1. Key Takeaways

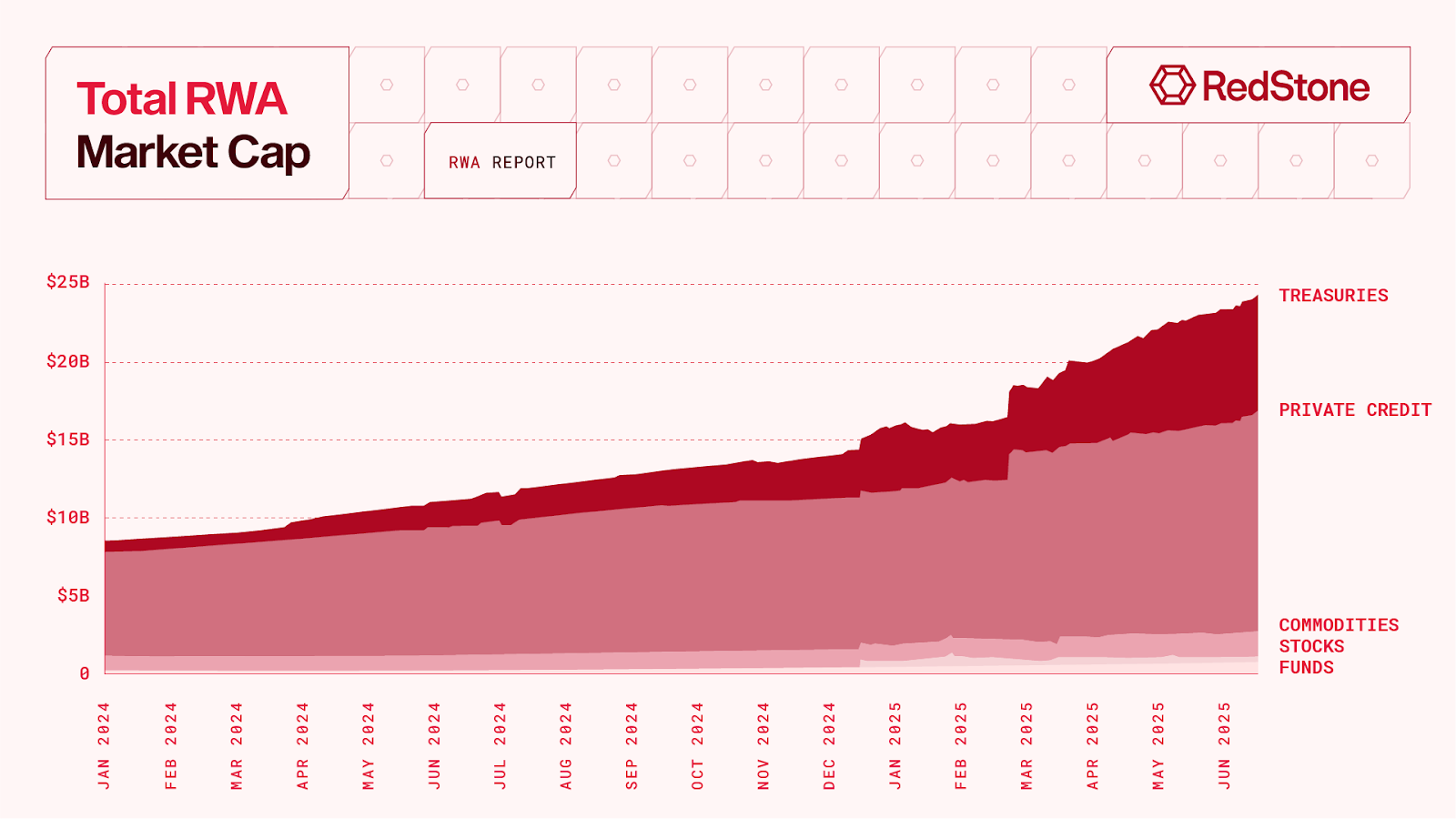

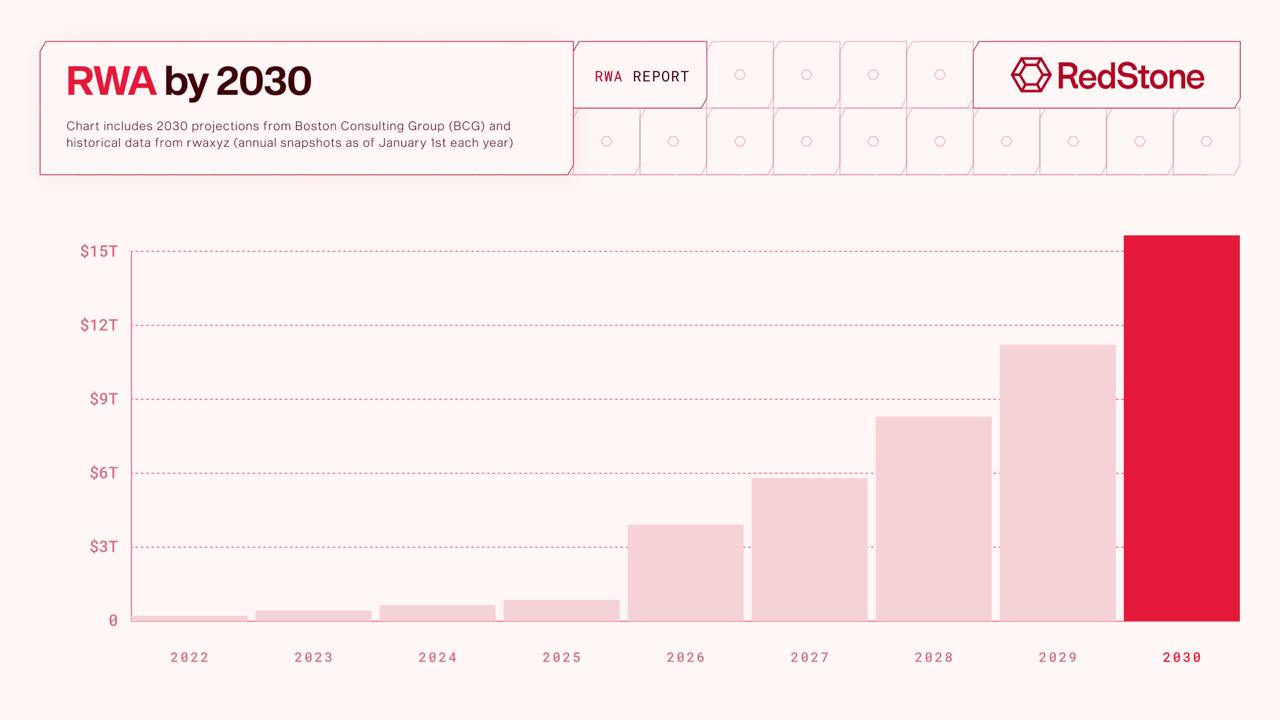

- RWA tokenization exploded from $5B in 2022 to over $24B by June 2025 (+380%), making it crypto’s 2nd fastest-growing sector after stablecoins. While stablecoins are technically tokenized fiat currencies, we exclude them from this report as our research team is already working on in-depth material about them. Industry projections suggest 10-30% of global assets could be tokenized by 2030-2034, positioning RWAs are bridging traditional finance’s $400+ trillion in assets to blockchain – over 130x larger than crypto’s current ~$3 trillion market cap.

- Asset tokenization has decisively transitioned from experimental pilots to scaled institutional adoption in 2024-2025. The tokenized real-world asset market reached $15.2 billion by December 2024 (excluding stablecoins) and continued the growth reaching over $24B by June 2025 – a remarkable 85% year-over-year expansion.

- The current institutional adoption wave represents years of infrastructure development culminating in production-scale deployment. Major financial institutions including BlackRock, JPMorgan, Franklin Templeton, and Apollo have moved beyond experimentation, while governments increasingly recognize blockchain as essential infrastructure for modernizing legacy financial systems and addressing fundamental macroeconomic challenges of the decade. Catalyzed by a friendlier regulatory environment towards tokenization, RWAs are positioned to proliferate.

- DeFi integration through regulated frameworks is unlocking RWAs’ next growth phase, transforming historically illiquid assets into composable financial primitives. Platforms like Ethena, Maple, Spark, Morpho, Pendle Citadels, Drift Institutional, Kamino and Securitize’s sToken framework enable institutional assets to access DeFi liquidity while maintaining compliance, creating yield amplification and secondary market opportunities impossible in traditional finance.

- Private credit has emerged as the largest RWA tokenization segment at $14 billion as of June 2025, demonstrating institutional appetite for blockchain-native credit markets. Tokenization addresses the sector’s primary constraints by lowering operational costs, improving accessibility and distribution, while creating potential for robust secondary liquidity markets. They maintain institutional underwriting standards and offering high-yield opportunities previously restricted to accredited investors.

- RWA oracles represent a fundamental shift requiring entirely new technological paradigms, with specialized providers like RedStone pioneering the sophisticated pricing mechanisms tailored to institutional adoption. Unlike DeFi’s real-time price feeds, RWA pricing demands complex architectures that blend Net Asset Value calculations, regulatory compliance, and illiquidity adjustments—establishing the critical infrastructure foundation for trillion-dollar tokenized asset integration into DeFi.

