Intro

A popular takeaway regarding the FTX drama has been that it was not a DeFi problem, but a TradFi one. It’s absolutely true that custody risks apply to CEXs and not DeFi. Yet, given the size of the collapse, we find it important to ask why, despite all their inherent custodial risks, CEXs continue to attract capital at such higher orders of magnitude.

Reflecting objectively on this question, it becomes evident that current infrastructure rails are immature across a number of fronts. When combined, these result in an inferior user experience compared to centralized solutions. We identify the major ones as follows:

Unsurprisingly, the existing shortcomings of these verticals also hint at where some of the biggest opportunities lie in crypto. In light of this, we’ll first summarize the current landscape across these four verticals, identify the current pain points, and highlight promising solutions/projects working to improve them.

In the second half of this report, we’ll cover an emerging crypto-native vertical that will remain at the center of blockchain operations – MEV.

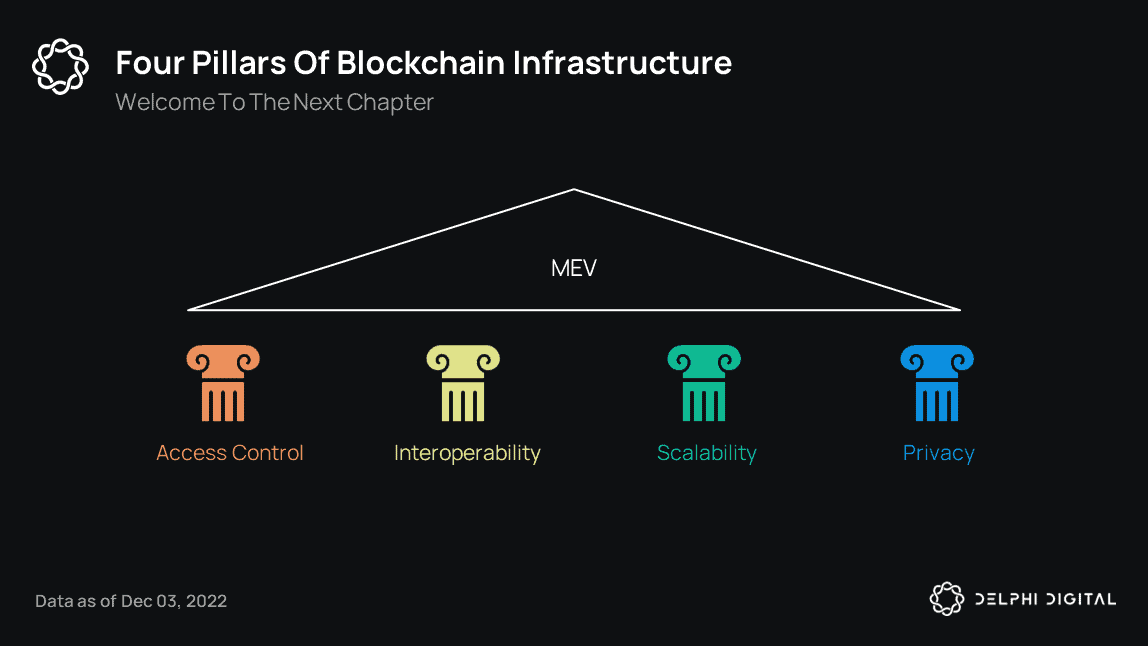

Access Control

The inconvenient UX of self-custody continues to be one of the primary reasons why people prefer custodial solutions. Today, access control in blockchains is static and binary. A typical user either has complete and exclusive control over her funds or has none. There is no in-between and no recourse if her private key is lost. This is understandably a very inconvenient experience for many.

Two ways to improve on the current UX of self-custody are smart contract wallets and MPC wallets. This post isn’t meant to be a comprehensive overview of MPC vs. smart contract wallets. Those interested in that can see this great overview.

In this post, we will summarize some main focus areas and trends across these verticals as well as highlight solutions gaining momentum.

Smart Contract Wallets

Smart contract wallet adoption is highly dependent on the VM and/or consensus layer design of the underlying chain.

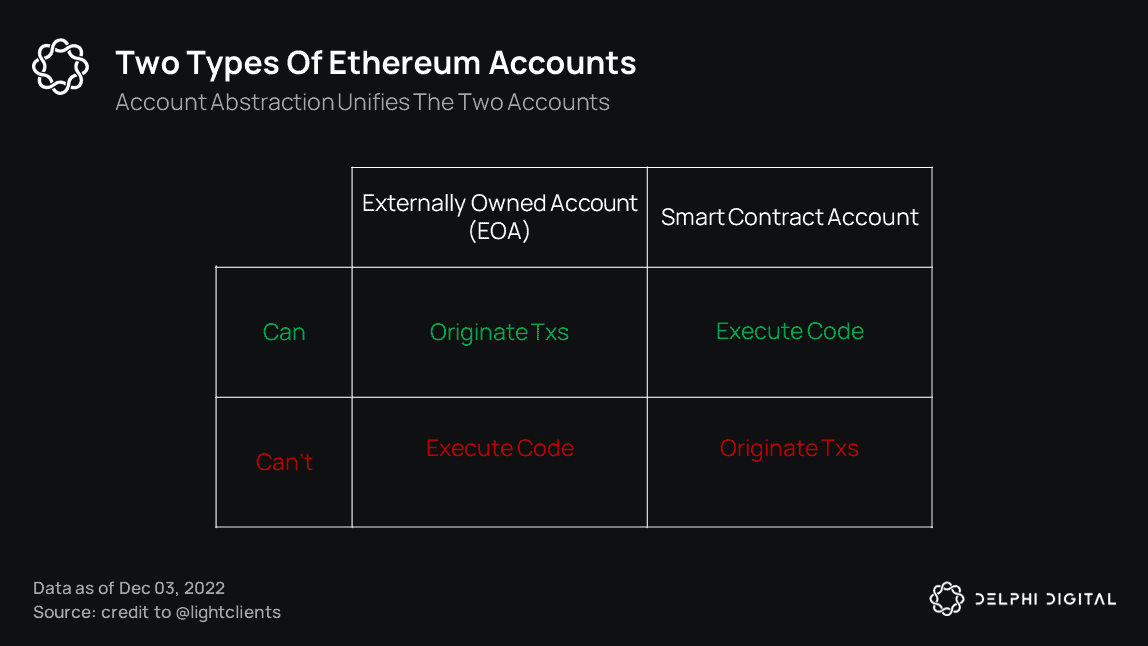

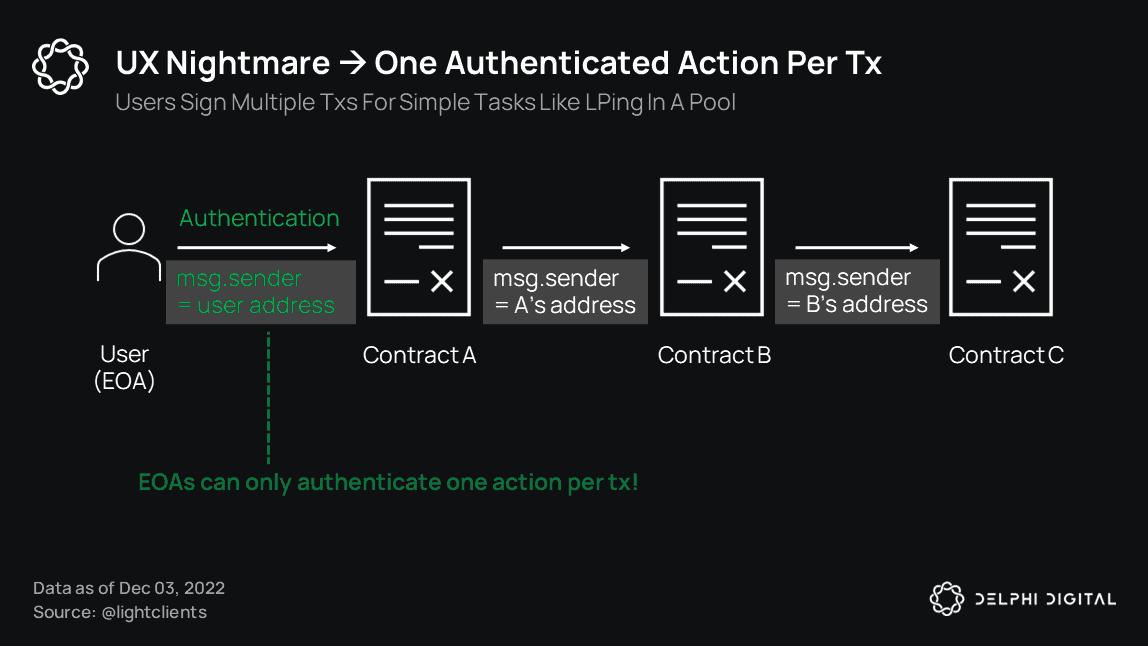

Today in Ethereum, smart contract wallets are regarded as second-class citizens. They can’t operate on their own; they need an externally owned account (EOA) like MetaMask to originate a transaction and pay for gas in order for them to trigger an action, and they are more gas-intensive.

The reality is that for smart contract wallets to be widely adopted, chains need to be redesigned accordingly. The Ethereum community has been actively seeking solutions here for many years. These efforts can be summarized as account abstraction.

Account Abstraction (AA)

Account abstraction is a true game changer. To understand it, we must first revisit how accounts work on Ethereum.

There are two account types on Ethereum: externally owned accounts (EOAs) controlled by private keys and smart contract accounts controlled by code. All transactions must originate from an EOA and may trigger smart contracts that execute arbitrary code.

Under account abstraction, EOAs and smart contract accounts that were previously separated become unified. Put another way, they are abstracted away. Let’s see how this works at a high level.

Under account abstraction, EOAs and smart contract accounts that were previously separated become unified. Put another way, they are abstracted away. Let’s see how this works at a high level.

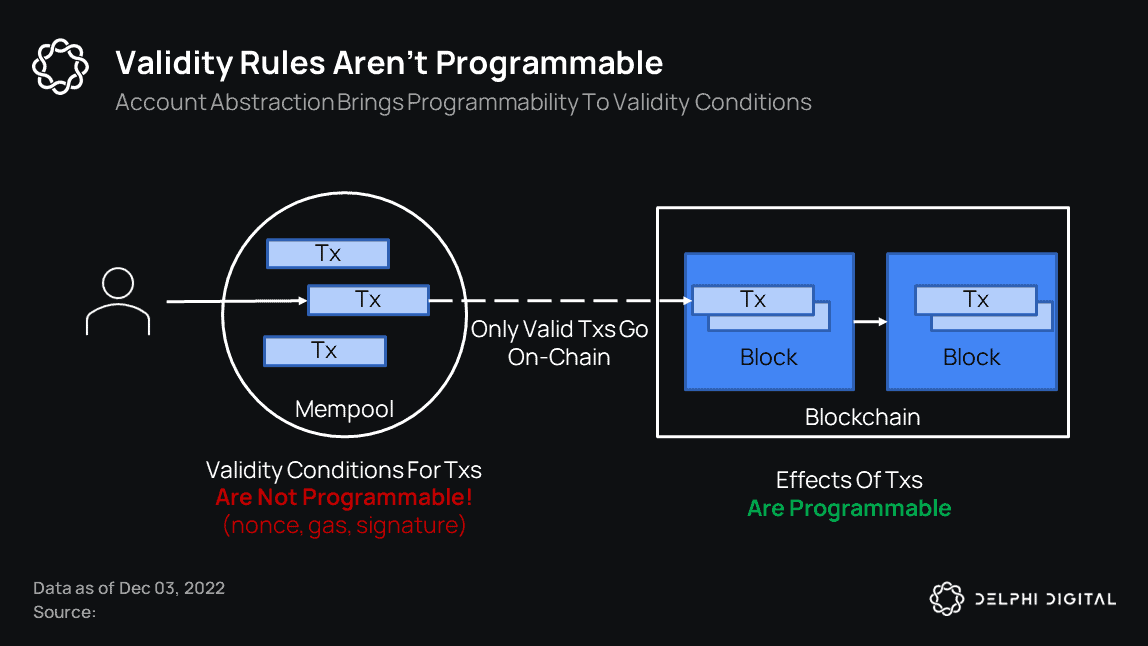

AA can be simply described as bringing programmability to transaction validity rules. Every transaction mined on Ethereum can trigger an arbitrary code stored in smart contracts. The results of transactions are therefore fully programmable. However, for transactions to be mined on-chain in the first place, they must conform to some validity rules. They need to have a proper nonce, gas amount, signature, and syntax.

Today, these validity rules are fixed and not programmable.

Account abstraction also allows validity rules to be programmable. Under AA, smart contracts not only determine the effects of transactions, but can also determine whether or not they are valid, and thus be the agents that authorize them.

Account abstraction also allows validity rules to be programmable. Under AA, smart contracts not only determine the effects of transactions, but can also determine whether or not they are valid, and thus be the agents that authorize them.

Motivations for Account Abstraction

For the end user, AA means a dramatic improvement in UX. Today, in the absence of native AA support, even the simplest UX needs are out of reach for on-chain users. For example, a typical Ethereum user has to sign three different transactions via MetaMask to LP on Uniswap – two to approve tokens, and a third one to deposit them.

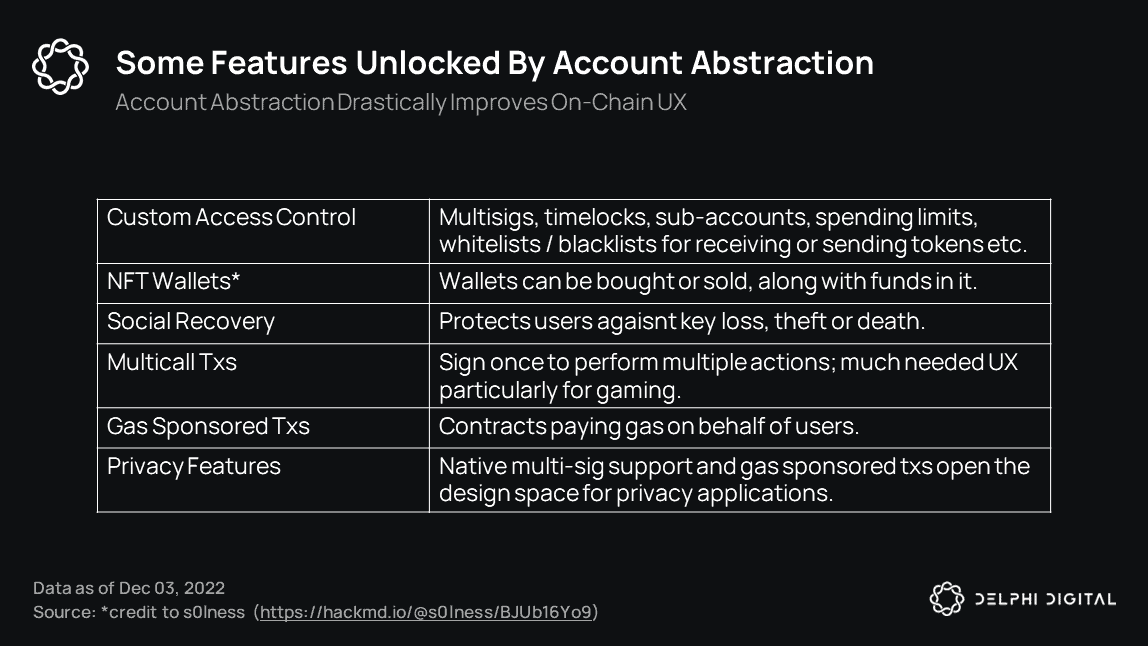

Smart contract wallets, combined with native AA, remove these frictions along with many others that currently make our lives harder. AA will allow for an on-chain UX approach on par with Web2 – without sacrificing self-custody.

Smart contract wallets, combined with native AA, remove these frictions along with many others that currently make our lives harder. AA will allow for an on-chain UX approach on par with Web2 – without sacrificing self-custody.

When Account Abstraction?

When Account Abstraction?

AA is nothing new. It’s been around since 2015. Leading smart contract wallets like Argent and Safe have been actively promoting and pushing for AA for many years. Yet, to date, the Ethereum developer community hasn’t been able to converge on a particular solution. This is because it’s not an easy problem to solve and can result in unexpected second-order effects.

Transaction validity rules protect the network against attacks; gas prevents spam, nonce prevents replay, and signature prevents theft. Under AA, it becomes harder to reason about these protections. Proper gas accounting, in particular, can become challenging and potentially expose the network to griefing and/or DDOS attacks.

Another challenge with implementing AA is breaking backwards-compatibility with existing applications.

Given these challenges, it’s fair to not expect Ethereum to natively support AA anytime soon. The good news is L2s can be free from backwards-compatibility constraints. Also, they have a much lower bar for social coordination. This allows them to act fast and benefit from all the work done on AA throughout the years.

Account-Abstracted L2s

zkSync and StarkWare are among the first L2s to have native AA support in their protocols, making their smart contract wallets quite powerful. Argent supports StarkWare and will also support zkSync once it launches. Cartridge is another wallet that leverages AA to enhance the on-chain gaming experience on StarkWare.

Another chain that supports native AA in its VM is Fuel. FuelVM is designed to support UX-enhancing features previously mentioned such as batched transactions, native multisig support, gas-sponsored transactions, privacy-enhancing features, etc.

MPC Wallets

So, we have seen that smart contract wallets mostly rely on protocol-layer changes to gain adoption, but what about MPC wallets?

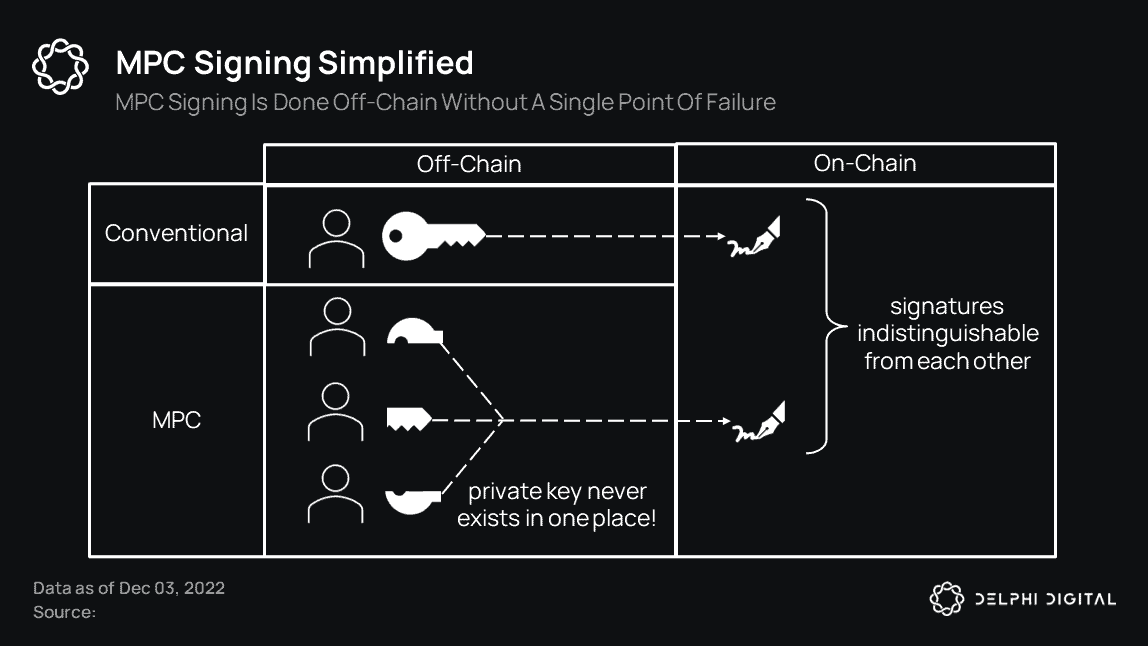

In very simple terms, MPC wallets allow multiple parties to collectively operate a public-private key pair without a single point of failure. The private key is split, encrypted, and held among multiple parties as secret shares. The private key does not exist in its entirety on a device anywhere in the process. Yet, a threshold of parties can generate a signature corresponding to the key using their secret shares.

A signature generated using MPC is indistinguishable from a signature generated by an EOA. This unique property of MPC brings numerous advantages. First of all, it makes them first-class citizens just like EOAs. Unlike smart contract wallets, MPC wallets don’t need to wait for protocol-layer changes to reach their full potential and they don’t have extra gas overhead compared to EOAs. MPC solutions are also domain-agnostic. They can easily apply to all chains and even be extended to Web2 platforms.

A signature generated using MPC is indistinguishable from a signature generated by an EOA. This unique property of MPC brings numerous advantages. First of all, it makes them first-class citizens just like EOAs. Unlike smart contract wallets, MPC wallets don’t need to wait for protocol-layer changes to reach their full potential and they don’t have extra gas overhead compared to EOAs. MPC solutions are also domain-agnostic. They can easily apply to all chains and even be extended to Web2 platforms.

However, consumer hardwares manufacturers like Ledger and Trezor don’t support MPC. Ledger has extensively written on why they don’t consider MPC as a truly ready solution, highlighting numerous security issues. Lack of consumer hardware support has held back MPC wallets from getting adopted by retail. So far, MPC has (for the most part) been used as an enterprise solution. Albeit, mature non-custodial MPC wallet solutions like Zengo are changing this landscape and paving the way to bring MPC to the reach of average consumer.

Another notable progress in this direction is web3auth’s MPC SDK. Thanks to advancements in MPC, distributed key signing in compute constraint envrionments like browsers is becoming practical. As such, web3auth has recently been able to allow an sdk for wallets/dapps to offer self-custody using multi-factor authentication powered by MPC.

Note: This paragraph was edited post-publication on 01/06/23

MPC-Based Key-Management Networks

In the last two years, significant funding has been applied towards new forms of MPC solutions catered towards crypto users. These solutions can best be defined as decentralized MPC-based key-management networks. Lit Protocol, Entropy, and the newer protocol Odsy fit into this category.

Entropy and Odsy: Entropy and Odsy are app-specific blockchains with smart contracts where the user’s key pair is split and shared between validators of the chain and the user. A valid signature can be formed when both parties (validators and users) sign their secret shares. Users can instruct validators to sign their shares when some arbitrary conditions in the smart contract’s code are satisfied. This opens up the design space for truly programmable and dynamic access control; typical examples include conditional payments, spending limits, whitelists, etc. More sophisticated and interesting use cases are also possible; DAOs may manage their internal policies by dynamically adjusting privileges for members. Illiquid assets like locked/bonded tokens can be traded on-chain, etc.

Given the complexity of their technical stacks, it’s hard to estimate timelines for these protocols. However, our best guess is that, as the more mature of the two, Entropy is likely to launch within the next year.

Lit Protocol: In Lit Protocol, there is a single private-public key pair. The key generation and distribution happens among Lit nodes when users mint an NFT on-chain. Whoever holds the NFT can instruct Lit nodes to sign transactions with the generated key pair.

The access control managed by Lit nodes can be programmed through Lit actions, which can be thought of as Lit’s version of smart contracts; they are immutable Javascript code that live on IPFS and can be deployed by anyone. By using Lit actions, users can create access control logic for all sorts of use cases, including conditional payments, recurring payments, automated on-chain actions, etc.

A unique ability of Lit actions is that they make HTTP requests. Thus, unlike smart contracts, they can also access and work with off-chain data. This allows Lit to unlock exciting use cases that bridge the Web2 and Web3 worlds. An exciting category of use cases involves bringing Sybil control to Web2; think NFT-gated Shopify stores, Tesla/Airbnb doors, Twitter polls, Google Drive files, etc. Plenty of innovative use cases can be found here.

Lit Protocol currently operates as a centralized network. Starting next year, it will transition to a federation and then to a fully permissionless network where nodes stake protocol tokens to participate in the network. Lit Protocol intends to use Celo chain for staking.

Limitations of MPC-Based Networks

MPC also has fundamental limitations which we haven’t discussed yet. Broadly speaking, what’s common in decentralized MPC protocols is that users manage key pairs with a decentralized network of nodes. As we saw, the benefit here is programmable and dynamic access control, and users typically have to sign their own shares to authorize transactions (which means nodes can never steal funds).

