on arbitrage and interest rate control. However, the DOLA minted by inverse.finance is still pegged to USD as a shadow of USD. Inverse.finance has specifically designed a token DBR, using DBR as a tool for interest rate clearing. DBR’s price responds to the interest rate level of lending DOLA. The emergence of DBR makes the lending strategy more flexible and versatile. Attention is paid to the disclosure of information in the product design. The consideration is often only available in great large projects.

DOLA is designed with a bond model, users can get its platform token INV at a discount price by staking DOLA.

DOLA’s scale changes:

【Figure 8】Dola is gradually expanding in size

DOLA has the obvious disadvantage of having a lending rate of 4.92%, which is far higher than the interest rate offered by MakerDAO and higher than the LUSD, which claims to be interest-free. It is therefore difficult to scale up.

RAI is a customized index anchored, minted stablecoin. RAI uses redemption rates to regulate the amount of stablecoin supplied in the market, which in turn keeps the price of RAI close to the ideal price set by the system. RAI’s anchored price is free from the shadow of the dollar. However, the consensus cost of establishing a price is extremely high and must be large enough to have a scale effect. In the design of the stabilization mechanism, the overcollateralization mechanism, which is generally accepted in the market, is not used, which makes RAI has been gradually towards extinction. But as a radical explorer of decentralized stablecoins, RAI could still make a comeback if the blockchain world faces an increasingly pressing threat of centralization.

Conclusion

In summary, the stablecoin track, as long as it is not completely decentralized, faces complete centralization risk. As the stablecoin track facing the risk of centralization, the centralized stable coins led by USDT and USDC dominate and have formed a mature monopoly industry pattern.

In decentralized stablecoins:

First, the market share is small, the market is still in the early stage of development, the road is bleak, but full of hope.

Secondly, decentralized stablecoins have an inherent market.

Third, no decentralized stablecoin has the monopoly scale advantage of deterring competitors in the segmentation track.