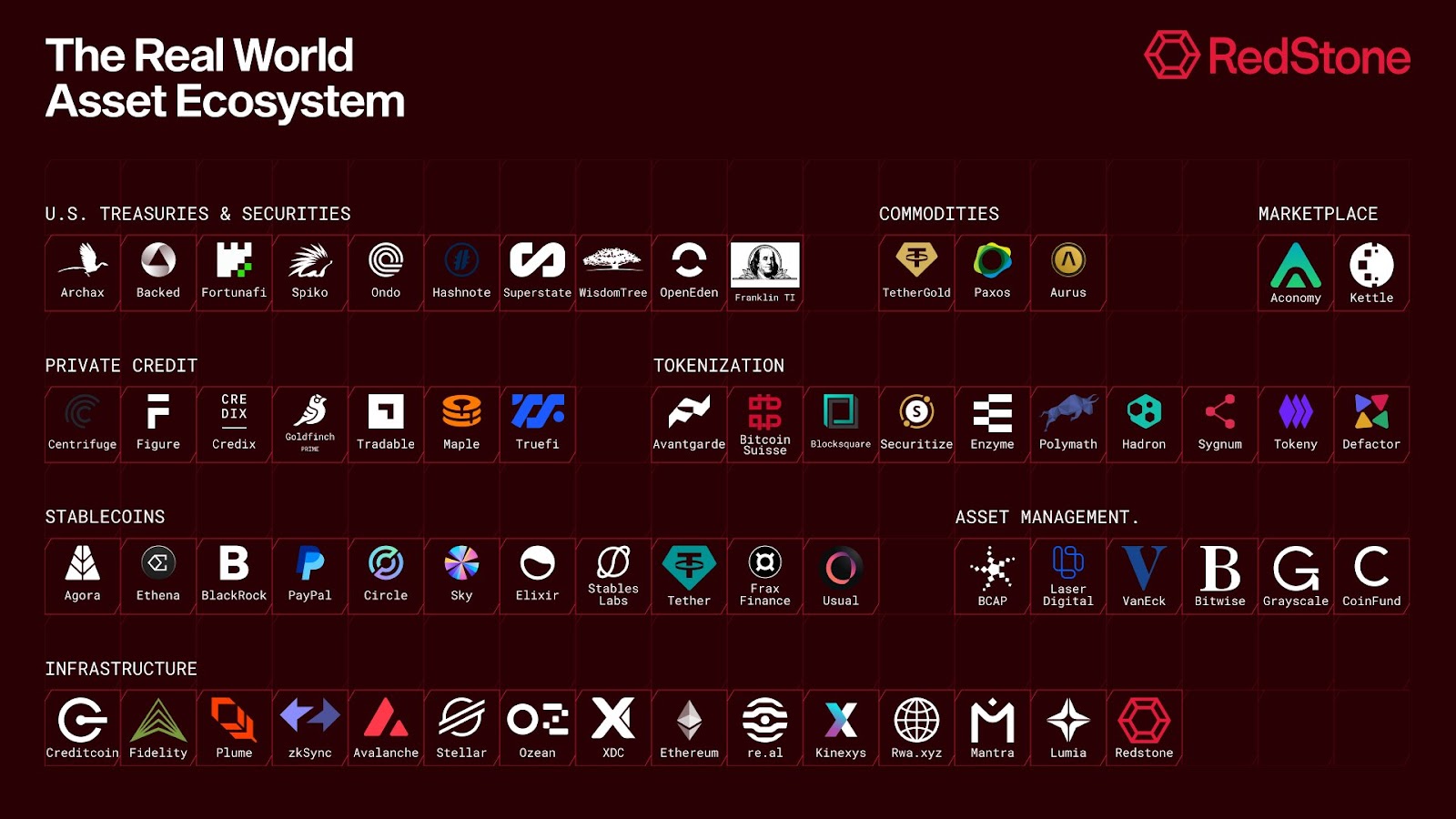

Featured Projects and Organizations

RedStone, as the author of the report, would like to express true gratitude to all the contributors, projects, and key opinion leaders who helped us create such a comprehensive piece on the RWA landscape. Starting with big gratitude towards Gauntlet and RWA.xyz teams, especially the research department, for their diligent and timely work. The depth and breadth of this report wouldn’t be possible without these individuals – thank you to Tarun Chitra, Simon Mathonnet, Carson Brown, Rahul Goyal, Bryan Choe, Reid Simon, Justin Pesola, Adam Lawrence, Grant Hummer, Marco Cora, Nadine Chakar, Denelle Dixon, Eric Saraniecki, Sid Powell, Sam MacPherson, and many more!

| Institutions | Multi-Asset Platform | Private Credit | U.S. Treasuries | Tokenization Infrastructure | Chains | dApps |

BNY Mellon | Robinhood | Apollo (ACRED) | BlackRock (BUIDL) | Securitize | Ethereum | Morpho |

Stripe | Revolut | Hamilton Lane (SCOPE) | VanEck (VBILL) | Tradable | Solana | Ethena |

Visa | Coinbase | Maple | Franklin Templeton (BENJI) | Ondo | Stellar | Spark |

Mastercard | Kraken | Tradable | Superstate (USTB) | Superstate | Plume | Sky |

Abu Dhabi Mubadala | Bybit | Figure | Ondo (OUSG & USDY) | Paxos | Polygon | Drift Institutional |