However, there is an inherent trade-off. While users don’t rely on nodes for safety of funds, they may rely on them for liveness, i.e., it’s possible for user funds to get stuck if nodes stop responding to them. Workarounds typically include introducing crypto-economic security, more cryptography to discourage node collusion, and recovery methods. Inarguably, this brings more complexity into the protocol.

Access Control Wrap-Up

To summarize, we think smart contract wallets combined with native account abstraction result in the most secure, clean, and flexible UX for on-chain self-custody. However, they will take significantly more time, and the progress will differ vastly from one chain/VM to another. In the meantime, decentralized MPC solutions can offer a hacky way to get there faster. While they can’t offer the full flexibility and security that account abstraction promises, they are domain-agnostic and can therefore unlock new use cases that span across all chains and even expand to Web2. In reality, it’s likely for both solutions to complement each other.

Cross-Chain Interoperability

The multi-chain world we live in today is living proof that a single chain can’t serve everyone’s needs. Cross-chain interoperability is thus at the heart of scalability.

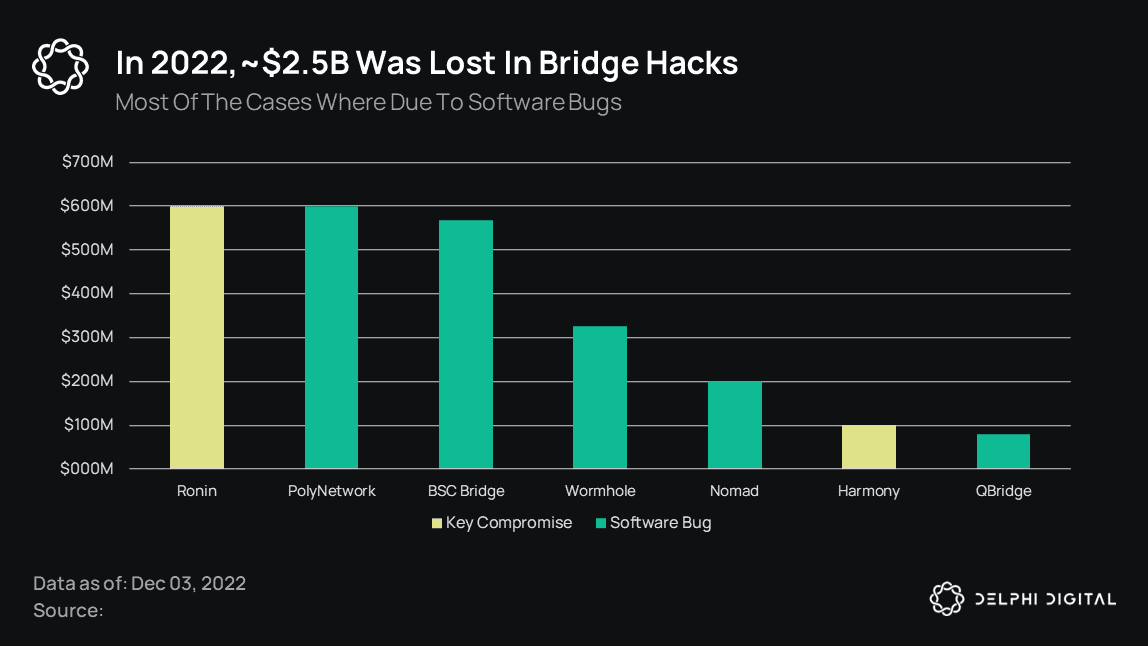

Unfortunately, bridge security remains a major pain point and a fundamental problem for the industry. The last two years have shown that bridges are scary. In aggregate, bridge hacks have resulted in close to $2.5B of losses.

Most of these hacks have been due to implementation bugs, and some have been due to key compromises which can be seen as part of the security model of the bridge (no fallback mechanism).

Most of these hacks have been due to implementation bugs, and some have been due to key compromises which can be seen as part of the security model of the bridge (no fallback mechanism).

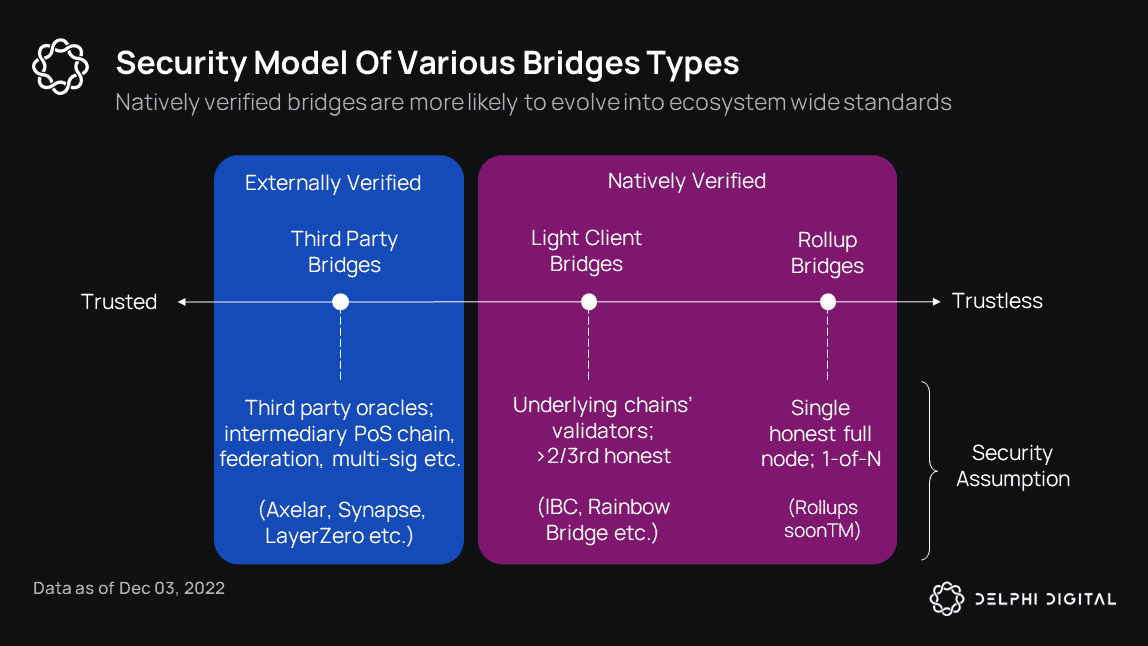

Natively Verified vs. Externally Verified Bridges

When evaluating bridge designs, it’s tempting to see the security model and implementation as disjointed factors. However, moving forward, we would argue that the healthier (and perhaps more realistic) approach is to consider them in conjunction.

At a high level, bridge designs can be categorized into three buckets: third party, light client, and rollup bridges. Third-party bridges are externally verified, while light client and rollup-based bridges are natively verified.

Most bridges in the last two years have been externally verified bridges. These bridges are often developed and maintained by arbitrary teams each building their own designs. There is little to no cooperation between them in terms of code scrutiny. Furthermore, because they compete for market share, they are inclined to boost TVL by handing out rewards during the first few days of launch. This leads to a perfect environment for black hats.

Most bridges in the last two years have been externally verified bridges. These bridges are often developed and maintained by arbitrary teams each building their own designs. There is little to no cooperation between them in terms of code scrutiny. Furthermore, because they compete for market share, they are inclined to boost TVL by handing out rewards during the first few days of launch. This leads to a perfect environment for black hats.

This is why we no longer think it’s a good idea to consider bridge designs in isolation from how they are likely to be implemented. We know by now that the threat model is nation state-level black hats. While we can never be certain that vulnerabilities don’t exist, the winning solutions are likely to be the ones that encourage maximum cooperation and code scrutiny. This brings us to natively verified bridges.

Natively Verified Bridges Rising as Standards

The antidote for bridge hacks is standardization. Natively verified bridges (light client and rollup-based) have notable characteristics that make them more likely to evolve into standards than externally verified bridges.

Natively verified bridges not only function as general message-passing protocols, but also serve other fundamental needs and primitives such as mobile wallets, fast syncing, reducing reliance on centralized RPC services, etc. Given that they are ecosystem-centric, natively verified bridges are relied upon and scrutinized by a larger number of teams and developers in their respective communities. Their roadmaps revolve around developing ecosystem-wide standards considering the maximum mutual benefit of ecosystem participants.

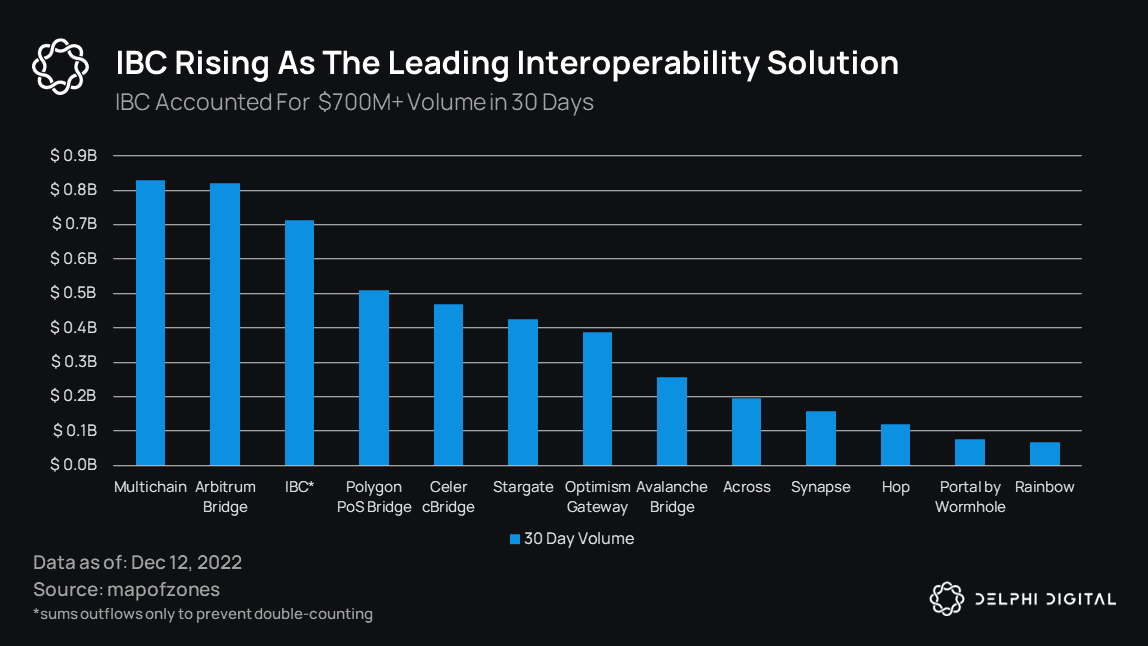

Inarguably, the most successful example of this is IBC. IBC isn’t immune to implementation bugs, but its development greatly benefits from the mindshare and attention it receives from a large number of diverse Cosmos teams. Considering how a critical incident was flagged and patched recently, we can count this as an important factor for its survival.

IBC’s Traction

IBC had undeniable success in 2022, emerging as the canonical bridge for Cosmos. Today, 53 chains rely on IBC to pass messages to each other. In the last 30 days, IBC accounted for more than $0.7B of cross-chain volume and was ranked third-highest in volume after Multichain and Arbitrum.

Given its existing network and lindy effects, there is now increasing interest in extending IBC to Ethereum and other ecosystems.

Given its existing network and lindy effects, there is now increasing interest in extending IBC to Ethereum and other ecosystems.

IBC to DotSama

IBC’s first extension beyond Cosmos may be through the Centauri bridge developed by Composable Finance. Centauri will bring IBC to DotSama (Polkadot and Kusama). The first implementation will be between Picasso (Composable’s Kusama parachain) and Cosmos chains early next year. Centauri is well positioned to become the canonical bridge between the Substrate and Cosmos chains.

IBC to Ethereum

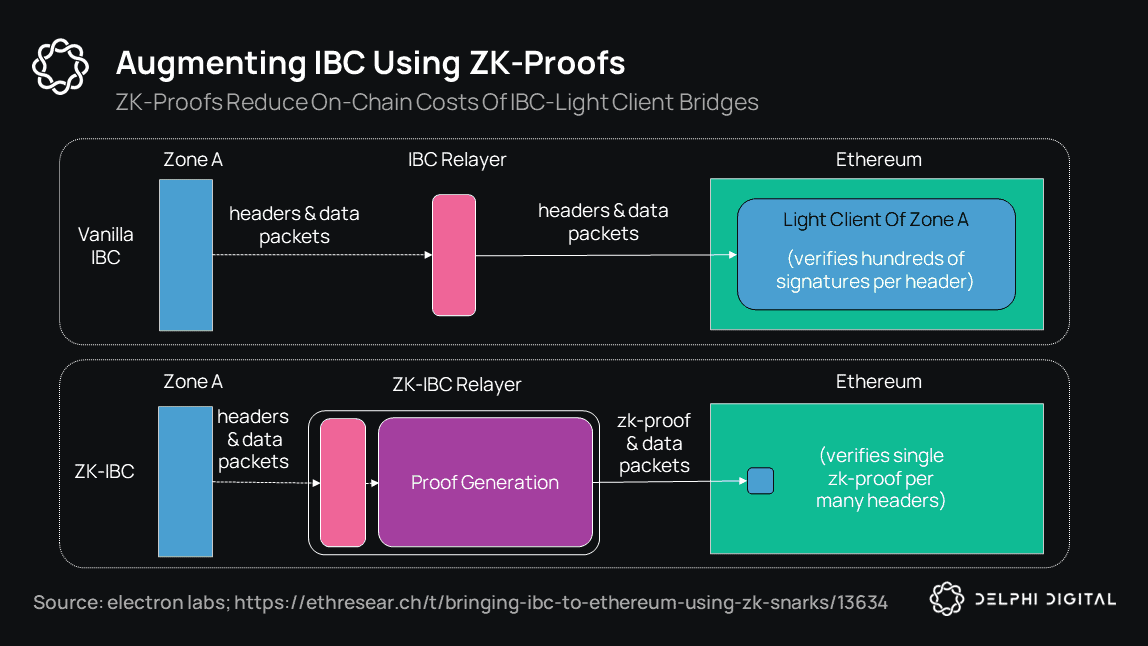

A major challenge for light client-based bridges is cost of verification. The fundamental limit here is that for each block where the source chain sends a message, the destination chain needs to verify the header of the source chain. This involves the verification of validator signatures.

For example, if the source chain is a Cosmos chain with 150 validators, the destination chain verifies 100+ signatures (>2/3 validator votes) on-chain for every block where cross-communication takes place. This can be astronomically costly if the destination chain doesn’t natively support the signature scheme of the source chain and has expensive gas.

This is the key reason why the Cosmos<>Ethereum IBC connection has historically been infeasible. However, thanks to recent advancements in zk-tech, there is now a viable path to bringing IBC to Ethereum!

Zero-Knowledge IBC

Instead of Ethereum smart contracts directly verifying the header on-chain, the computation of verifying the header is done by off-chain provers using beefy machines. These provers then generate a succinct validity proof that can be cheaply verified by Ethereum smart contracts. This technique is coined as consensus proofs. Notable pioneering teams here include Electron Labs and Polymer Labs.

For the sake of clarity, the use of zk-proofs doesn’t change the existing trust model of the bridge. The proofs are used to reduce the verification costs of proving consensus *without* introducing new trust assumptions. Our light client-based bridge would still rely on source-chain consensus (>2/3 validators) for the safety of funds. Thus, it would still not be as trust-minimized as rollup bridges (which prove every state transition). That said, given its narrower scope, proving consensus can perhaps gain momentum much sooner with widespread usage of zk-proofs.

For the sake of clarity, the use of zk-proofs doesn’t change the existing trust model of the bridge. The proofs are used to reduce the verification costs of proving consensus *without* introducing new trust assumptions. Our light client-based bridge would still rely on source-chain consensus (>2/3 validators) for the safety of funds. Thus, it would still not be as trust-minimized as rollup bridges (which prove every state transition). That said, given its narrower scope, proving consensus can perhaps gain momentum much sooner with widespread usage of zk-proofs.

Augmenting IBC bridges with zk-proofs is very exciting because it can bring IBC to any smart contract blockchain lacking native IBC support. There is even a possible future where consensus from multiple chains could be aggregated into a single proof using recursive zk-proofs. This would drive the amortized costs of cross-chain messages further down and become the ultimate solution for the relayer incentivization problem of IBC. Perhaps this gives us a glimpse into what IBC will look like in its end state.

ZK-Based Ethereum Light Clients

So far, we have discussed how Tendermint consensus can be cheaply verified on other ecosystems. But what about verifying Ethereum consensus?

An on-chain light client for Ethereum was out of the question for PoW Ethereum. However, with Ethereum transitioning to PoS and advancements in zk-proofs, this has recently become possible.

In fact, tremendous progress has been made this year by pioneering teams like Succinct Labs and zkBridge. Both teams are close to having working products. Succinct Labs has already demonstrated a two-way on-chain light-client bridge between Ethereum and Gnosis chain in testnet. Gnosis was chosen because it has the same consensus protocol as Ethereum. Similarly, zkBridge has built an initial version of a SNARK-based Ethereum light client.

Cross-Chain Apps

Shifting our focus to the application layer, one trend we expect to see next year is cross-chain apps. Today, the application layer is multi-chain but it’s not yet cross-chain. Next year, we expect to see the first major cross-chain apps. We see this playing out in multiple ways.

- Siloed deployments composing with each other.

Today, major dApps exist across multiple chains. This is especially common in the EVM world with blue chips like Uniswap, Aave, Synthetix, and Compound. However, these instances are mostly siloed.

There are multiple reasons for this. First, it is mostly an artifact of the bull market where teams prioritized market share above all else, with little focus given to cross-chain composability. DeFi protocols looking for bridge partners had in-depth discussions yet struggled to commit given there were no clear winners. Bridge hacks exacerbated the problem even further. However, given the bull-market hype is seemingly over, this landscape may change next year.

One catalyst here will be Chainlink’s cross-chain interoperability protocol CCIP. For large communities like Aave, Synthetix, and Compound, it’s easier to decide to rely on Chainlink as a cross-chain interoperability partner given that they already rely on it for price feeds. This would further reinforce Chainlink’s standing in DeFi.

LayerZero is another protocol that’s well positioned here. Their recent integration with Chainlink oracles can be a catalyst, as applications can permissionlessly spin up bridges with Chainlink oracles. We also note that Sushi is already using LayerZero through its integration with Stargate earlier this year. Rage Trade is another promising derivatives platform that will use LayerZero for its cross chain offerings.

2. Existing cross-chain applications offering more use cases.

A cross-chain protocol well positioned to capitalize on its already established market fit is THORChain (see here for our report from April). THORChain is making new integrations with existing DEXs and wallets. The goal here is to abstract THORChain away from user flow. Users can use their favorite wallets/DEXs without even realizing that their cross-chain swaps are going through THORChain. Pangolin, Trader Joe, and Kyber were integrations completed earlier this year. Very recently, a major integration was announced with Trust Wallet, one of the biggest wallets in terms of user base.

Aside from integrations, THORChain is also expanding its cross-chain offerings. It recently launched a savings product, which can be thought of as a decentralized version of BlockFi. It’s currently the only major DeFi product that offers yield on native Bitcoin. Next year, THORChain plans to deploy a new cross-chain lending/borrowing product with zero liquidations and interest. With more integrations and offerings, THORChain is taking important steps towards becoming an economically sustainable protocol (we note that most of these THORFi offerings change the tokenomics of RUNE in an unprecedented way, and thus may involve unforeseen risks that must be carefully considered).

Another protocol well positioned here is Axelar. Axelar is not an app-specific protocol like THORChain, but a hub for generic message-passing. Axelar is uniquely positioned because it supports Ethereum and other EVM chains as well as IBC. So far, it has been a major contributor to Cosmos by acting as a direct hub between Ethereum and numerous Cosmos appchains. Following its launch early last year, Axelar was selected as the canonical bridge for Osmosis, and has since been among the top chains in terms of IBC volume. Next year, Axelar can potentially benefit greatly from increased Cosmos adoption.

3. New applications starting cross-chain from the get-go.

Finally, there is a new set of dApps that will start cross-chain from the get-go. Some notable ones which chose this path include Mars Protocol, Prime Protocol, Composable Finance, and Rage Trade.

Mars and Prime are both cross-chain lending/borrowing applications enabling users to borrow on one chain against their collateral on another chain. Mars will be a Cosmos appchain leveraging advanced features of IBC such as interchain accounts and queries. Prime will be offering a similar use case but targeting EVM L1s and L2s and leveraging Axelar for cross-chain interoperability.

Scalability

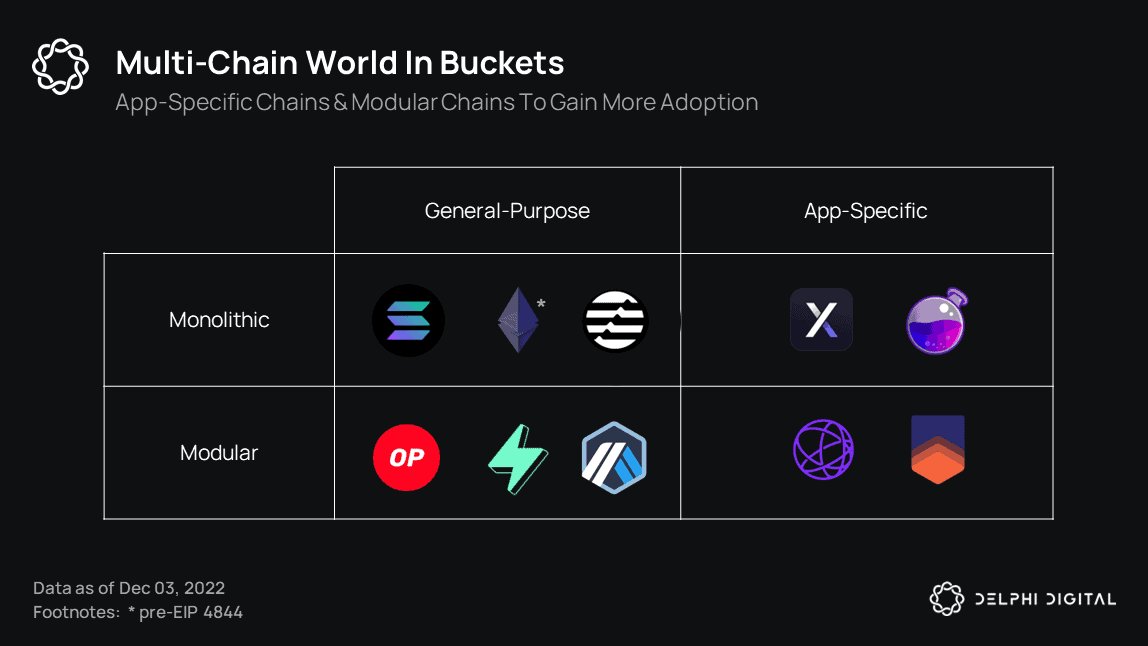

Scalability is a moving target. Much like the internet, blockchains will continue to struggle to scale as they onboard new users.

Put another way, scalability solutions take different shapes and forms at different levels of user demand. Today, various different blockchain architectures coexist to accommodate the current user load. It’s possible to categorize these architectures into four buckets.

Today, user adoption is mostly dominated by general-purpose monoliths. As we move forward, we expect this to gradually change and for user adoption to shift towards appchains and modular chains. Given their maturity, we predict appchain adoption to materialize in the near-term, perhaps within the next 1-3 years, and imagine modular chains as the end state architecture where blockchains become mainstream. A comprehensive overview of the motivations behind the appchain and modular chain theses can be found in Delphi Labs’ Finding a Home For Labs report and Delphi Ventures’ Dawn of the Modular Era post.

Today, user adoption is mostly dominated by general-purpose monoliths. As we move forward, we expect this to gradually change and for user adoption to shift towards appchains and modular chains. Given their maturity, we predict appchain adoption to materialize in the near-term, perhaps within the next 1-3 years, and imagine modular chains as the end state architecture where blockchains become mainstream. A comprehensive overview of the motivations behind the appchain and modular chain theses can be found in Delphi Labs’ Finding a Home For Labs report and Delphi Ventures’ Dawn of the Modular Era post.

This is, however, not to say that we expect general-purpose monoliths to die off anytime soon. While we see a shift towards modularity and appchains over time, we recognize that there is a benefit to the synchronous composability and permissionless innovation in the sandboxed environments that general-purpose chains enable. By no means do we expect these to go away completely.

Indeed, we expect these different designs to coexist for a very long time. There will be winners and losers in each category. In this post, we will highlight the ecosystems and projects that (in our opinion) are likely to thrive in their respective categories.

For general-purpose monoliths, we still consider Solana the biggest contender in this category despite all the hits it took after the FTX implosion.

What’s Next for Solana?

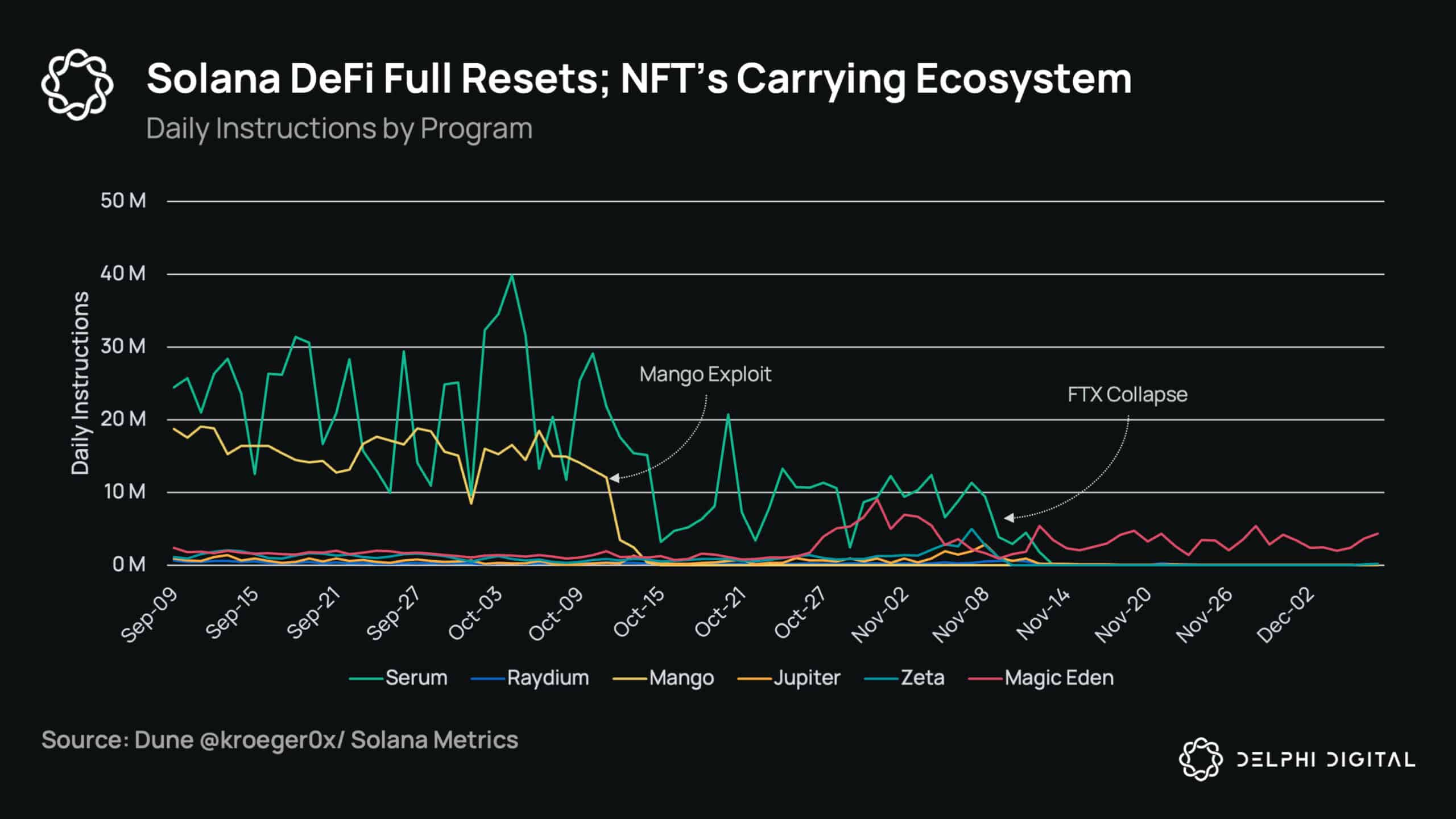

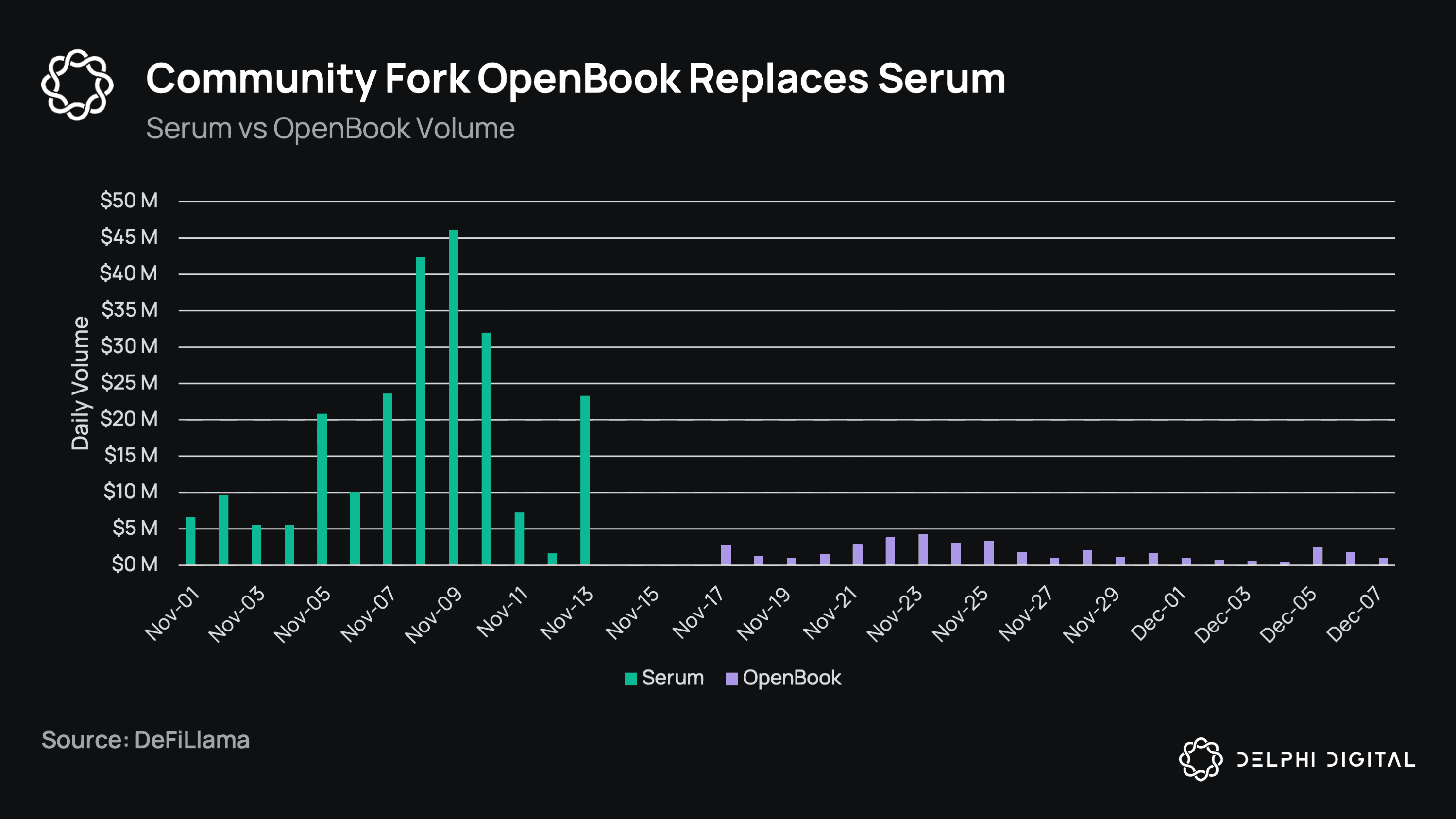

The recent FTX collapse hit the Solana ecosystem harder than any other. Saying that Solana DeFi has had a rough couple of months is an understatement. In October, Solana’s largest DeFi protocol (Mango Markets, >$100M TVL at the time) was exploited, with the FTX collapse happening a month later. During the fallout, there were also concerns around FTX-led Serum, so the community came together to fork it and take control, deploying a new CLOB DEX called OpenBook. Since most of Solana DeFi was built on top of Serum, many DeFi protocols had to pause/go offline due to the lack of liquidity. Solana DeFi has truly gone through a full reset, with NFT activity responsible for retaining Solana users for the time being. So, should we write Solana off as dead, or are there catalysts on the horizon to turn it around?

We should start by noting that Solana is becoming a more modular ecosystem in and of itself, not with respect to the Solana chain, but with the Sealevel Virtual Machine (arguably Solana’s best innovation) becoming a rollup standard through Eclipse and Nitro. If you believe that a big part of Ethereum’s moat is the EVM, then the SVM becoming widely adopted should be no different for Solana, and the data backs this up.

We should start by noting that Solana is becoming a more modular ecosystem in and of itself, not with respect to the Solana chain, but with the Sealevel Virtual Machine (arguably Solana’s best innovation) becoming a rollup standard through Eclipse and Nitro. If you believe that a big part of Ethereum’s moat is the EVM, then the SVM becoming widely adopted should be no different for Solana, and the data backs this up.

Outside of Ethereum, the Solana Web3-developer package is the most widely adopted. Adoption has also continued to increase week over week, from 87k weekly downloads a year ago, to 200k in June, to 365k the first week of November, and most recently to 420k the first week of December. It has continued its consistent uptrend even with FTX’s collapse.

Besides SVM, there are reasons to be constructive on the Solana L1 itself.

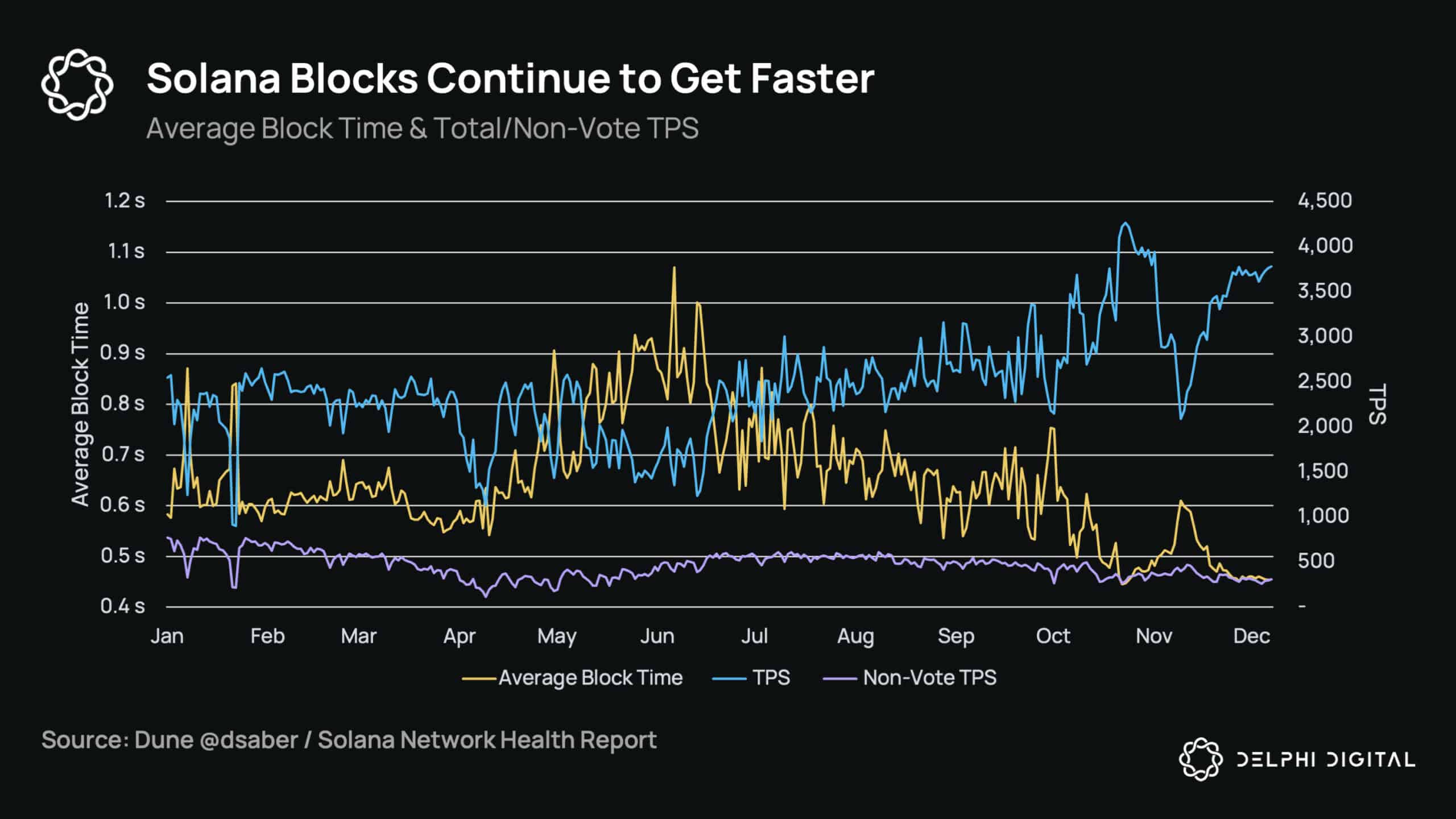

First, network performance has been getting better over time. Average block times on Solana have come down significantly over the last half-year. While some of this is due to a higher vote/non-vote transaction ratio (as votes are less computationally demanding), there have also been numerous software upgrades to the network. The NFT minting/spam issue that took Solana offline on multiple occasions has not impacted the chain to the same degree it did in the past, and it should only keep getting better with solutions like QUIC, fee markets, Jito, and Firedancer all going live.

There were still some performance issues during the FTX collapse (like publisher oracle updates not going through), but the chain performed much better than it would have six months ago and stayed up throughout the chaos and massive bot liquidations stressing it. While non-vote TPS are down, this is mainly due to lower overall activity – something we’re seeing on all chains, not just Solana.

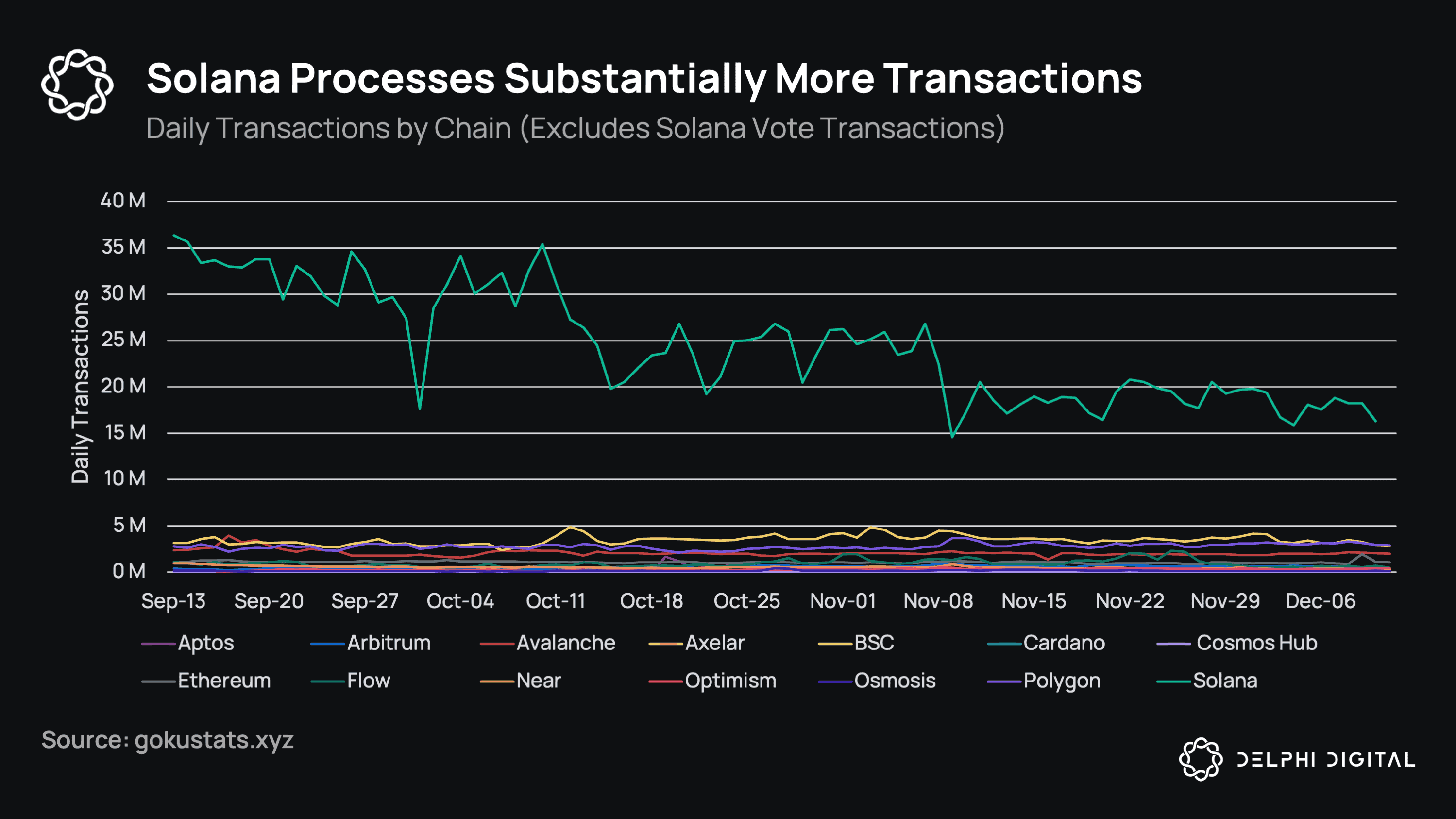

Still, with ~300 non-vote TPS, and removing the ~100 from oracles, Solana is doing ~200 real TPS, significantly ahead of all other chains. Their 15-20M non-vote transactions/day are still in a league of their own when compared to other blockchains.

Still, with ~300 non-vote TPS, and removing the ~100 from oracles, Solana is doing ~200 real TPS, significantly ahead of all other chains. Their 15-20M non-vote transactions/day are still in a league of their own when compared to other blockchains.

TPS is by no means a perfect metric, even when excluding votes/oracle transactions, but it’s still a rough signal for overall demand. We also shouldn’t completely disregard the oracle transactions, as Solana’s sub-second block times + cheap fees enable these fast oracle updates (something no other chain has live today) and, subsequently, unique products — specifically in the derivatives space.

TPS is by no means a perfect metric, even when excluding votes/oracle transactions, but it’s still a rough signal for overall demand. We also shouldn’t completely disregard the oracle transactions, as Solana’s sub-second block times + cheap fees enable these fast oracle updates (something no other chain has live today) and, subsequently, unique products — specifically in the derivatives space.

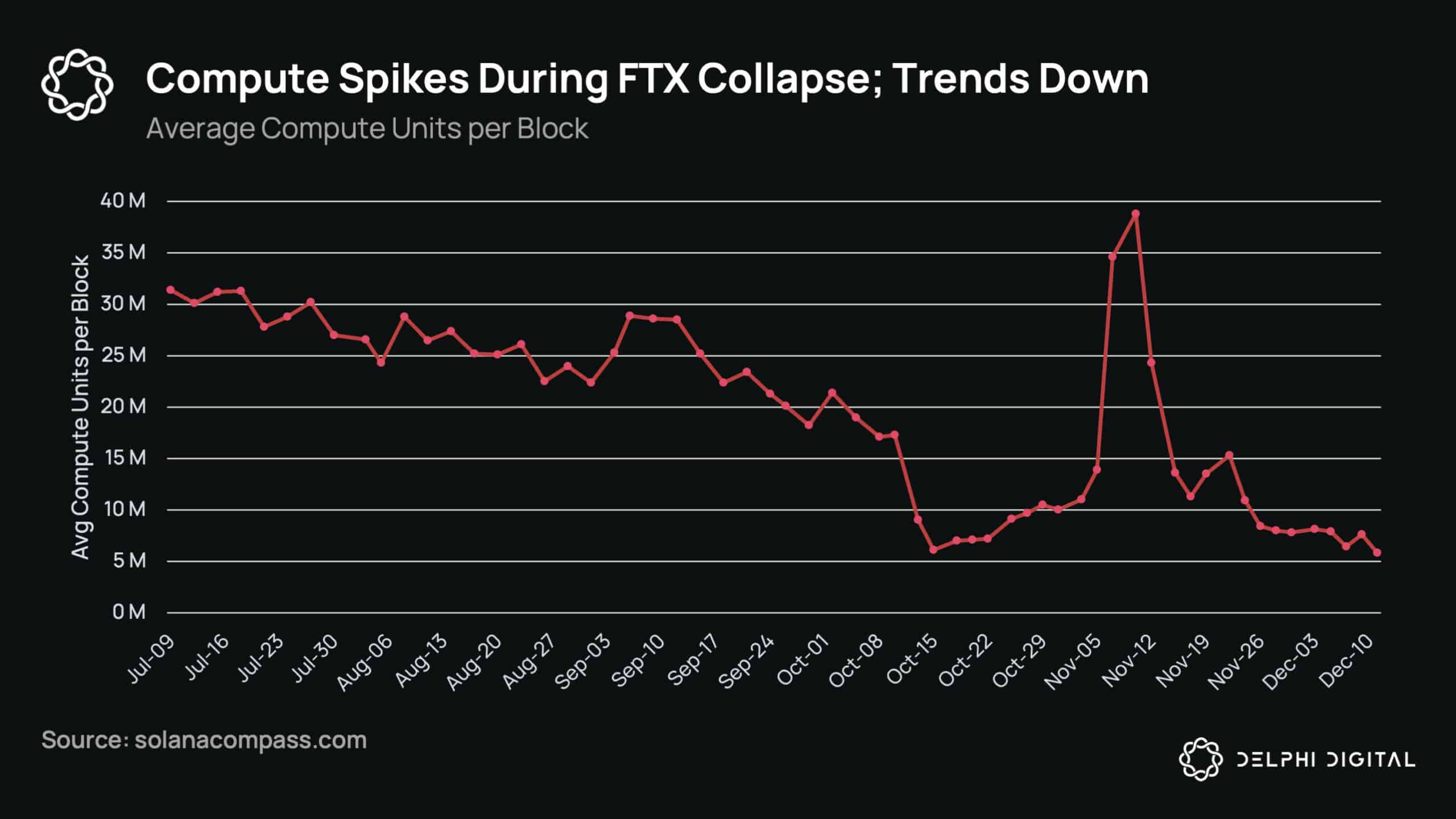

As a preferred metric for demand, we would look to compute units per block, which is a representation of both the number of transactions and their complexity. Seeing this metric go up over time will be a good signal for real usage of Solana. With Serum offline and overall demand for blockspace falling over the last few months (see Ethereum gas fees), this metric has settled into a lower floor. As a note to the chart below, Solana blocks have a max of 48M compute units per block.