Wisconsin Pension Fund | Fidelity | Janus Henderson (JTRSY) | Tether Holdings | XRP Ledger | Kamino | |

Moody’s | Circle (USYC) | Centrifuge | Converge | Pendle Citadels | ||

Goldman Sachs | OpenEden (TBILL) | Circle | Canton Network | Maple | ||

BNP Paribas | Spiko (USTBL) | WisdomTree | Collateral Appchain (DTCC) | Aave Horizon | ||

Franklin Templeton | Fidelity (FIUSD) | Hadron by Tether | Kinexys (JP Morgan) | Pendle | ||

BlackRock | WisdomTree (WTGXX) | Sygnum Bank | Ondo Chain | |||

JPMorgan Chase | ZkSync | |||||

VanEck | Aptos | |||||

State Street | Avalanche | |||||

Base | ||||||

Ink |

Find out from JP Morgan, Moody’s, DTCC, and more experts on where RWAs are headed next at RWA Cannes, June 30 2025.

Don’t miss RWA Summit series and the upcoming edition in Cannes, July 1 2025.

2. What are RWAs?

Real-World Assets (RWAs) refer to tangible or traditional financial assets that exist in the off-chain world but are represented and traded on blockchain networks. In crypto terminology, RWA specifically denotes assets from the traditional world that get tokenized onchain – essentially anything that exists outside the crypto-native ecosystem.

This spans a broad spectrum: tangible assets like real estate, gold, and oil; financial instruments such as government bonds, loans, and equity shares; and even intangible rights like intellectual property royalties. The key characteristic is that these digital tokens represent a claim on real assets – whether that’s actual gold bullion in a vault, US dollars held in reserve, or ownership stakes in physical property.

The “real-world” label serves an important purpose in distinguishing these assets from purely digital tokens created within crypto ecosystems like BTC or ETH. RWAs are fundamentally different because they’re backed by physical assets or legal contracts in traditional finance, then brought onto blockchain rails. This tokenization process enables onchain ownership and transfer of these assets, combining the liquidity, transparency, and 24/7 access of blockchain with the economic stability and value of traditional assets.

It’s worth noting that in traditional banking, RWA also stands for “Risk-Weighted Assets” – a completely different concept related to regulatory capital requirements. In our context, we’re always referring to Real-World Assets and their digital representations on blockchain networks.

A quick history look at RWA and tokenization

Pre-Blockchain Precursors

Many believe that the story of RWAs starts no sooner than blockchain technology emerged, which isn’t entirely true. Financial engineers were already trying to fractionalize and broaden the ownership of real-world assets like estates and commodities long before onchain was even a concept.

Picture this: it’s the 1960s, and someone has a brilliant idea – what if ordinary people could own a piece of massive commercial real estate without needing millions of dollars? Enter Real Estate Investment Trusts (REITs), which basically chopped up skyscrapers and shopping malls into bite-sized, tradable pieces. A few decades later, Exchange-Traded Funds (ETFs) did the same magic trick with everything from gold bars sitting in Swiss vaults to entire stock market indices.

These weren’t just financial products – they were early experiments in asset democratization. Take E-Gold in the late 1990s, which offered digital gold certificates that you could redeem for actual physical bullion. Sounds familiar? It was essentially tokenization before we had the word for it. Users could transfer “digital gold” instantly across borders, representing real metal stored in warehouses.

But here’s where the story gets interesting – and messy. E-Gold collapsed under regulatory pressure and operational nightmares, highlighting a fundamental problem that plagued all these pre-blockchain attempts: they were built on trust, not truth. Every REIT needed management companies, every ETF required custodians, and E-Gold depended on a single company keeping honest books about what gold actually existed.

The key challenge wasn’t innovation – it was infrastructure. Without distributed ledgers, these models were trapped by intermediaries and single points of failure, making global peer-to-peer transfer a pipe dream rather than a reality.

Why Blockchain Changed the Game

The breakthrough came with Bitcoin in 2009, but it was Ethereum’s launch in 2015 that truly opened the floodgates. What made blockchain tokenization fundamentally different wasn’t just the technology – it was the elimination of the trust problem that had plagued every previous attempt.

Think about E-Gold’s fatal flaw: when regulators came knocking or when operational issues arose, the entire system could be shut down because it relied on a single company maintaining honest records. Blockchain flipped this script entirely. Smart contracts on Ethereum allowed complex ownership and transfer rules to be encoded directly onchain, with automated enforcement that didn’t require anyone to “trust” a central authority.

The early experiments were admittedly rough around the edges. Bitcoin’s Colored Coins tried to represent real assets on the blockchain, but the technology was rudimentary and regulatory frameworks were virtually non-existent. However, these pioneering efforts proved something crucial: you could create digital representations of real assets that were truly peer-to-peer, globally transferable, and resistant to single points of failure.

Stablecoins became the first major validation of this concept. Starting with USDT in 2014, these tokens essentially took fiat currency and put it onchain. The fact that this market has grown to over $250 billion according to analytics platform DeFiLlama, demonstrates massive demand for bringing real-world value into the digital realm – but with blockchain’s superior infrastructure backing it.

Recent Momentum: The Perfect Storm

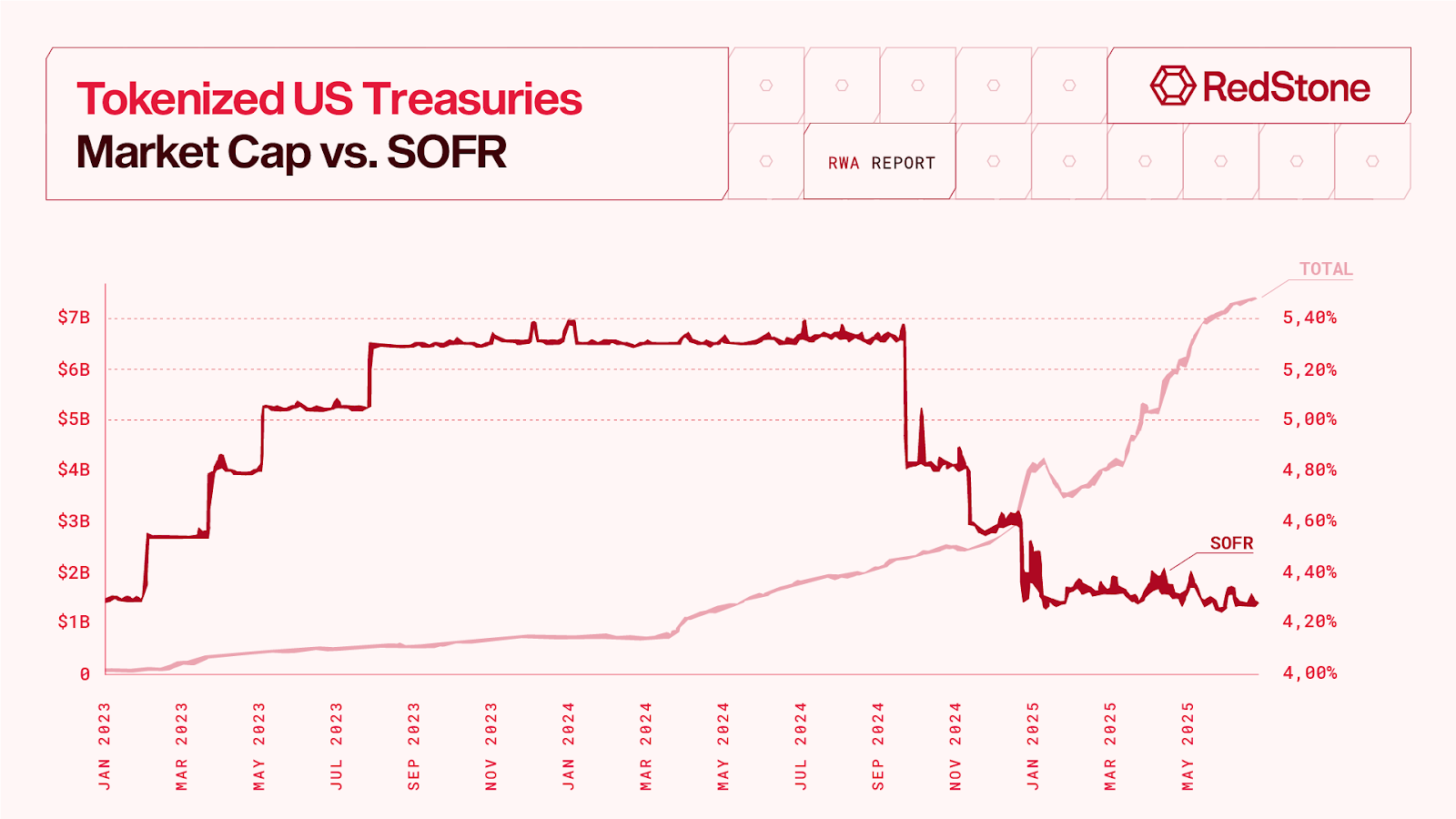

By the end of 2022, several forces were converging to create what industry insiders call the start of the “RWA moment.” Rising global interest rates suddenly made traditional yield-bearing assets like the U.S. Treasuries attractive again, but crypto investors wanted to access these returns without leaving the blockchain ecosystem. We can see there’s a positive correlation between Tokenized US Treasuries Market Cap and SOFR, however the tokenized US Treasuries market cap shows a significant lag in responding to SOFR changes.

Note: 🔍 You can click on the chart to zoom in

The timing couldn’t have been better. Large institutions were finally becoming comfortable with blockchain technology, and regulatory clarity was improving in key jurisdictions. Major asset managers and fintech firms started tokenizing everything from U.S. Treasury bill funds to portions of private equity funds on both public and permissioned blockchains.