More important developments are on the horizon, with the major ones highlighted here:

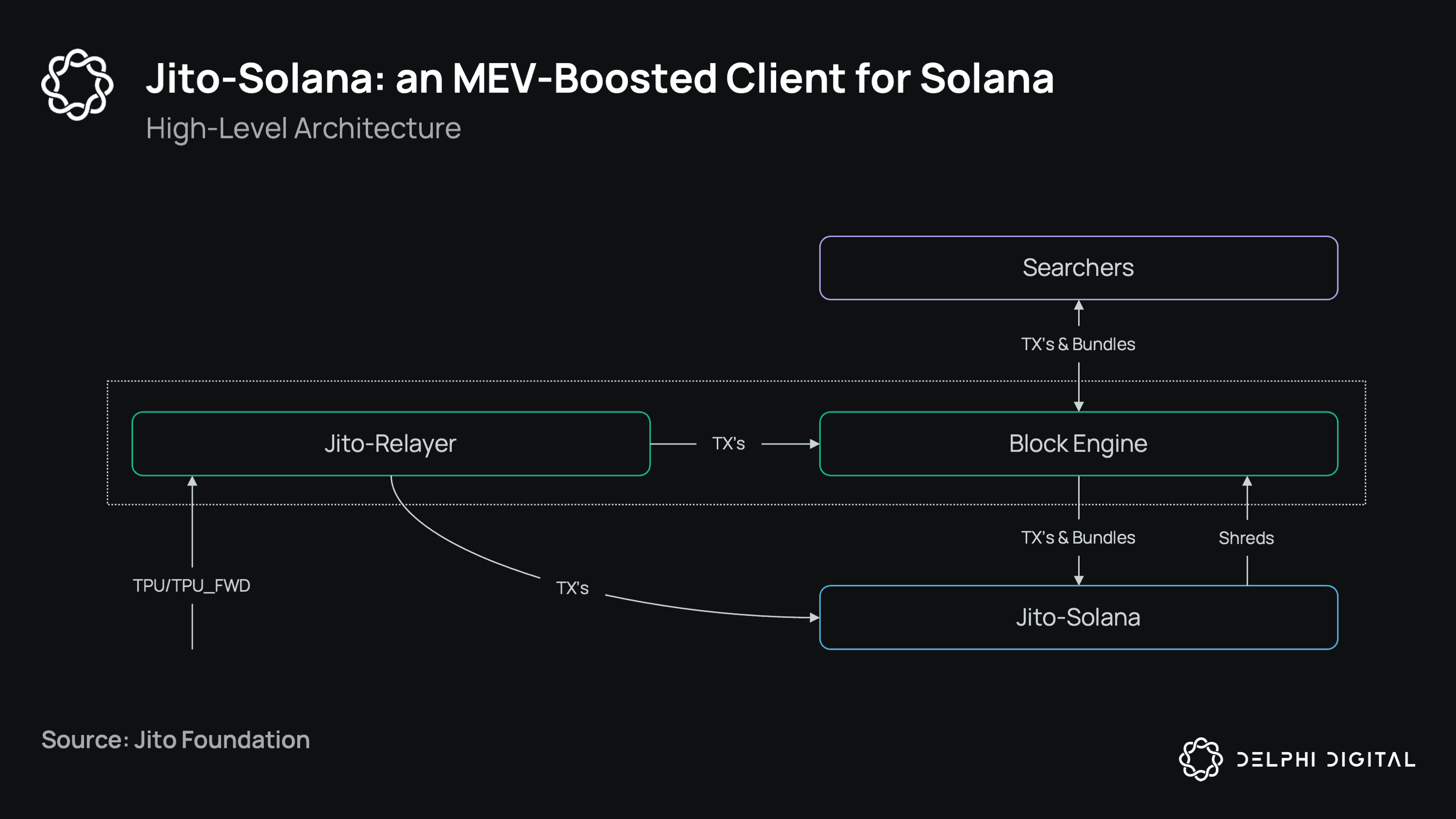

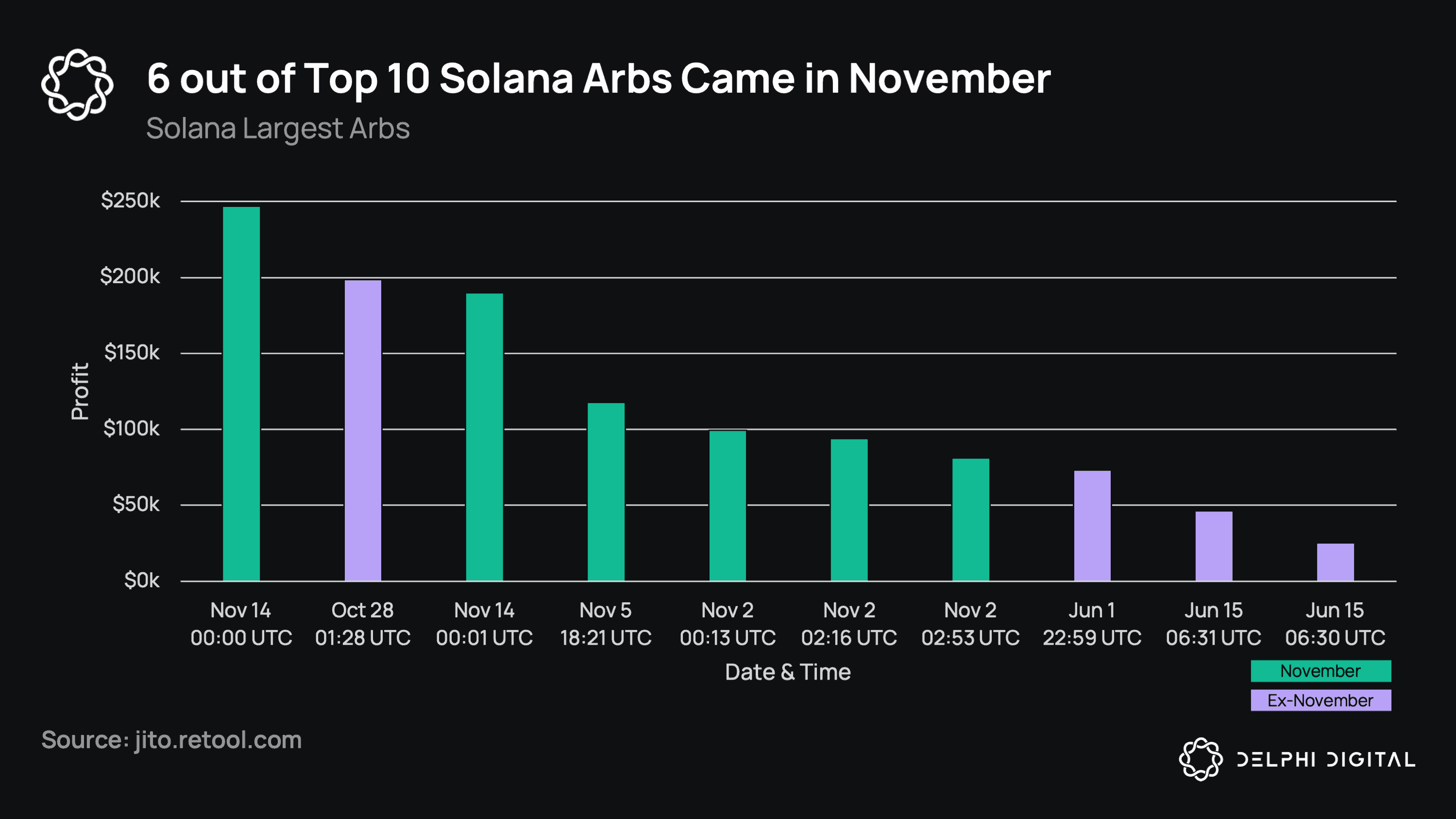

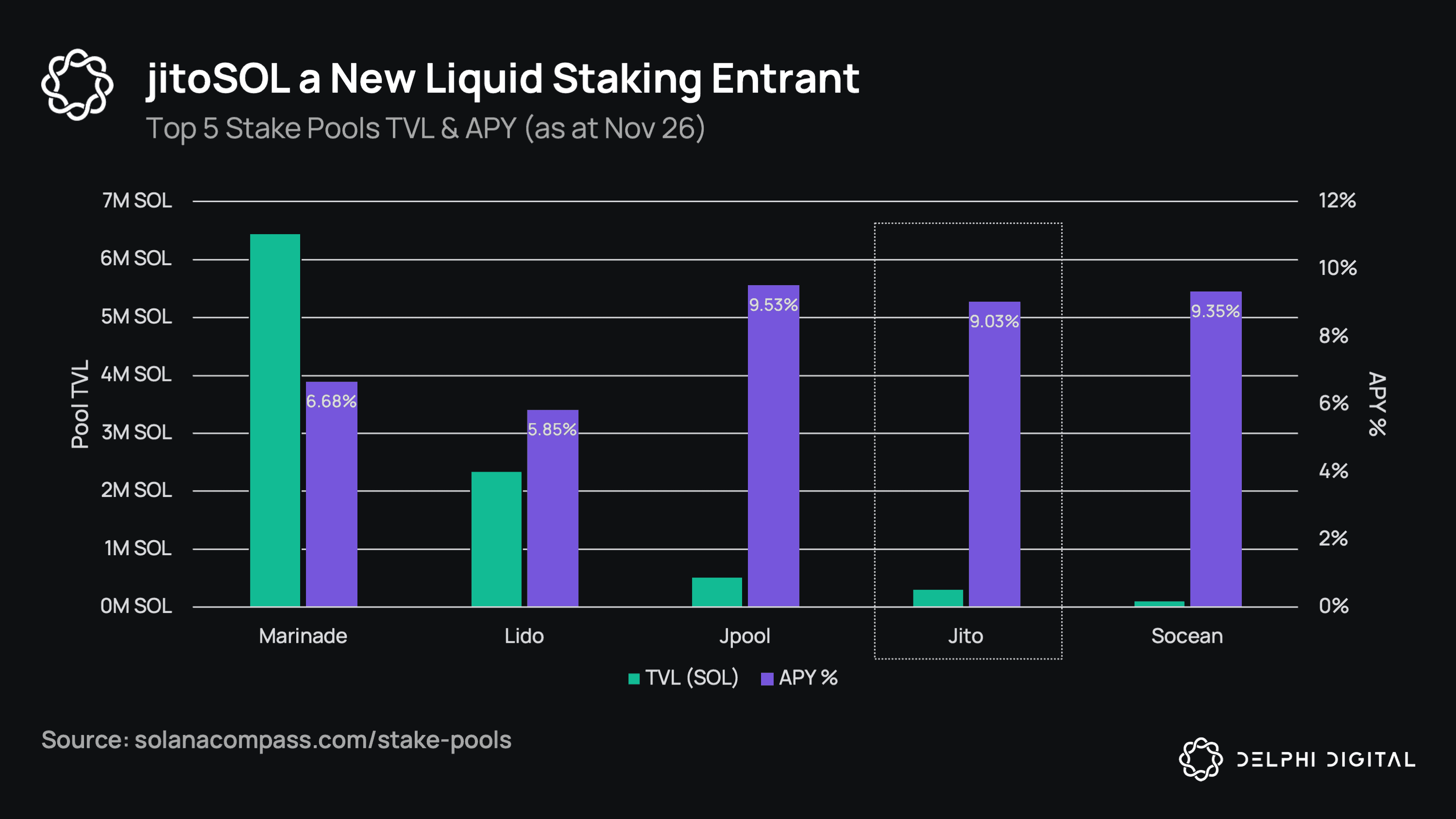

- Jito: Jito open-sourced their validator at the end of October (to be discussed in-depth later in the MEV section). At a high-level, the Jito validator not only enables a more efficient MEV market, but also filters spam, with the Jito relayer acting as a separate transaction processing unit, by extension reducing the burden on validators and improving Solana’s network stability. Spam (i.e., transaction floods) has been responsible for two of the four times Solana went down, and slowing the chain/causing high transaction-failure rates on other occasions.

- Firedancer: A new, independent Solana validator client in development by Jump Crypto. Built by a completely separate team than the Solana validator, Firedancer will help client diversity on Solana and make things like client or execution-layer bugs less likely to halt the network (overlap of the same bugs in both clients is low, so if one fails the other can keep running). Firedancer’s main difference is in its modular architecture, running many individual C processes called tiles (compared to the Solana Rust validator that runs as a single process). For a more complete breakdown, you can watch the presentation and demo from Breakpoint and read the latest blog post. Firedancer is probably the most important near-term development for Solana.

- OpenBook and Ellipsis: Spearheaded by the Mango Markets team and others in the Solana DeFi community, OpenBook is a community fork of the Serum DEX with the goal of replacing Serum as the backbone of Solana DeFi. Contributors come from a diverse group of protocols across the ecosystem, and there have even been discussions around whether SOL should be the token for OpenBook instead of creating a new one, making it a true public good. There are a lot of interesting proposals for how to incentivize development of OpenBook. For more details, refer to the first community call notes. Currently, volume is a fraction of what Serum was doing. Part of this is due to so many protocols built on Serum going offline and needing to integrate OpenBook. The other part is due to removing Alameda’s >50% of maker activity — something that will not come back overnight (this is one of the downsides to CLOBs that rely on large MMs vs. passive AMMs). OpenBook isn’t the only new CLOB on Solana though, with another promising competitor Ellipsis also in production and planning to go live in Q1.

- Mainstream UX: Stripe fiat-to-crypto integration was recently announced, with 11 of the 16 partners being protocols building on Solana. These include Magic Eden (NFTs), Glow Wallet, Orca (DEX), and more, offering direct fiat on-ramps to these protocols. Fiat-to-crypto on/off-ramps are arguably the most important pieces of infrastructure. In the long-run, these should be the only centralized points crypto needs to rely on. Solana also partnered with Discord, becoming the first blockchain to do so. The Saga mobile phone is also upcoming, which will be discussed in the “Futuristic Ideas” section at the end of this report.

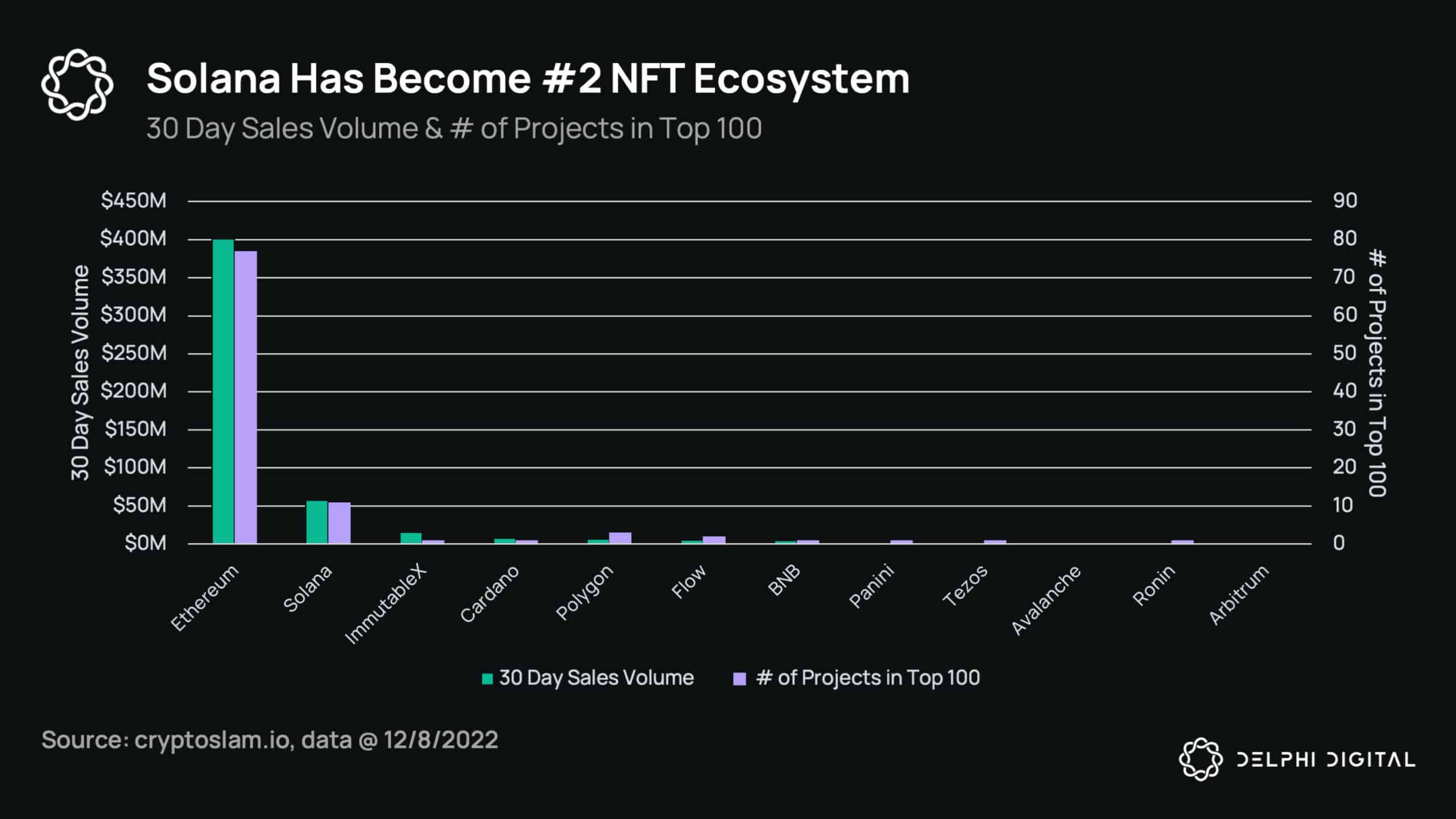

- NFTs: While there was an initial sell-off during the FTX implosion, Solana NFT activity has bounced back quite well. Solana has consistently had the second-largest NFT ecosystem for some time now, with 30-day volume of $60M vs. Ethereum’s $400M, more than 4x the next ecosystem, ImmutableX (which is made up of one collection). NFTs were not in the original pitch for Solana, so it’s quite notable that activity has passed NFT-specific chains like Flow. There’s a deeper meaning here for what NFT adoption implies about Solana. Did users come to Solana because they liked NFTs? Or did they come to Solana because they liked the UX of the chain, and then moved to NFTs because there was more upside and better risk/reward than with DeFi tokens? While the DeFi ecosystem rebuilds, NFTs will need to continue to onboard and retain users, although Solana can’t rely solely on NFTs forever.

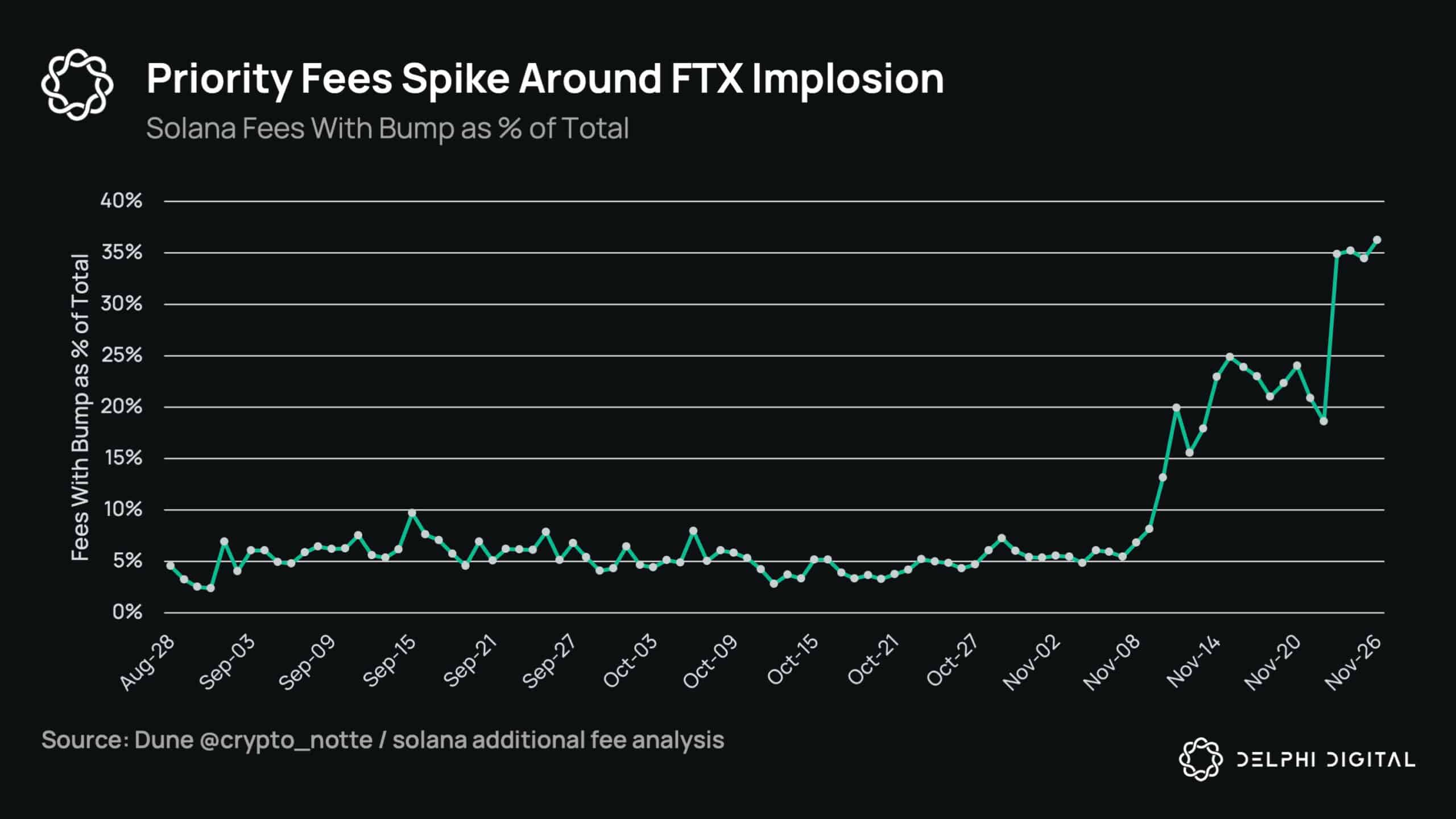

- Base-Layer Upgrades: QUIC, stake-weighted QoS, and isolated fee markets all improve Solana’s stability. QUIC and stake-weighted QoS are already live, while isolated fee markets are in production. The new fee markets will, theoretically, isolate network fee spikes to the most in-demand areas on Solana. For example, fees would spike for minting an in-demand NFT but would not rise at all for simple token transfers. This is in contrast to most other blockchain designs that have global fee markets (an NFT mint causes fees to rise for everyone). Solana also introduced a new “fee with bump” transaction which saw an uptick in adoption during November (see chart in the MEV section).

It’s no secret that Alameda/FTX were a big part of Solana’s rise, and we can probably say with confidence that a lot of the SOL price action in 2021 was due to them, and not real/organic. But losing Alameda, while it will hurt on-chain liquidity for the time being, is not a deathblow. Solana is unique in that it was designed from an engineering perspective rather than academic. While we have seen some of these design decisions hurt them over their first couple years, they have also unlocked unique use cases that not all other chains can achieve. Network stability has been getting better, TPS (excluding votes) are still significantly higher than any other chain, and the aforementioned improvements should continue to improve stability. Still, you should probably expect Solana to go down again at some point.

Solana is a truly differentiated product in an industry with so many copycats, and if you’re going to pursue the monolithic vision, it would probably look something like Solana. It’s also important to point out that so far, all blockchains have failed to scale. Ecosystems going through what seem like existential crises are nothing new; both Bitcoin and Ethereum went through their own challenges (Mt. Gox for Bitcoin and the DAO hack for Ethereum). It’s now Solana’s turn with the FTX collapse, and while surviving is by no means guaranteed, if they do, they’ll come out of the other side better for it. Encouragingly, DeFi protocols like Mango, Drift, and Zeta, among others, are all working towards new versions, with plans to go live soon.

Solana is dead. Long live Solana.

The Appchain World: Cosmos Gaining Momentum

A major component of appchains involves restricting access to state. Contrary to general-purpose chains, which allow anyone to permissionlessly launch new applications, appchains decide which applications they will run through social coordination. Similarly, cross-chain communication requires social coordination. Chains shake hands to establish IBC connections.

There is an inherent trade-off here. Appchains lose the agility of permissionless innovation, but in turn gain sovereignty over their applications. Furthermore, they get to optimize their chain for the particular use case(s) they want to address and thereby offer a more reliable UX.

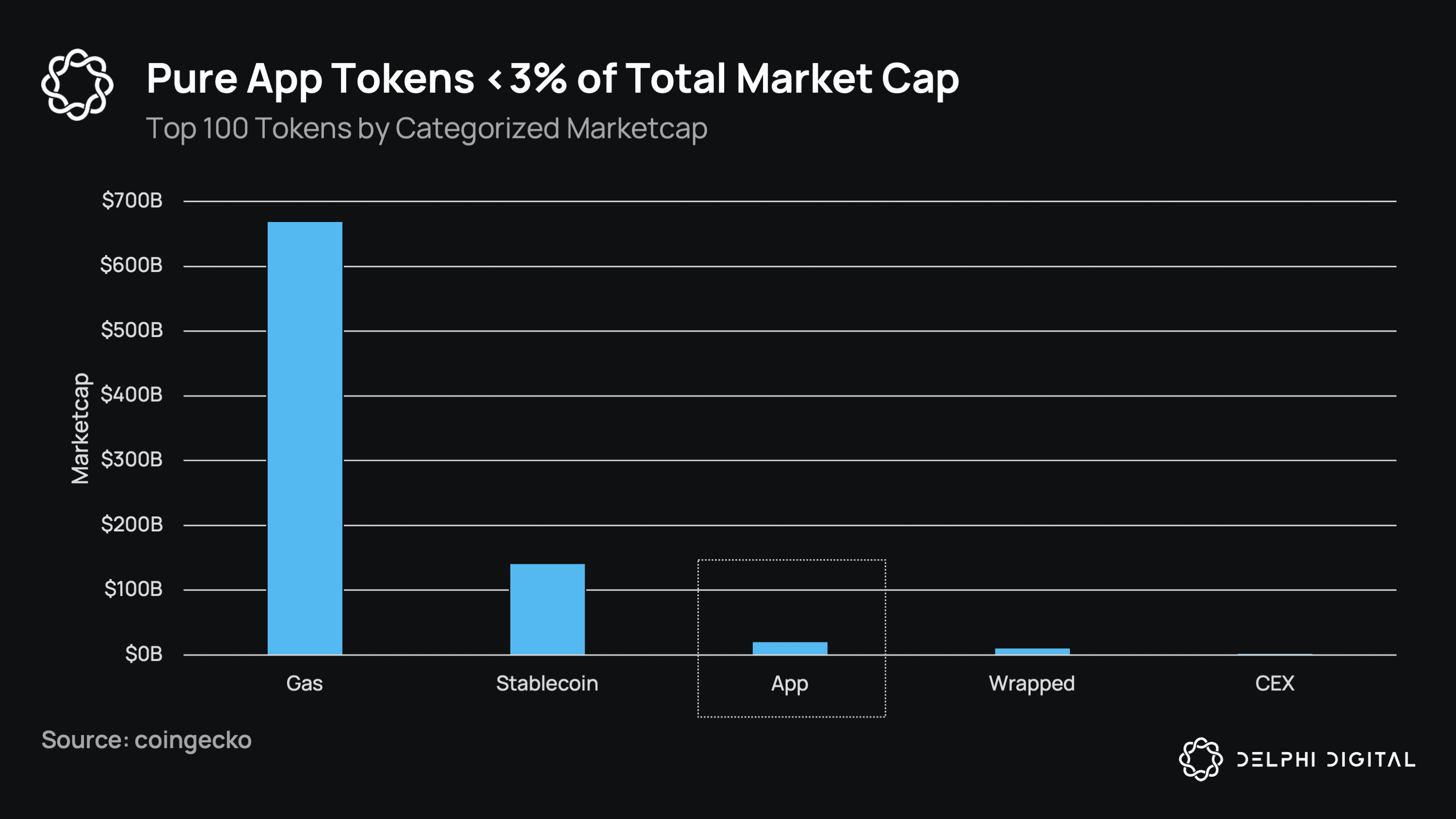

Another major aspect of the appchain thesis involves incentives. On general-purpose chains, revenue often leaks to the underlying gas token. Even the most popular dApps fall short in capturing most of the revenue they generate. Dan Elitzer’s Inevitability of Unichain is a great study which presents this case for Uniswap.

To further illustrate this point, we look no further than CoinGecko. It’s remarkable to notice how rare it is for pure app tokens to be among the top 100. Appchains fix this incentive misalignment by unifying app and gas tokens.

When we think of appchains today, we think of Cosmos, as the Cosmos SDK is the most production-ready toolkit to permissionlessly build a new chain from scratch. In the long-run, we expect appchains as rollups (or rollapps) to gain adoption as the tech becomes more mature. Some notable live and upcoming appchains today are:

When we think of appchains today, we think of Cosmos, as the Cosmos SDK is the most production-ready toolkit to permissionlessly build a new chain from scratch. In the long-run, we expect appchains as rollups (or rollapps) to gain adoption as the tech becomes more mature. Some notable live and upcoming appchains today are:

dYdX: A pure DEX appchain, it’s currently live as a StarkEx Ethereum L2 and will be shifting to Cosmos as a standalone chain in the new year. There is a massive opportunity in 2023 for the Cosmos ecosystem through dYdX, and FTX’s implosion (while obviously terrible) could not come at a better time. Trading is being “pushed” on-chain as centralized entities all throughout crypto blow up, and as the top DeFi derivative DEX today, dYdX has the most to gain (and lose). The launch of dYdX will be around the same time as the Cosmos Hub’s “asset issuance” consumer chain. This chain is where Circle will issue USDC, with dYdX being the largest first customer (dYdX currently has $430M USDC on their StarkEx L2). This will heavily bootstrap the amount of native USDC on the Interchain — something that has always been lacking throughout Cosmos and IBC. In essence:

- dYdX growth is good for native USDC growth on Cosmos.

- Native USDC growth on Cosmos is good for the growth of activity through the Hub’s economic zone as an Interchain Security provider of the asset issuance chain.

- Growth of the Hub as an ICS provider is good for the adoption of other consumer chains, and native USDC makes bootstrapping them quicker.

- Native USDC growth and the growth of the Hub’s economic zone is good for overall liquidity to grow to other appchains in the ecosystem.

Osmosis: The “liquidity hub” of Cosmos, Osmosis is the most active chain in IBC, with the highest TVL (~$200M) and IBC volume (>$1B per month). It also acts as the backbone for liquidity for Cosmos chains tokens. Osmosis’ first main innovation was Superfluid staking, a module which allows the underlying OSMO in liquidity pools to simultaneously be LP’d and staked to secure Osmosis. The latest Fluorine upgrade adds some more features like a stableswap AMM, IBC rate limiting, and multi-hop routing. IBC rate limiting is a response to the numerous bridge hacks we saw in 2021-2022, putting a cap on the percentage supply of a token that can move in/out of Osmosis during a defined window. Multi-hop routing adjusts LP fees to account for swaps going through multiple pools. For example, a swap of USDC for ATOM would go through the USDC/OSMO pool and then the OSMO/ATOM pool. Instead of charging the 0.2% swap fee that both of these pools charge, the fee will be cut in half to 0.1% to charge 0.2% total. Osmosis has more in the pipeline for 2023, including a concentrated AMM, MEV mitigation through threshold decryption and a partnership with Skip to “internalize” MEV (i.e., have the protocol complete arbs against itself), the launch of Mars Protocol for borrowing against LP tokens, Interfluid staking (similar to Superfluid, but staking the underlying LP tokens of non-OSMO tokens), mesh security, and more. A lot of Osmosis’ growth can be attributed to their high supply issuance/inflation, but the upcoming features and integrations in 2023 offer paths for more organic traction while becoming the liquidity backbone throughout IBC.

Sei and Injective: As “DeFi-optimized” chains, Sei and Injective sit in the middle between pure appchains and something more general purpose. They’ve built orderbook logic into the base layer and have permissioned apps built on top. A key difference between dYdX and these two is that dYdX is a pure appchain focusing on derivatives, while Sei and Injective are just the infrastructure layer for things like perps, options, stablecoins, and more to be built on. Sei is also aiming to be the base layer for both the SolanaVM and MoveVM rollups. For a deep dive on Sei, you can read our report from September.

Interchain Security

Finally, one of the biggest catalysts for appchains will be infrastructure that makes it easy to launch new chains. Enter Interchain Security, which allows appchains to spin up without bootstrapping an entire validator set. With ICS, new chains are able to lease security from the Cosmos Hub’s (ATOM) validators and stakers in return for some percentage of the tokens and fees generated on their chains (percentages are variable). For more on ICS, you can reference our Cosmos report here. ICS is expected to go live in January, with the first chains launched in February. Notable consumer chains include:

Neutron: A PoS smart contract chain secured by the Hub, slated for launch shortly after ICS goes live in Q1 2023. Neutron gives the Hub (ATOM) a smart contract platform to try all of the new/experimental things they want to use and develop. This includes things like CosmWasm contracts, ICAs for cross-chain operations, and ICQs to read data from other chains, along with using these in tandem for innovative products like an Interchain DEX, all while keeping the Hub isolated. In a nutshell, it’s a fully permissionless general-purpose smart contract chain secured by the Hub. Really, anything that can be developed on a CosmWasm smart contract chain can be deployed on Neutron, a breeding ground for smart contract dApp innovation within the Hub’s economic zone. One of the first notable projects to be launching will be Lido, issuing their ATOM liquid staking derivative on Neutron. Neutron is currently in testnet on the Hub’s “Game of Chains” ICS testing ground, which has recently moved to phase three.

Asset Issuance Chain: Sometimes described as a USDC/Circle consumer chain, this will be a chain secured by the Hub for generic asset issuance. USDC will be the first asset to launch, but any centralized asset wishing to issue on the Cosmos ecosystem could choose this chain as the canonical one. As this chain will be onboarded by CEXs, it’s likely to be the central point for these assets to issue their tokens.

Duality: A DEX appchain that aims to become a sort of hybrid between AMMs and CLOBs. Duality’s core feature is the ability to create AMM pools that allow swaps at a constant price. This differs from a typical concentrated AMM where price ticks determine a range. Duality allows liquidity to be placed at specific prices, resembling limit orders on a CLOB. Any arbitrary curve can be built on top of a Duality pool, and traders can utilize market or limit orders to access the underlying shared liquidity between all pools. Like Osmosis, their main competitor, Duality aims to internalize and redistribute arbitrage profits from MEV back to LPs. Duality is planning to go live in Q1 2023.

Stride: Liquid staking is a big focus of the ATOM 2.0 whitepaper, and Stride is the first to market. While Stride is a standalone chain today, it will become a consumer chain once ICS is live (to get economic security from the Hub). When you think of a liquid staking token, it’s imperative that the security of the underlying asset is not jeopardized by a chain with a low-market cap token and less-tested validator set securing it. Stride has issued the liquid staking tokens stATOM, stOSMO, and stSTARS, all of which have incentivized pools on Osmosis. The main competitors to Stride will be Lido (when they launch on Neutron) and Quicksilver, another Cosmos-native liquid staking solution coming to market. Quicksilver just announced their launch date of Dec. 16th.

Polymer: zk-IBC, discussed in the section above.

FairBlock: “Bad” MEV prevention through an identity-based encryption (IDE) scheme, discussed in the MEV section later.

While ICS is a great tool which allows new chains to bootstrap, it also allows a wider range of products to be built for the Cosmos Hub in their own “economic zone.” These early consumer chains will give ATOM a general-purpose smart contract chain, an asset issuance platform for stablecoins and other assets, a fully customizable high-performance DEX, liquid staking, and more. ICS scales the Hub in a way that couldn’t be done before.

Appchain Wrap-Up

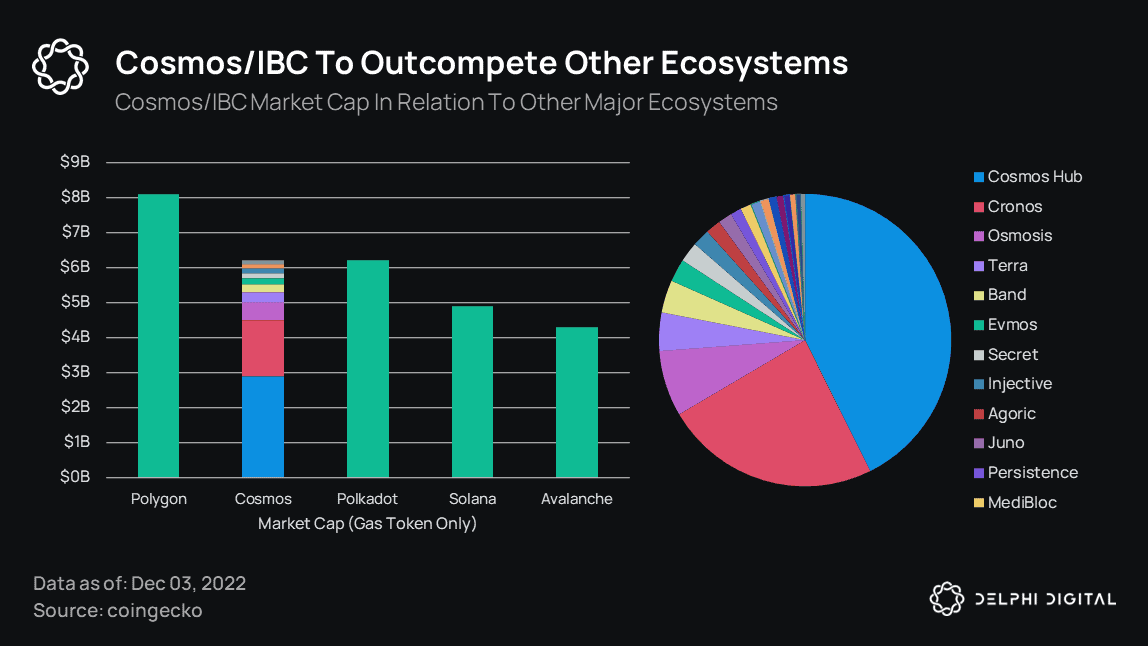

Before we move on to modular blockchains, we would like to share our conclusion for appchains and the Cosmos ecosystem. Overall, we notice developer activity on Cosmos is more lively than ever. Cosmos infrastructure is already ready to onboard new applications by horizontally adding new chains to their IBC ecosystem. The asset issuance (USDC) chain and IBC tapping into other ecosystems can bring significant inflows to Cosmos. Next year, considering other ecosystems continue to suffer from bridge exploits, Cosmos will be well positioned to increase its market share.

Modular Blockchains

The rollup-centric vision set forth by Ethereum has been the biggest catalyst of smart contract rollup development. Last year, Celestia broadened the rollup definition by introducing the notion of sovereign execution and/or settlement rollups as well as Celestiums.

Today, we refer to these different architectures as modular blockchains; blockchains that outsource at least one of their core functions (execution, settlement, consensus, data availability) to another blockchain.

While we expect the modular blockchain thesis to materialize over a very long time, there have been significant developments this year and there are many in the roadmap for next year.

Ethereum Ecosystem

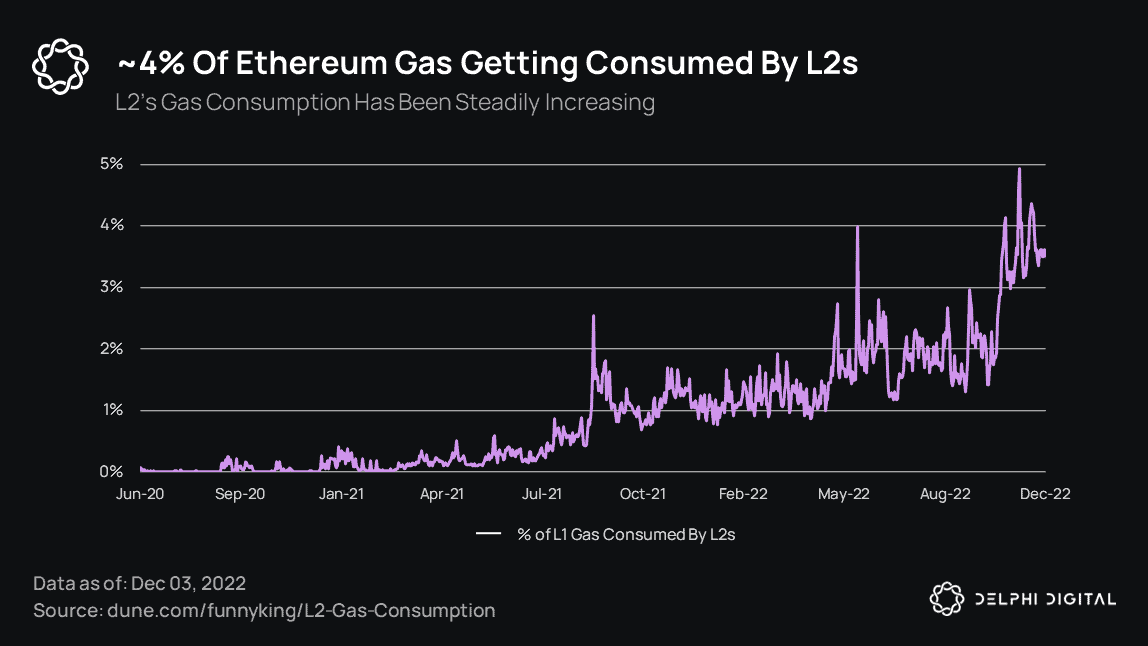

L2 adoption on Ethereum over the last year has been impressive. The most reliable way to see this is to look at how much of the base-layer gas fees have been consumed by L2s. We notice that their share of L1 gas consumption has increased from less than 1% in the beginning of the year to 4% today.

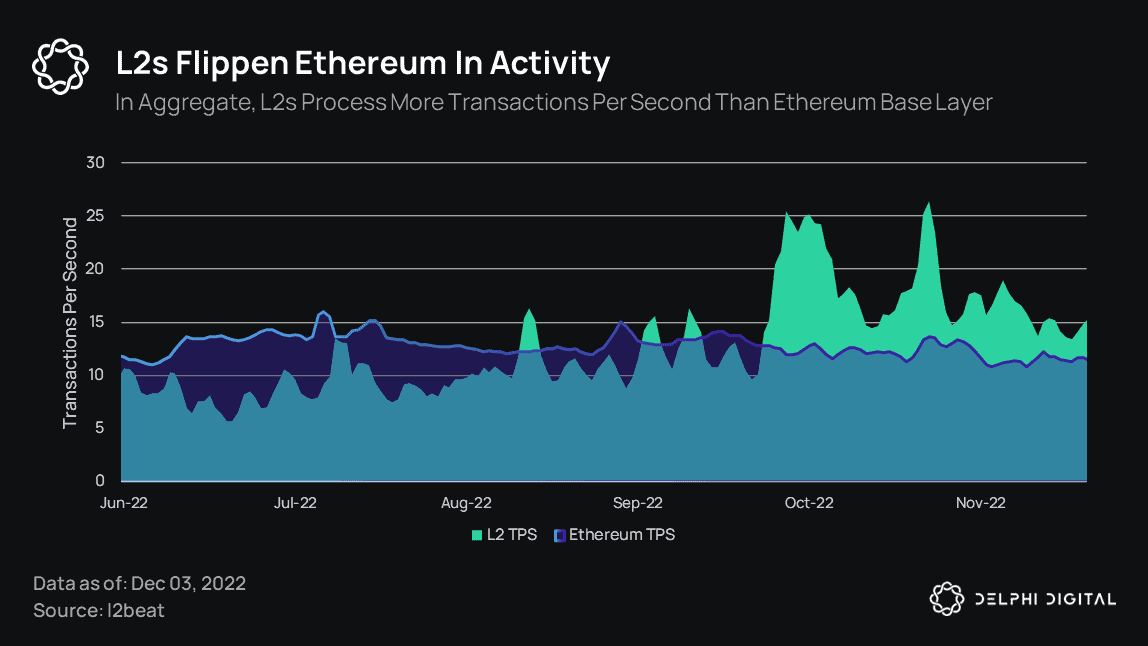

As L2 gas consumption increased, so did their TPS. This year, L2s have flipped the Ethereum base layer in terms of TPS.

As L2 gas consumption increased, so did their TPS. This year, L2s have flipped the Ethereum base layer in terms of TPS.

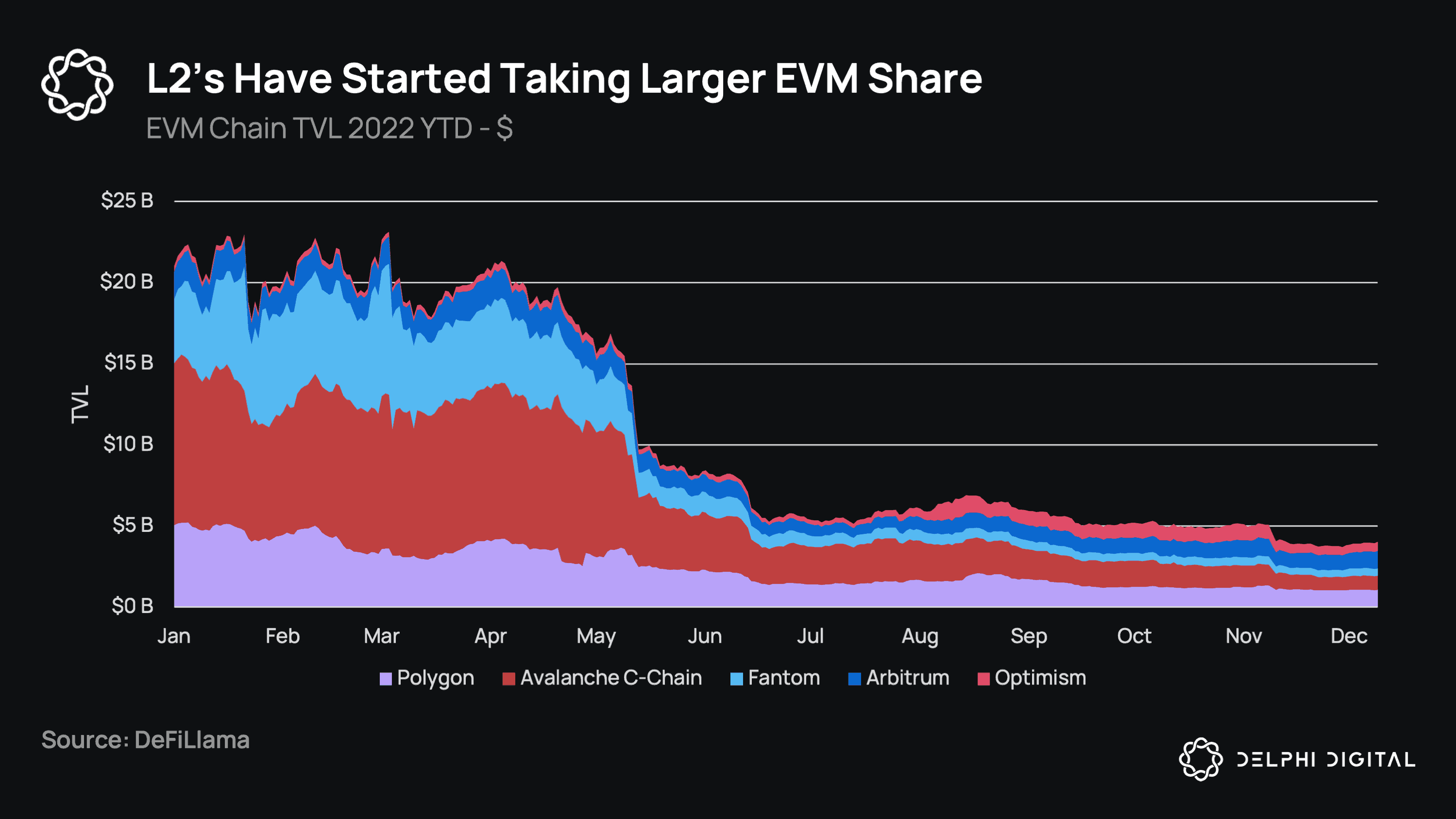

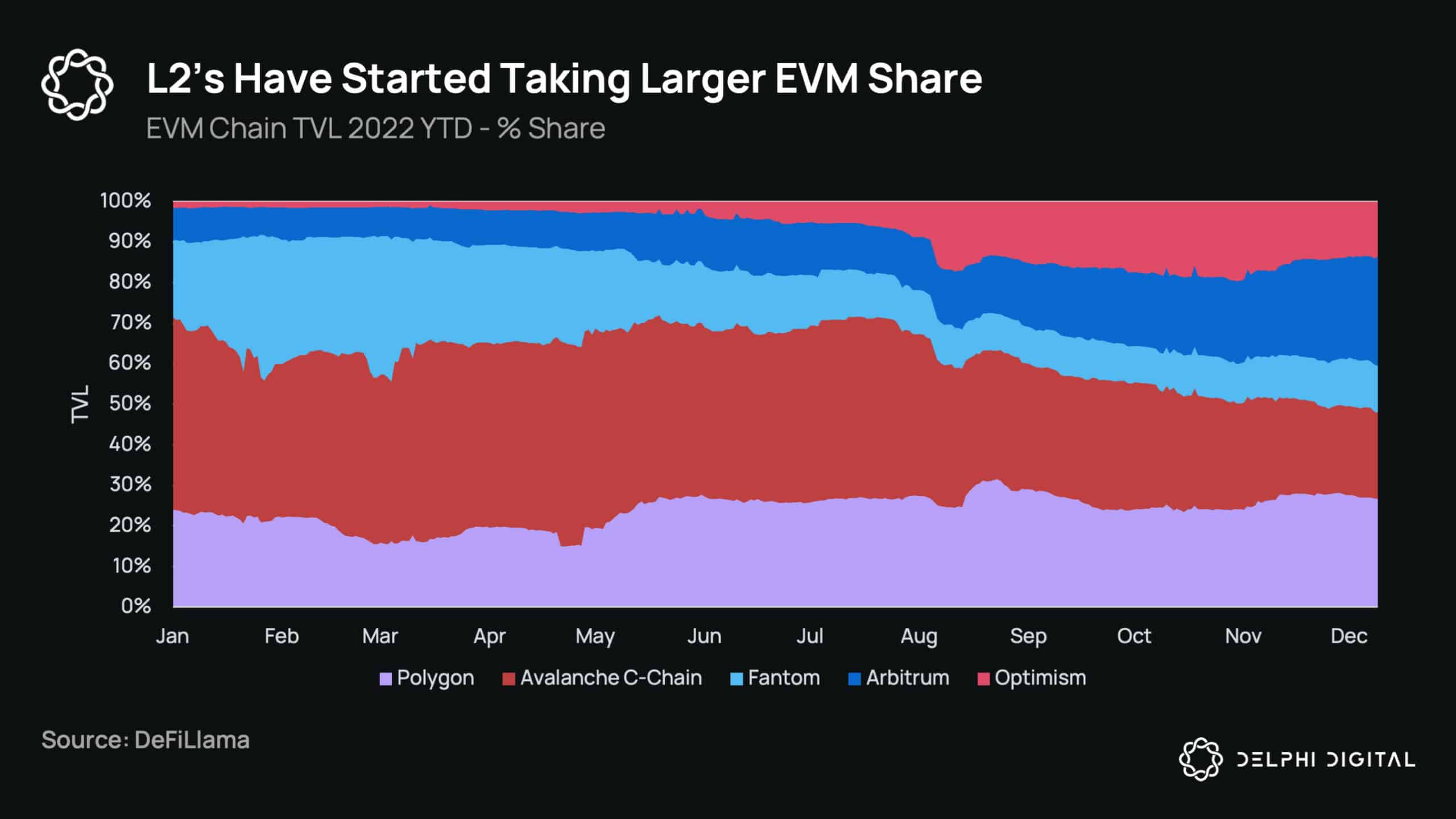

Contrary to major EVM L1s like Avalanche and Polygon, which have lost significant liquidity since the beginning of the year, TVL on Arbitrum and Optimism has been consistently increasing. This is a trend we saw starting in the summer and has only increased since.