The numbers tell the story: the onchain RWA market exploded from roughly $5-10 billion in 2022 to over $20 billion by mid-2025. In just the first half of 2025 alone, the RWA token market surged approximately 260%, growing from $8.6 billion to over $23 billion in value.

The momentum reflects more than just crypto enthusiasm – major institutions are taking notice. BlackRock’s CEO Larry Fink has stated that “the next generation for markets will be the tokenization of securities.” Industry projections vary widely, with the Boston Consulting Group suggesting that 10% of global GDP (roughly $16 trillion) could be tokenized by 2030, while Standard Chartered estimates up to $30 trillion in tokenized assets by 2034.

Source: BCG

This represents a significant shift: traditional finance is beginning to recognize that blockchain infrastructure offers capabilities that previous attempts at asset digitization couldn’t deliver – namely, global accessibility, enhanced liquidity, and reduced reliance on intermediaries.

Why USD and Treasuries Dominate the RWA Space

When discussing RWAs in crypto, U.S. dollar assets – particularly USD currency and U.S. Treasury bills – consistently take center stage. This isn’t a coincidence; it’s the result of nearly 80 years of economic history that established the dollar as the backbone of global finance.

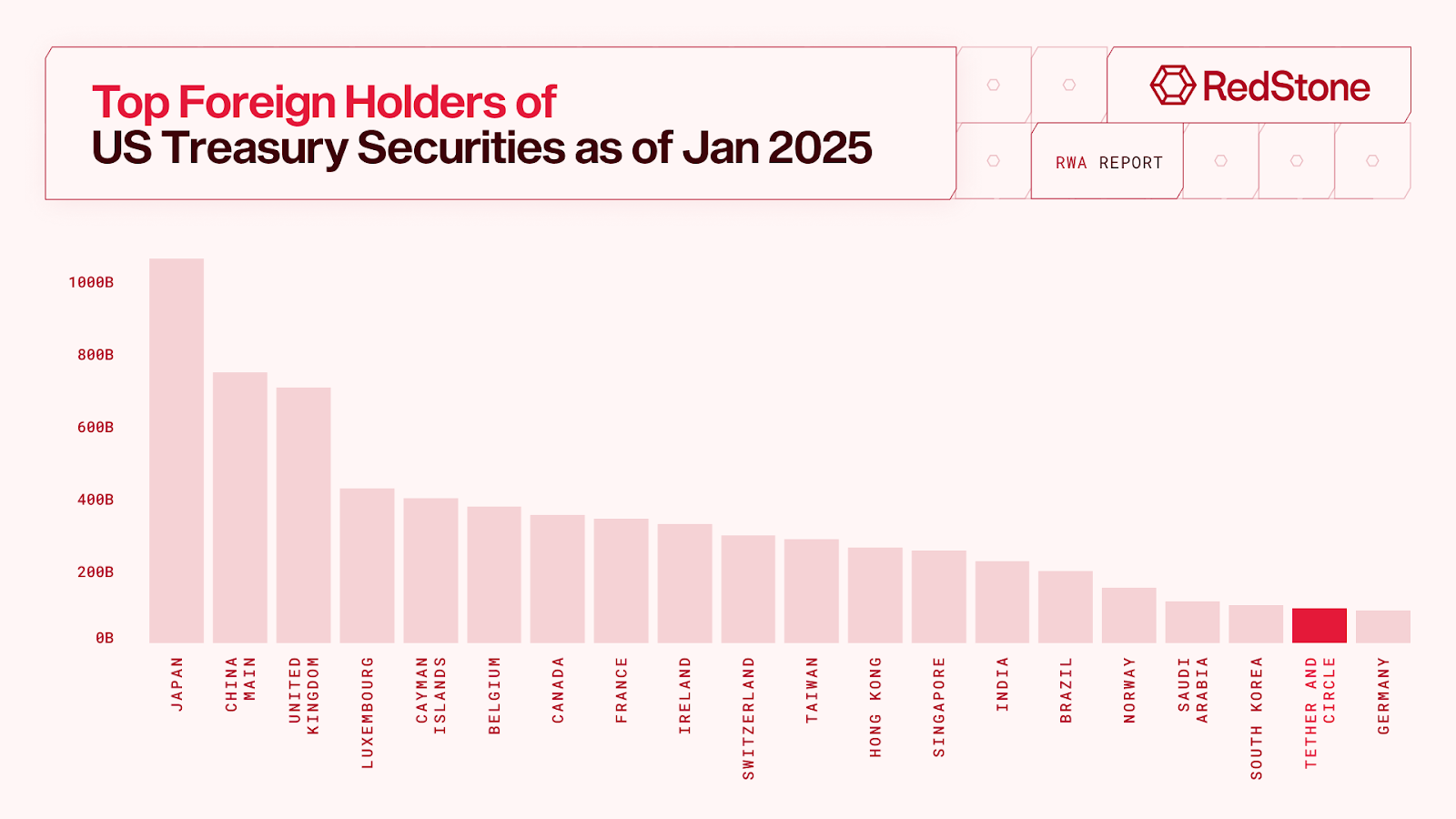

The story begins in 1944 with the Bretton Woods agreement, which pegged global currencies to the dollar and cemented USD’s status as the world’s primary reserve currency. Even after the gold standard was abandoned in 1971, the dollar’s dominance persisted through the petrodollar system and the sheer size and stability of the U.S. economy. Today, roughly 58% of official foreign exchange reserves worldwide are held in U.S. dollars – far ahead of the euro’s 20% share. This translates into real numbers that matter: central banks globally hold the bulk of their reserves in USD-denominated assets, with much of that invested in U.S. Treasury securities. The Treasury market represents the largest bond market in the world, with about $28.8 trillion outstanding and unrivaled liquidity. Foreign governments and investors alone hold roughly $9 trillion of that debt, underscoring its role as the ultimate global reserve asset.

Why this matters for crypto becomes clear when you consider that there has historically been “no obvious alternative” matching the depth, stability, and credit quality of U.S. Treasuries. High-quality government bonds serve as the bedrock of institutional portfolios – used to park capital safely and as collateral for other investments. The crypto world is simply tapping into these same fundamentals, but the relationship runs even deeper than many realize. While Bitcoin dominated early crypto activity, USD denomination quickly became the industry standard. As early as 2014-2015, most crypto financial activity shifted to USDT-based trading pairs and transactions. This wasn’t just a temporary preference – it represented a fundamental recognition that stable value measurement was essential for meaningful commerce.

Over the years, this USD-centric approach has only strengthened. Today, more than 30 stablecoin issuers maintain circulating supplies exceeding $100 million each, creating a diverse ecosystem of dollar-pegged tokens. The scale has become genuinely remarkable: combined, Tether and Circle would rank as the 18th-largest holder of U.S. debt globally – trailing South Korea but surpassing Germany. This positions two crypto companies among the world’s most significant Treasury holders.

Source: Ark Invest

The 2020 DeFi boom amplified this trend dramatically. As decentralized finance captured increasing market share, billions in “Total Value Locked” flowed into smart contracts – with liquidity providers earning trading fees and users benefiting from direct onchain trading, almost all denominated in USD-equivalent tokens.

This evolution reveals something important: crypto hasn’t been building an alternative to the dollar system – it’s been building a more efficient infrastructure for dollar-based finance. USD stablecoins like USDC and USDT give traders stable currencies for transactions, backed by the same bank deposits and short-term treasuries that traditional institutions rely on. Tokenized Treasury products allow crypto investors to earn reliable 4-5% annual yields with minimal risk – a compelling alternative to volatile DeFi yield farming.

From the ground up, crypto has embraced the dollar as its unit of account, making the integration of traditional USD-denominated assets a natural evolution rather than a forced adoption.