Contrary to major EVM L1s like Avalanche and Polygon, which have lost significant liquidity since the beginning of the year, TVL on Arbitrum and Optimism has been consistently increasing. This is a trend we saw starting in the summer and has only increased since.

EIP-4844, AKA Proto-Danksharding

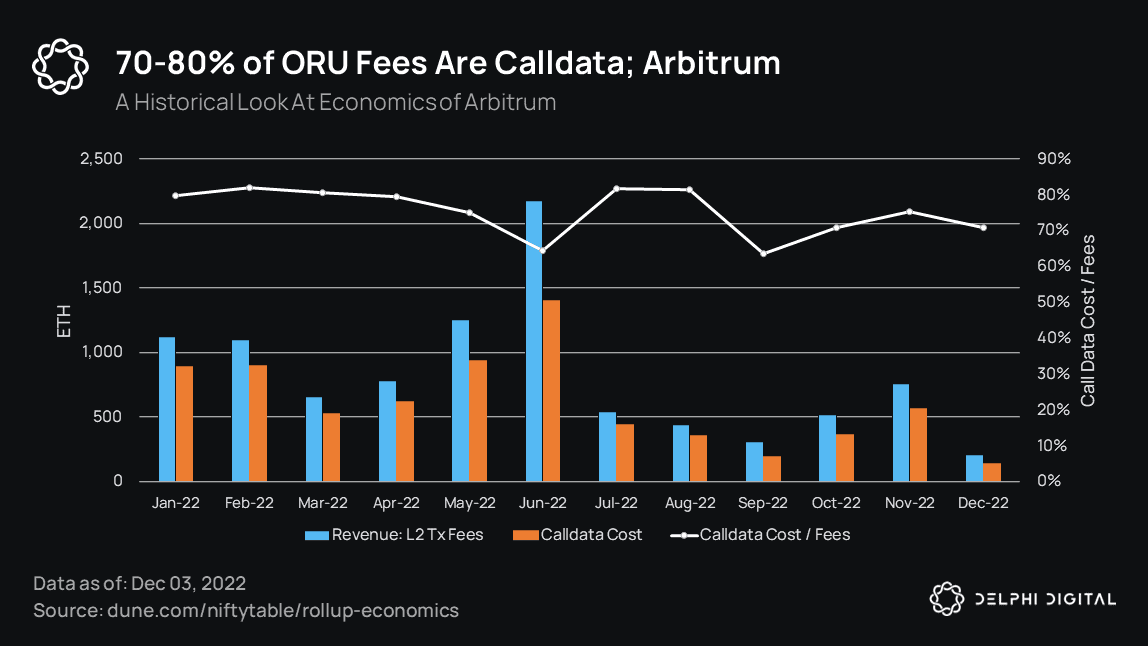

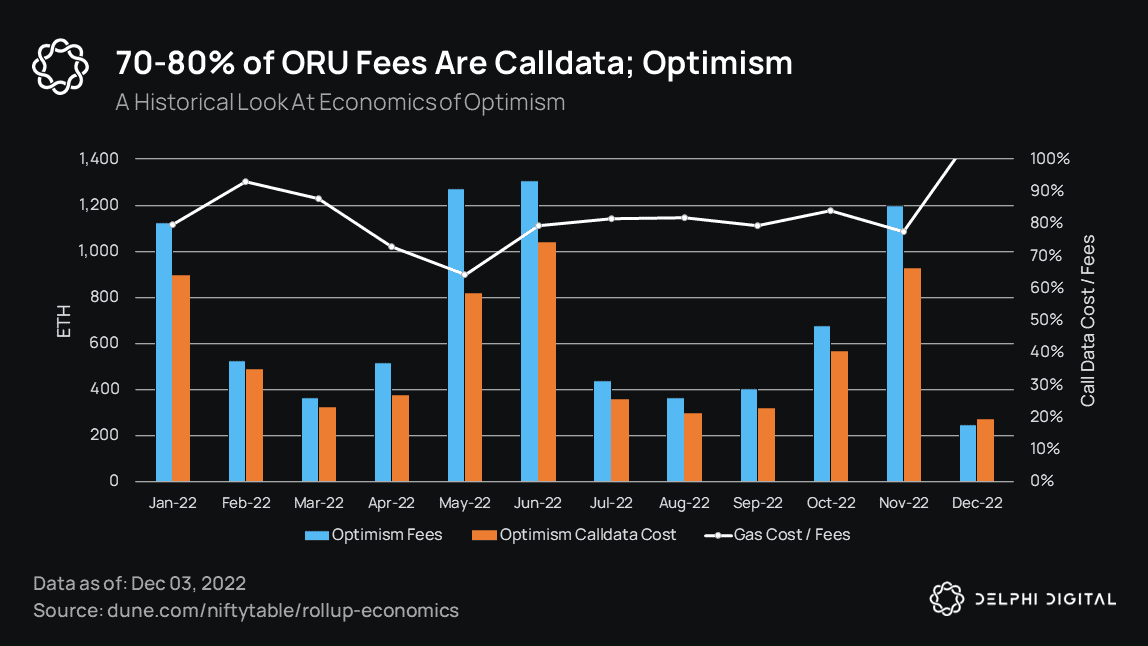

EIP-4844 will be a major milestone for Ethereum L2s (particularly rollups) next year. EIP-4844 is going to be a pivotal moment for Ethereum because it will significantly reduce transaction fees for rollups.

Rollups have two separate costs — execution on L2 and data on L1. Currently, the highest-cost item for Ethereum rollups is posting data to Ethereum. EIP-4844 will reduce this fee by increasing the data capacity of Ethereum by an order of magnitude.

Today, data posted by rollups is stored by the L1 forever. However, forcing the L1 to store old, stale data doesn’t really bring any meaningful security to L2s (for example, ORUs can’t be rolled back to a state that’s older than the fraud proof window, ~2 weeks). The L1 just needs to store L2 data for a reasonable time so that anyone interested in joining the rollup network can do so as it progresses.

Today, data posted by rollups is stored by the L1 forever. However, forcing the L1 to store old, stale data doesn’t really bring any meaningful security to L2s (for example, ORUs can’t be rolled back to a state that’s older than the fraud proof window, ~2 weeks). The L1 just needs to store L2 data for a reasonable time so that anyone interested in joining the rollup network can do so as it progresses.

EIP-4844 relaxes the data requirement on Ethereum L1. It introduces a new type of blob-carrying transaction where the blob of data doesn’t need to be stored forever, but only for ~2 weeks. This increases the data capacity that can be posted on L1 and, in turn, reduces data costs for rollups. Post-EIP-4844, Ethereum will have two separate fee markets, one for execution and one for data availability.

EIP-4844 will reduce rollup fees by an order of magnitude. This will encourage more dApps to migrate to rollups and accelerate developer mindshare across modular blockchains.

It’s important to note that EIP-4844 is a step before Danksharding. It will increase the data capacity of the base layer by relaxing a requirement which is deemed unnecessary. However, each node will still store the full data. Therefore, EIP-4844 doesn’t introduce data availability sampling; the core tech that brings true scalability. Data availability sampling, where nodes store shards of data, will be introduced with Danksharding.

EIP-4844 likely won’t be ready in time for the Shanghai hard fork, which is optimistically expected around March next year. EIP-4844 will be the next major update after Shanghai.

Those interested in Ethereum’s roadmap for next year, can check ‘Hitchhiker’s Guide to Ethereum‘ where we comprehensively cover it in layman terms.

EigenLayer: A unique project that could play an important role for Ethereum is EigenLayer. EigenLayer can be considered Ethereum’s version of Interchain Security. It will enable Ethereum validators to re-stake their ETH in order to offer additional services which could be helpful for Ethereum L2s as well as the base layer. By re-staking their ETH, validators will make it subject to additional slashing conditions against malicious behavior (which will be enforced by Ethereum base layer). In turn, validators will receive rewards from the services they provide.

In Interchain Security, consumer chains are selected by the provider chain’s consensus. In EigenLayer, Ethereum validators will be free to opt-in to provide any service they want, which is great for permissionless innovation. Use cases planned range from a hyperscale data availability layer for L2s to BFT protocols.

One application that actively works with EigenLayer is Mantle. Mantle is a modular execution layer which intends to use EigenDA (EigenLayer’s data availability service) for data availability. This hybrid approach may enable a sweet spot where Mantle doesn’t pay expensive data costs like rollups do yet can still have superior security compared to sidechains; a solution that could be appealing for gaming and many other applications. Mantle also plans to implement EIPs that improve the UX to solve many of the issues discussed earlier in the access control section. As noted in their announcement, Mantle is a product of BitDAO. And, as gas for its execution layer, it intends to use BitDAO’s governance token BIT.

Given that EigenLayer services are run by Ethereum validators, a competitive advantage of EigenLayer is to offer services related to the Ethereum base layer. One exciting use case here involves credible commits, which enable validators to commit to MEV strategies. Generally speaking, EigenLayer services can supercharge the rate of innovation at the protocol level.

Celestia Ecosystem

We’ve initally covered Celestia in depth in the beginning of the year in our Pay Attention To Celestia report. Since then the Celestia network has significantly evolved and is planning to go to mainnet around Q2 2023. With this, Celestia is expected to become the first truly modular blockchain network in production. The mainnet launch of the base data availability layer will be followed by a number of modular settlement and execution layers, kickstarting user-facing applications. Based on their current roadmap, some of those projects include Fuel, Astria, Eclipse, and Dymension.

Fuel is an ambitious and comprehensive project destined to become a major player in the modular stack. The Fuel team has been developing FuelVM from scratch to create the fastest modular execution layer. We are highly impressed and excited by the design choices Fuel made on their VM. Those interested in a more comprehensive overview of Fuel can refer to our report Is Fuel the Best Modular Execution Layer? Fuel is likely to have multiple instances including PoS sidechain to Ethereum, a smart contract rollup on Ethereum as well as a sovereign rollup on Celestia. Fuel may also operate as a settlement layer in the future.

Note: This paragraph was edited post-publication on 01/06/23

Astria (previously known as Cevmos) is a purpose-built settlement layer which runs a restricted EVM. Astria will only execute fraud/validity proofs for execution rollups that settle on it, and will not run other applications. Astria is a good option for rollups looking for a cheap EVM settlement layer.

Eclipse recently completed its seed round and will be running SolanaVM both for the settlement layer and the execution layers that will run on top. For this, Eclipse will be working on an ambitious goal to make SolanaVM fraud-provable. Given their value-add to the Solana ecosystem, Eclipse is also supported by the Solana foundation, receiving a grant from them to build IBC messages for SolanaVM. Eclipse plans to launch three testnet chains in Q1 and plans to launch mainnet roughly around Q2.

Dymension is also a settlement layer. But, unlike Eclipse and Astria, it’s not a rollup — it’s a Cosmos appchain. Dymension wants to make it very easy to bootstrap new app-specific rollups known as rollapps. Rollapps will settle on Dymension, which will allow them to access IBC.

Rollups Are in Their Infancy

While all of these developments are exciting, it’s important to realize that rollups are still in their infancy, and are likely to operate with training wheels for the foreseeable future. Almost none of the optimistic rollups have permissionless fraud proofs, and all rollups have safety-critical upgradability paths in their contracts, making their bridges non-trust minimized. The tech stack of modular chains is challenging, and it will take years of research and engineering efforts for modular chains to unleash their full potential. See ‘The Complete Guide to Rollups‘ for a deeper dive.

Highlights From Other Modular Ecosystems

Polygon is a major ecosystem that strongly supports the modular vision. The core team has been heavily investing in numerous modular execution layers including several different zk-rollups: Hermez, Miden, Zero, and Avail (the data availability layer). It’s hard to comment on timelines for these projects. However, among all of them, the Hermez EVM-compatible zk-rollup seems to be the most mature. The project is currently in public testnet.

StarkNet plans to have its re-genesis by early next year. This will make fundamental improvements in the StarkNet infrastructure including the full transition to Cairo 1.0. Recently, StarkNet also deployed its token on Ethereum. As per the announcement, the tokens aren’t for sale. However, some tokens will start circulating by the end of next year and the foundation will determine and announce the distribution strategy for its allocation at a future date.

Similarly, zkSync plans to have its full launch alpha early next year, and plans to decentralize parts of the network including proof generation, block production, etc., within the next year. For a complete overview on zk-rollups see our report from June.

We also expect new ecosystems to adopt modular architectures. One such ecosystem worth following is Sei — a DeFi-focused high-performance Cosmos appchain.

Nitro SVM and Paddle are two highly performance-optimized rollups that plan to launch on Sei; the former runs SolanaVM and the latter runs MoveVM. Indeed, Paddle is going to be the first rollup to run MoveVM, a relatively new smart contract platform. MoveVM has already been adopted by fast monoliths like Sui and Aptos and is considered to be among the fastest and most secure VMs.

Privacy

The openness of public blockchains is a double-edged sword. From a solvency and transparency standpoint, the openness is a feature, and one of blockchain’s greatest strengths. Being able to audit protocols in real-time and check their solvency in a few seconds solves the black box opaqueness we see with centralized institutions — a lesson learned quite painfully in 2022.

After the FTX collapse, we saw DeFi protocols like dYdX post proof of reserves on Twitter, hammering home the point of why DeFi is worth building. You can’t run into a Celsius or FTX situation with fully collateralized on-chain protocols. A one-click audit of dYdX’s entire reserves is something that will never be achievable in CeFi, regardless of how robust the PoR process is or the diligence and reputation of the audit firm.

However, a 100% transparent financial network is not without its trade-offs. When it comes to personal financial privacy, this transparency is not a feature, but a bug. Not only does having your history 100% on-chain leak profitable trading strategies to the public (leading to alpha decay), but it can be dangerous from a personal safety standpoint. With FTX’s collapse a general theme of this report, we look no further than mainstream media outlets like Bloomberg, The New York Times, and Financial Times filing to dox all creditor information publicly.

Publicly revealing creditor information in this case is extremely dangerous, as it has the potential to leak not only customer information and account balances at FTX, but on-chain addresses used as well, giving bad actors the ability to tie someone’s entire financial history together, especially when this data can be cross-referenced with other leaks. We shouldn’t have to further explain why someone’s entire financial history and residential address becoming public is a problem. It’s clear we need to come to a middle ground — one where the auditability and solvency of protocols is available 24/7 but personal data is private and safe from the public’s eyes. We expect privacy to come back into focus as a major theme, with the battle not only being a technical one, but a regulatory one as well. You can draw parallels to the war against encryption.

Penumbra: As a fully private DEX, Penumbra acts as a shielded pool within the Cosmos/IBC ecosystem. Their shielded swaps prevent certain MEV-like front-running and sandwich attacks and utilize a sealed-bid, batch execution that clears orders at a single price. Their v1 AMM utilizes a concentrated liquidity design, and market makers can deploy strategies privately without having them leak. Being connected through IBC, future use cases (like private governance voting on Cosmos chains with Interchain Accounts) will allow users to vote privately from their Penumbra accounts on any connected chain. While trade/transaction history is fully private publicly, users can decrypt their entire history on demand. Penumbra is expected to go live in 2023.

Aztec: A privacy-first zk-rollup on Ethereum, Aztec is different from other zk-rollups like StarkNet, Scroll, and zkSync in that it uses zero-knowledge tech for privacy rather than scaling. Their flagship product is Aztec Connect, which is unique to other rollups because instead of having its own smart contracts, dApps, and liquidity, it just acts like a VPN to use the Ethereum L1. Ethereum protocols can integrate with the Connect SDK to allow Aztec users to use their protocol privately from Aztec. Connect acts as a type of private pool; multiple users on Aztec submit encrypted transactions like swaps which then get batched together into one and executed on Ethereum. Not only does this batching provide privacy, but it can reduce gas fees by amortizing the cost among many users and transactions. Since all liquidity stays on Ethereum, there’s no fragmentation of liquidity, contract redeployment, or the need to re-audit any code. Their product zk.money started with just simple transfers, but has now expanded to a wider range of DeFi activities like staking, swaps, and borrow/lend. Currently in the works are expanding to private NFTs and the launch of their new zero-knowledge language Noir.

Aleo and Mina:

Blockchains increasingly move away from a model where everyone re-executes everything to one where computation happens off-chain and verification happens on-chain. We see this play out in the modular world with Ethereum L2s. But there are also L1s that are built with this principle from the ground up. Aleo and Mina are two such blockchains.

Both projects are ZKP smart contract platforms. Programs are run off-chain via a network of provers who submit zk-proofs on-chain that smart contracts can efficiently verify. Both are building infrastructure for general-purpose applications, but with slightly different primary focuses. Aleo’s primary focus is privacy whereas Mina’s is scalability.

Aleo:

Note: This paragraph was edited post-publication on 01/06/23

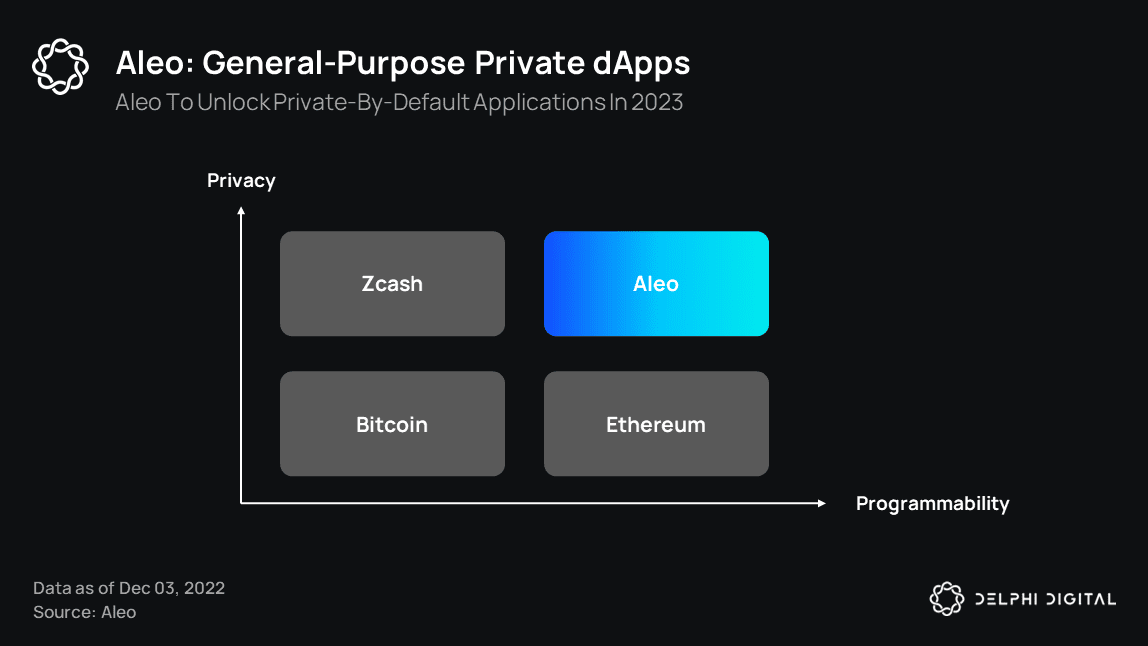

Aleo is a private-by-default smart contract platform. What this means is that developers don’t have to think about privacy considerations when developing dApps on Aleo, they get it for free by default. Nonetheless, they retain the ability to decide which aspects of their applications they want to display publicly.

Aleo is the largest project in the privacy space in terms of scope. It has raised a record-high $200M as a privacy project and is building an entirely new tech stack including its own language Leo — a SNARK-based virtual machine and OS.

A well-thought-out aspect of the project is its hybrid usage of PoW/PoS; PoS for instant finality and PoW to scale the performance of the proof generation. Aleo distributes a portion of block rewards to decentralize and open up proof generation to an open network of SNARK provers. On the other hand, instant finality allows easy interoperability with other chains — a crucial factor for the adoption of a standalone privacy chain.

Aleo just recently announced its incentivized testnet and will go to mainnet in 2023. The main challenge for Aleo will be bootstrapping a developer community around its new tech stack and programming language. We are excited for what Aleo is set to unlock and are looking forward to seeing how this will unfold for them.

MEV: What Is It Good For? (Absolutely Everything)

As one of (if not the) most important topics in crypto, we’d be remiss if we did not cover MEV in this report (“wait, it’s all MEV?” alwayshasbeen.gif). This section won’t be a complete deep dive on what MEV is, but rather how the MEV landscape looks today and how it may develop in the future. For a deep dive on the technicals, you can read the MEV Manifesto. For this report, we’ll start with Ethereum and how the market looks post-merge. Then, we’ll take a look at MEV-Boost adoption, relays, builders, censorship concerns, and round it out with some recent developments from Flashbots. After that, we’ll look at MEV on Solana and what Jito is doing there. Finally, we’ll explore the nascent MEV ecosystem in Cosmos while covering some projects that will help shape how it develops over the coming years.

Ethereum MEV Post-Merge

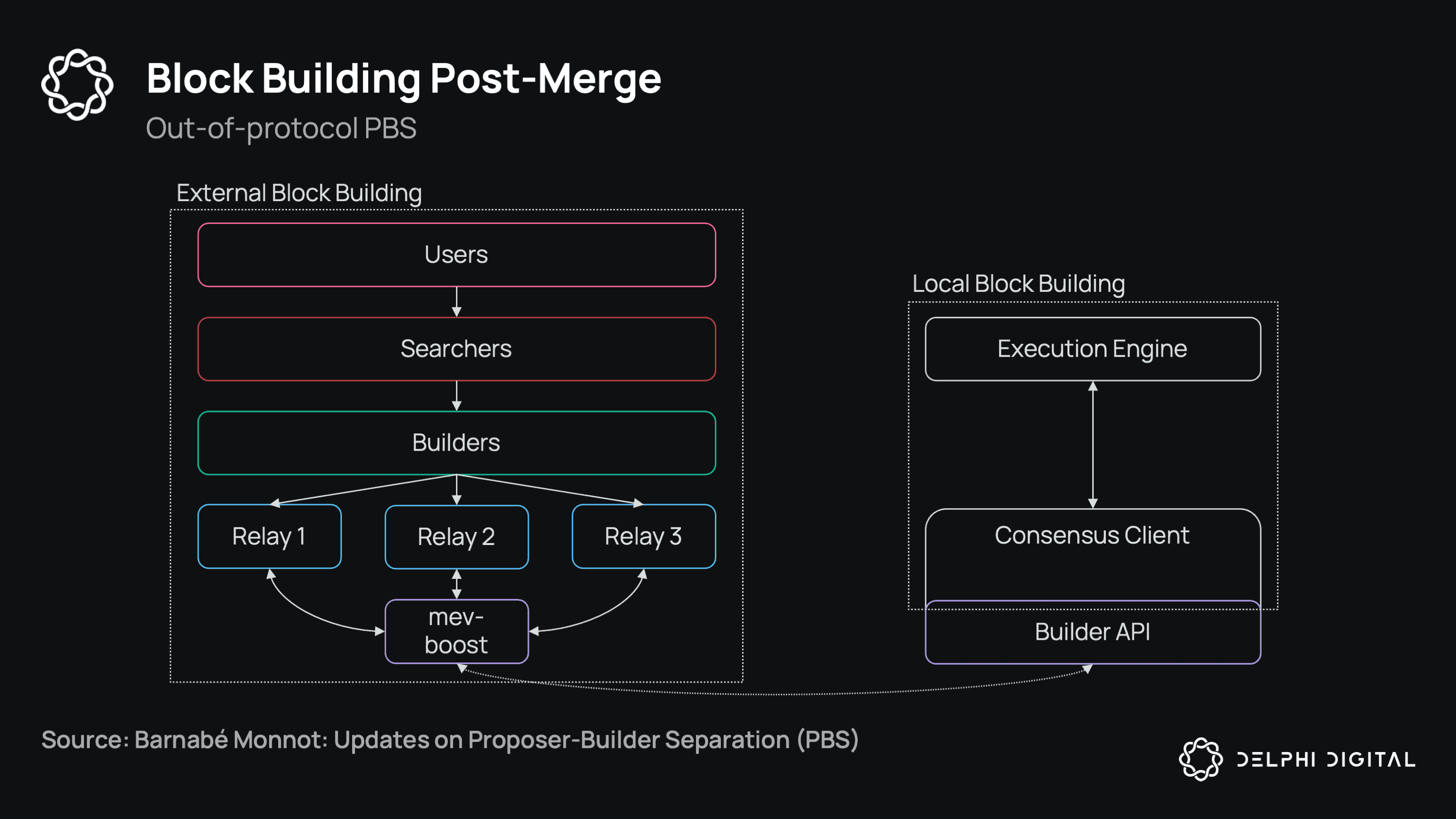

As a high level overview, Ethereum blocks can be built either locally or externally. Local block building is simple: it’s the default process where validators receive public mempool transactions, package them into a block, and then broadcast this block to other validators in the network. This is all done by the validator in isolation.

In external block building, validators outsource the block-building process by running MEV-Boost, a “sidecar” piece of software that allows validators to profit from MEV without any knowledge, sophisticated systems, or relationships with builders. MEV-Boost is simply an aggregator of relays that will choose the highest bid (i.e., most profitable) block from the relays the validator has connected to. The main stakeholders in this supply chain are searchers, builders, and relays.

- Searchers: Run MEV strategies and send bundles (sequences of transactions) to builders. They want to integrate with profitable builders that have high inclusion rates and need to trust builders to not steal/front-run them. There’s a trade-off here, because submitting to more builders increases inclusion odds but also increases the number of builders that searchers need to trust.

- Builders: Aggregate transactions from searchers and other sources to build blocks. Builders try to build the most profitable blocks and then pass them through relays to proposers. They need to trust relays to pass along their block if it’s the most profitable, and they want to connect to relays that have a high number of validators connected to them. If they build the most profitable block but the current proposer is not connected to the same relay, their block won’t be executed.

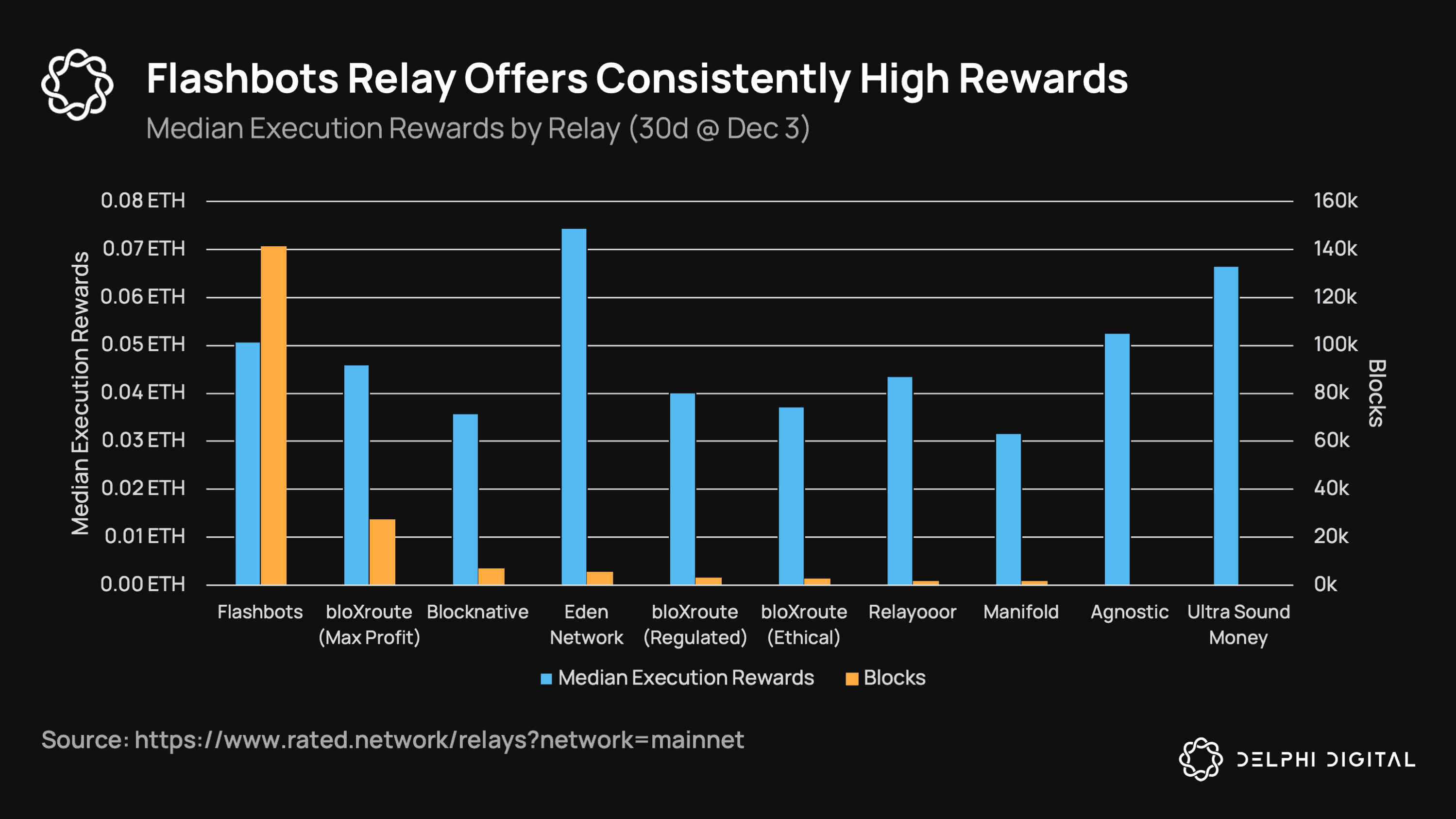

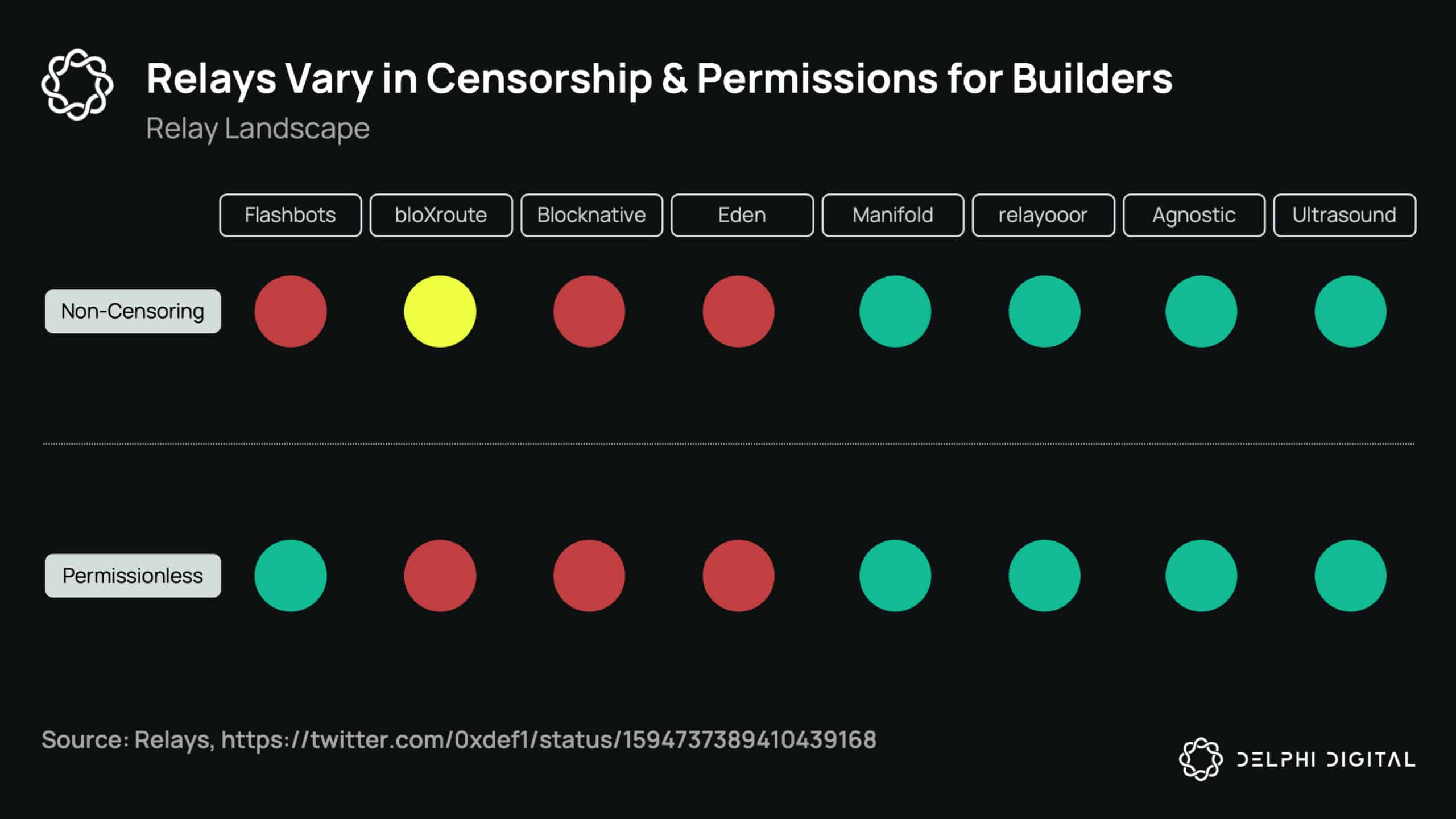

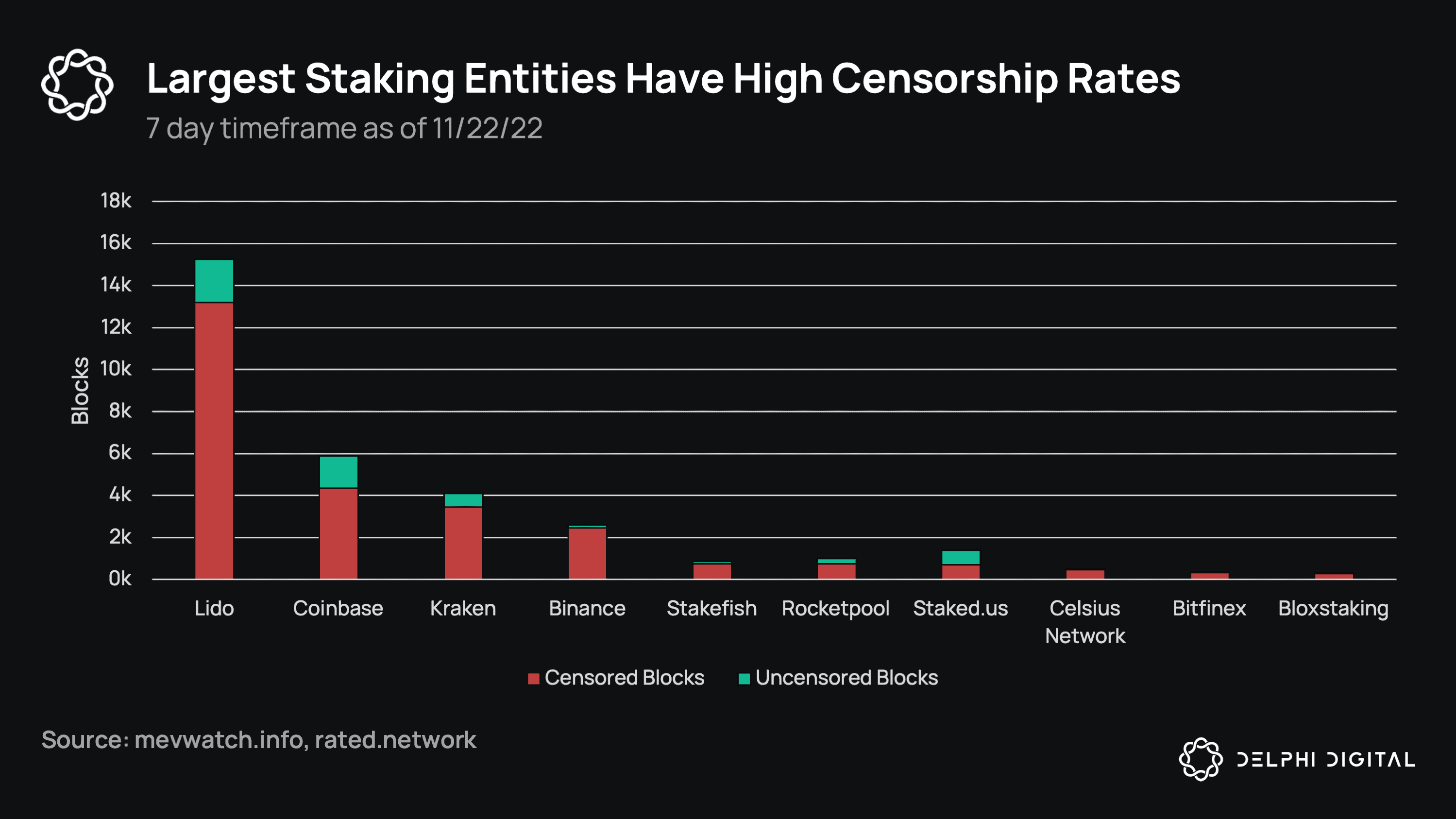

Relays: Receive blocks from builders and send them to proposers. Proposers put trust in relays to accurately assess and send the most profitable blocks, and to reveal the block and pay them upon signing. Some relays have had issues since the merge, like bloXroute sending invalid blocks, a Manifold exploit that allowed builders to submit phantom bids to win blocks, and a vulnerability in which malicious builders could prevent MEV-Boost blocks from landing on-chain.

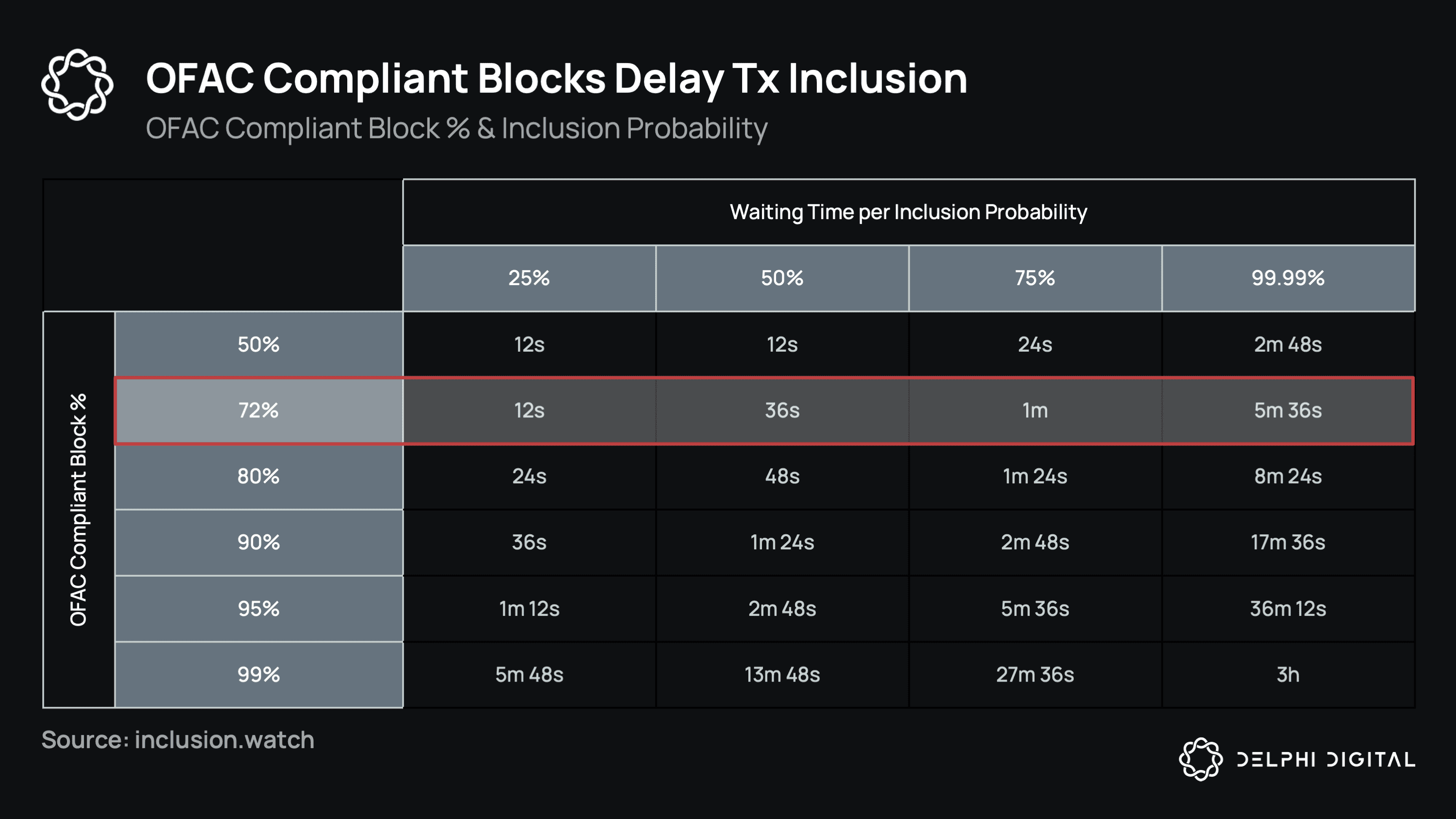

In the long-run, Ethereum will have enshrined PBS and relays won’t be needed. For now, they’re a critical cog in the chain. Relays also vary in their censorship (i.e., OFAC inclusion) and how permissionless they are for builders, as some relays only allow their own builder to connect (Eden, bloXroute, Blocknative).

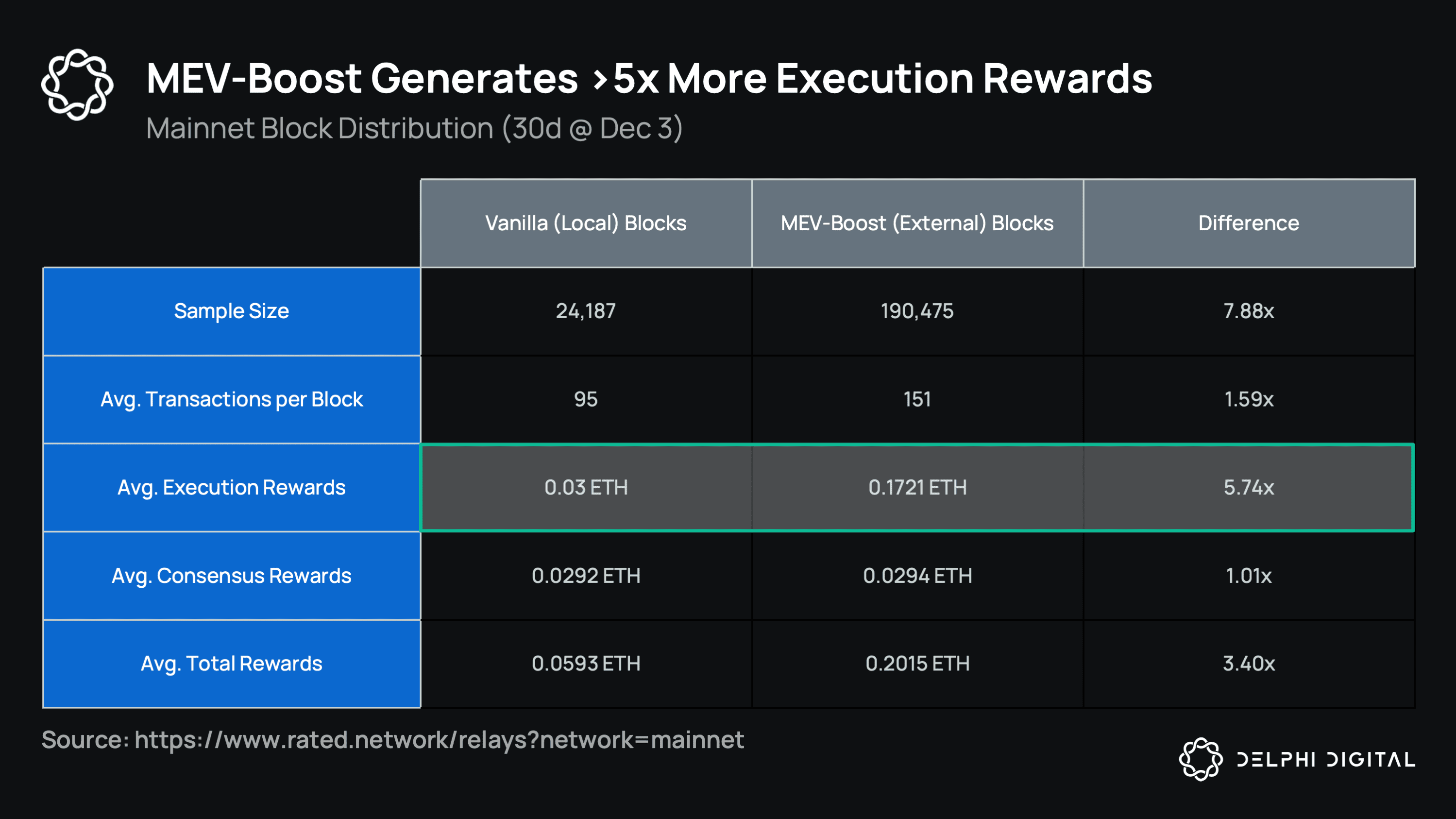

The TL;DR of all this is that MEV-Boost allows validators to maximize their staking rewards by selling their blockspace to an open and competitive market of block builders. For large staking providers like Lido, this means a consistently higher staking yield, with boosted execution layer rewards generating >5x the typical amount of execution rewards that a vanilla/local block would.

The TL;DR of all this is that MEV-Boost allows validators to maximize their staking rewards by selling their blockspace to an open and competitive market of block builders. For large staking providers like Lido, this means a consistently higher staking yield, with boosted execution layer rewards generating >5x the typical amount of execution rewards that a vanilla/local block would.

Execution layer rewards are the validator rewards for, well…executing transactions. Consensus layer rewards are the inflation/block rewards for securing the network. Execution rewards vary significantly, consensus rewards are more stable.

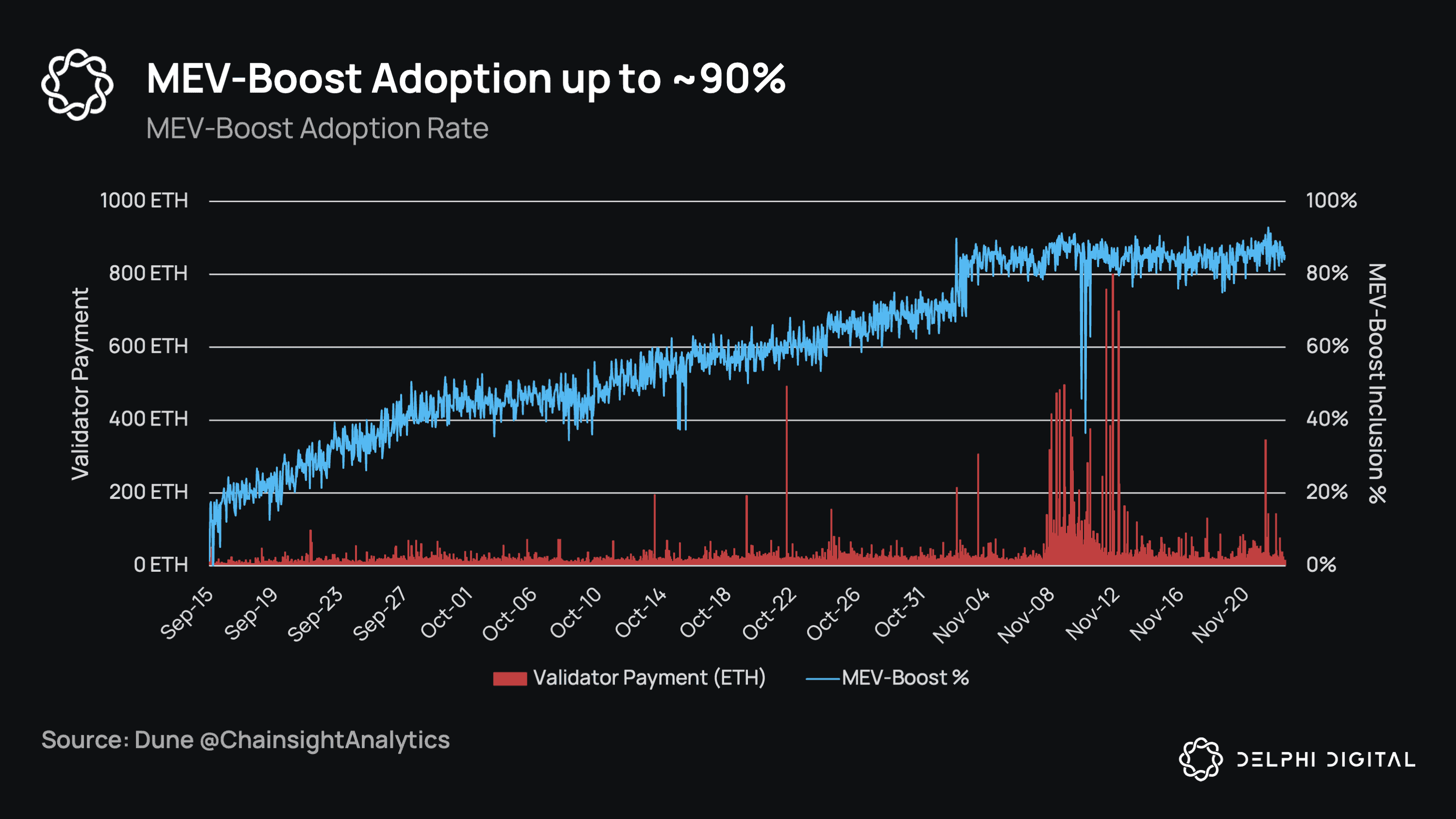

Besides a higher floor staking yield, the upside can be substantial, with the highest MEV-Boost validator payment so far being ~430 ETH ($516k) won by Lido. This is the financial incentive to get people to run home validators — not that they can get a consistent yield on their ETH (they can do so with a liquid staking provider) — but that they can have a shot at being the proposer of a high MEV block, a block that they would never be able to build locally. It is no surprise that MEV-Boost has seen fast adoption since the merge, with nearly 90% of validators already running it after just two months.

Besides a higher floor staking yield, the upside can be substantial, with the highest MEV-Boost validator payment so far being ~430 ETH ($516k) won by Lido. This is the financial incentive to get people to run home validators — not that they can get a consistent yield on their ETH (they can do so with a liquid staking provider) — but that they can have a shot at being the proposer of a high MEV block, a block that they would never be able to build locally. It is no surprise that MEV-Boost has seen fast adoption since the merge, with nearly 90% of validators already running it after just two months.

Back to Ethereum’s MEV design, the motivation for proposer-builder separation (PBS) was to prevent centralization of validators. If only sophisticated validators could extract MEV, then it would become uneconomical for smaller validators who would eventually be forced out. They would be better off just delegating to these top validators instead. This centralization is dangerous, as a small set of validators could more easily censor transactions. To combat this unavoidable centralizing force of MEV, centralization was pushed to the builder role instead, deemed a valid trade-off as long as proposing blocks is decentralized. But a centralized builder role is not without its own downsides.

Back to Ethereum’s MEV design, the motivation for proposer-builder separation (PBS) was to prevent centralization of validators. If only sophisticated validators could extract MEV, then it would become uneconomical for smaller validators who would eventually be forced out. They would be better off just delegating to these top validators instead. This centralization is dangerous, as a small set of validators could more easily censor transactions. To combat this unavoidable centralizing force of MEV, centralization was pushed to the builder role instead, deemed a valid trade-off as long as proposing blocks is decentralized. But a centralized builder role is not without its own downsides.

While isolating centralization to the builder role prevents centralization of validators (and makes base-layer censorship harder), builders can still extract MEV from end users. Block building has a feedback loop where a builder could get access to private order flow, in turn allowing them to create the most profitable (and winning) blocks, and thus leading to more exclusive agreements and private order flow until no one else can compete. MEV is inherent to blockchains; what remains to be seen is how the profits are shared.

A competitive builder market would result in a more balanced distribution of MEV as builders compete on execution guarantees, split profits with users, offer rebates for order flow, etc. A monopoly, on the other hand, would allow a single builder to keep more of these profits themselves, as there would be nowhere else for users to go.

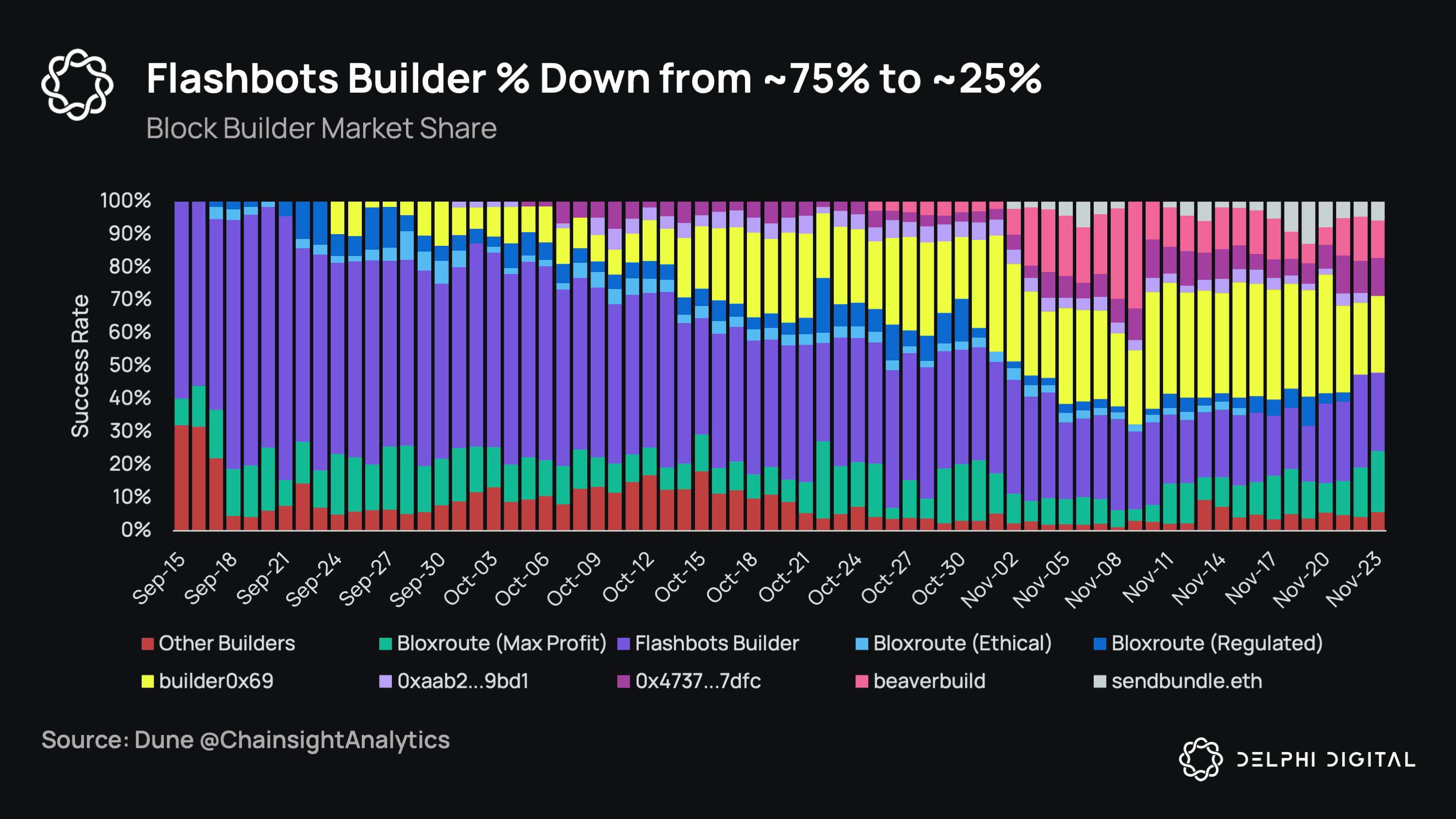

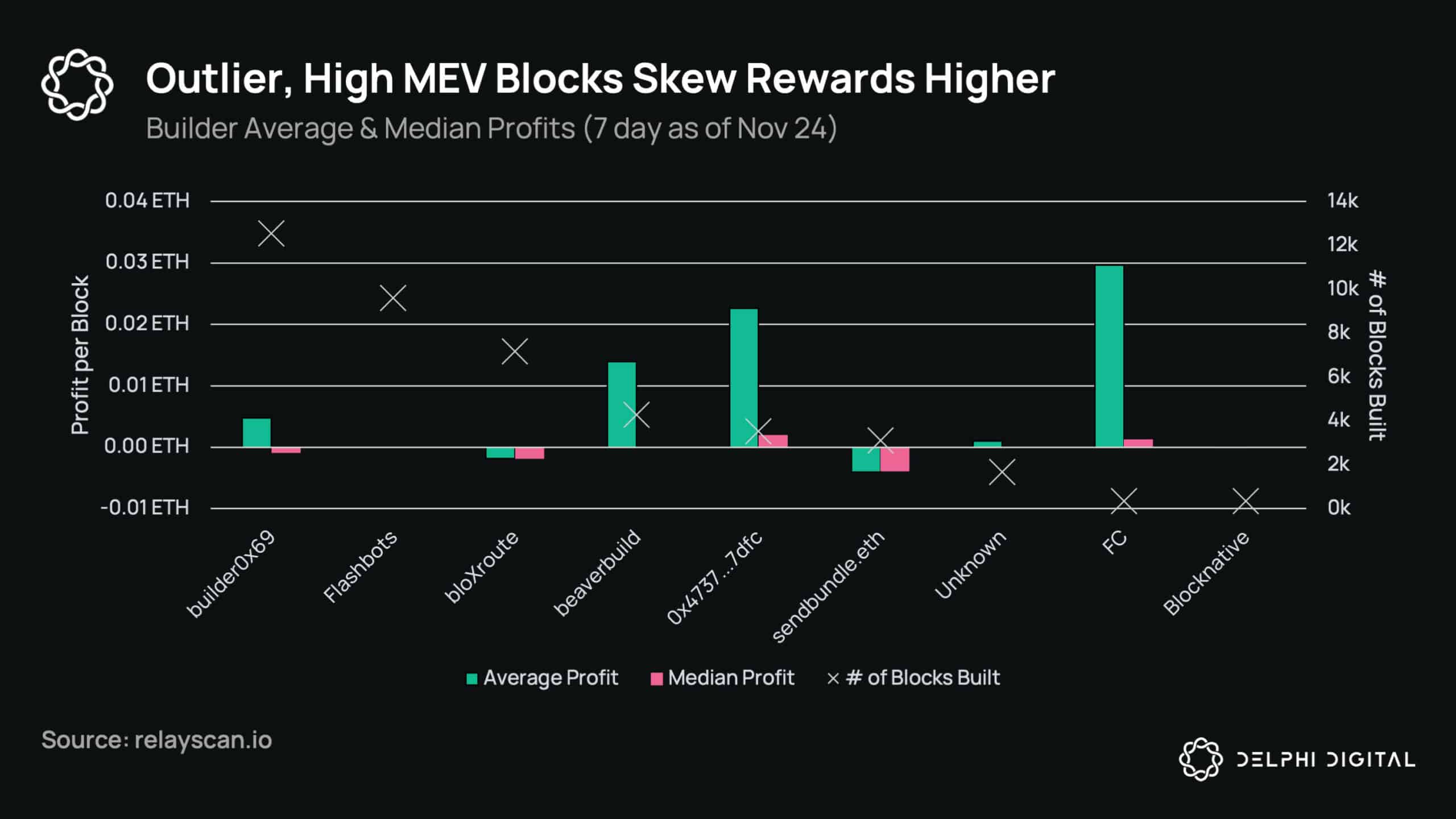

This will be one of the most important areas to watch in the MEV economy in 2023. Today, it’s dominated by about five builders, but recent encouraging signs have emerged as the Flashbots builder is down from 75% to 25% market share, and new builders like builder0x69, beaverbuild, and 0x4737 picking up substantial market share. Flashbots has also recently open sourced their builder to encourage competition.

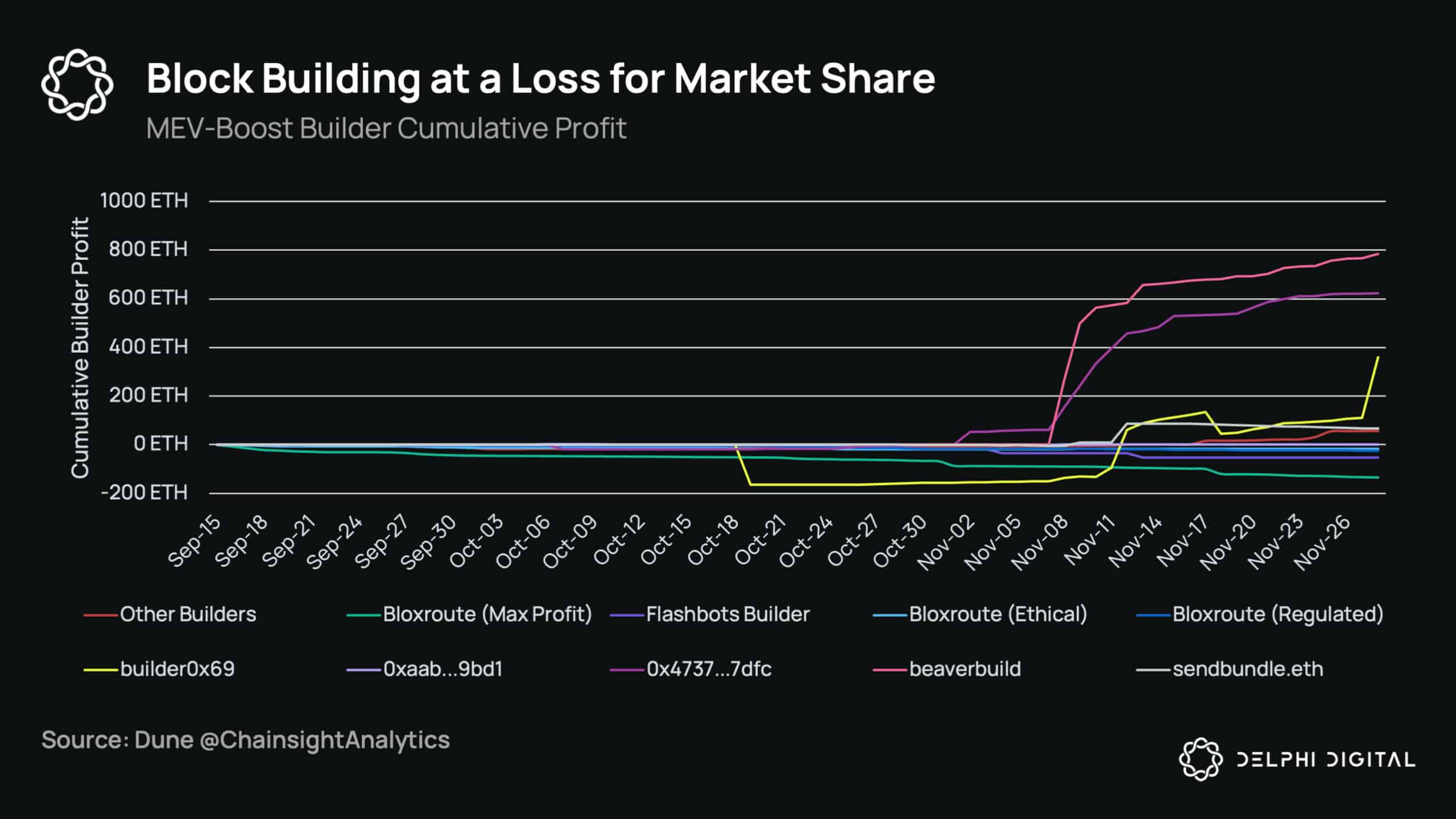

Block building since the merge has mostly been a battle for market share, as builders were passing basically all of their profit (and sometimes even subsidies) to validators. As we discussed above, there are positive feedback loops in being a successful builder, so some have chosen to extract zero or even negative rent for the time being in order to win flow. Bucking this trend are two new builders on the scene — beaverbuild and 0x4737 — who both started building profitable blocks the week of the FTX implosion. Little is known about either (besides beaverbuild’s killer website), but they’re ones to watch in the coming year as competition heats up. The builder market can be summarized as follows:

Block building since the merge has mostly been a battle for market share, as builders were passing basically all of their profit (and sometimes even subsidies) to validators. As we discussed above, there are positive feedback loops in being a successful builder, so some have chosen to extract zero or even negative rent for the time being in order to win flow. Bucking this trend are two new builders on the scene — beaverbuild and 0x4737 — who both started building profitable blocks the week of the FTX implosion. Little is known about either (besides beaverbuild’s killer website), but they’re ones to watch in the coming year as competition heats up. The builder market can be summarized as follows:

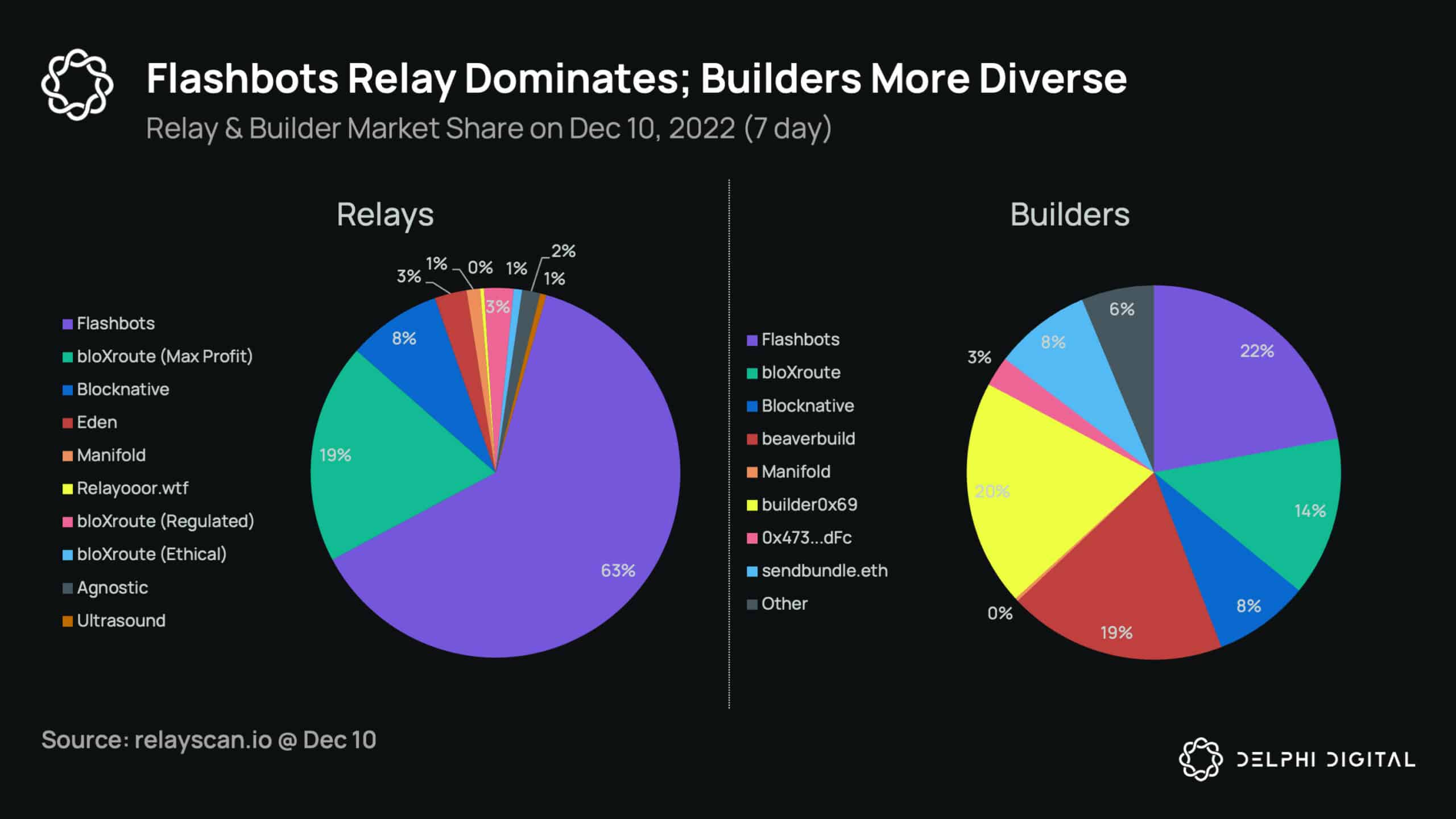

- Flashbots: Run their own builder (which they have open sourced) and the Flashbots relay. Both their builder and relay censor OFAC-sanctioned addresses. The Flashbots builder has connected to other relays to help boost adoption of non-censoring relays.

- bloXroute: Runs their own builder and has three relays: max profit, ethical, and regulated. The max profit relay is the only one with significant adoption, ~18% of relay share.

- Eden: Builds the most profitable blocks on average but has a relatively low inclusion rate. Their relay only allows their own builders.

- builder0x69: Started operations mid-October. Operated at a loss for a while before beginning to turn a profit recently, and now makes up ~20% of blocks. They subsidize blocks to increase order flow (discussed below) and created the relayooor non-censoring relay.

- beaverbuild: New builder that started in November and already has the most cumulative profit to date.

- sendbundle.eth: Newer builder that has been able to garner a consistent 5-10% builder share, although does so by operating at a loss.

- 0x4737: New builder that started around the same time as beaverbuild and has also been quite profitable.

- Manifold: Runs a builder, relay, and RPC service. There have been talks of Sushi integrations to capture, distribute, and share MEV with “SushiGuard,” although it is not yet live and TBD.