Source: RedStone

3. Tokenization

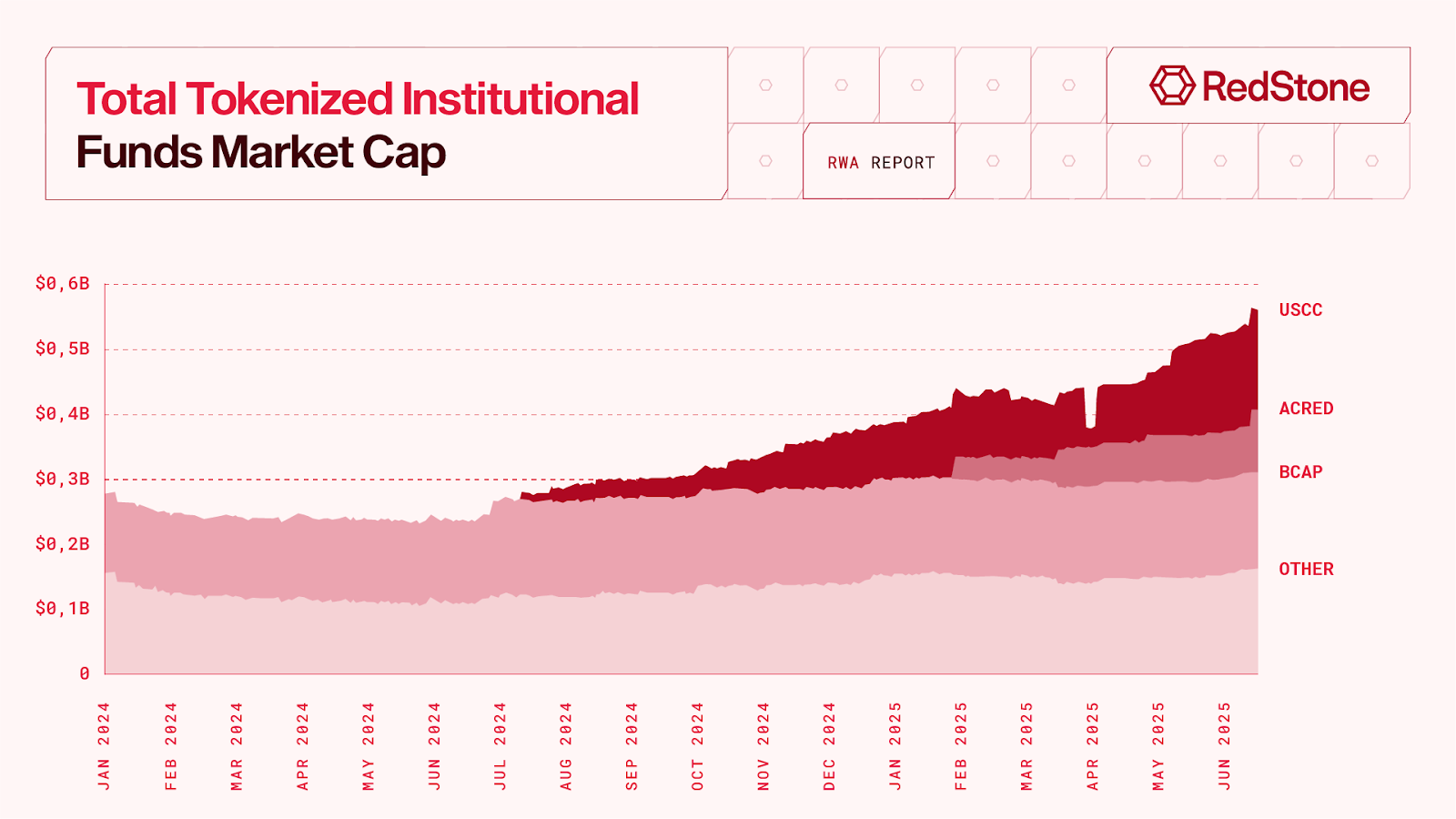

Asset tokenization has decisively transitioned from experimental pilots to scaled institutional adoption in 2024-2025. The tokenized real-world asset market reached $15.2 billion by December 2024 (excluding stablecoins) and continued the growth reaching over $24B by June 2025. This remarkable 85% year-over-year expansion signals the technology’s maturation as major financial institutions deploy production-scale solutions.

RWA tokenization brings structural advantages such as:

- Revolutionary liquidity transformation represents tokenization’s most significant breakthrough. Traditional private markets require millions in minimum investments with 7-10 year lock-up periods. Tokenization enables fractional ownership with investments as low as $1,000 and 24/7 secondary market trading. Private equity funds that historically required million dollar size of commitments can now offer $100,000 minimums through tokenized shares, democratizing access to institutional-grade investments.

- Settlement revolution eliminates the archaic T+2 settlement cycle that has plagued traditional markets since 1995. Tokenized securities settle instantly through blockchain networks, reducing counterparty risk and capital requirements. This breakthrough enables intraday yield accrual – investors earn proportional returns for partial-day holdings rather than waiting for month-end distributions.

- Programmable compliance automates regulatory requirements through smart contracts, eliminating manual processes prone to human error. KYC/AML verification, accredited investor status, and transfer restrictions execute automatically. Dividend distributions, voting rights, and corporate actions trigger programmatically, reducing operational costs significantly compared to traditional fund administration.

- Global accessibility breaks down geographical barriers that have historically fragmented capital markets. A tokenized real estate fund can simultaneously serve investors in New York, London, Singapore, and Dubai through blockchain infrastructure, with multi-currency settlement and automated tax reporting. This borderless access dramatically expands investor pools while reducing distribution costs.

Major platforms compete through innovation and scale

| Name | Category | Biggest Assets Issued | RWA Total Value | Market Share | RWA Holders |

Securitize | Multi-Asset Platform | BUIDL, ACRED, VBILL, SCOPE, EXOD, BCAP,MI4, and more | $4B | 28.2 | 1,103 (excluding MI4) |

Tradable | Private Credit | Tokenized private credit exposure | $2.06B | 16.2% | — |

Ondo | U.S. Treasuries | OUSG, USDY | $1.36B | 10.7% | 15,578 |

Superstate | Multi-Asset Platform | USTB, | $856M | 6.8% | 95 |

Paxos | Commodities | PAXG | $851M | 6.7% | 65,799 |

Franklin Templeton | U.S. Treasuries | BENJI | $741M | 5.8% | 637 |

Tether Holdings | Commodities | XAUT | $679M | 5.4% | 8,400 |

Centrifuge | U.S. Treasuries | JTRSY | $409M | 3.2% | 7 |

Circle | U.S. Treasuries | USYC | $359M | 2.8% | 41 |

WisdomTree | Multi-Asset Platform | WTGXX, FLTTX, WTGOLD and more | $323M | 2.6% | 1,474 |

Top 10 RWA issuers as of June 26, 2025. Data source: rwa.xyz. Note: Securitize figures adjusted with fund data not available on rwa.xyz.

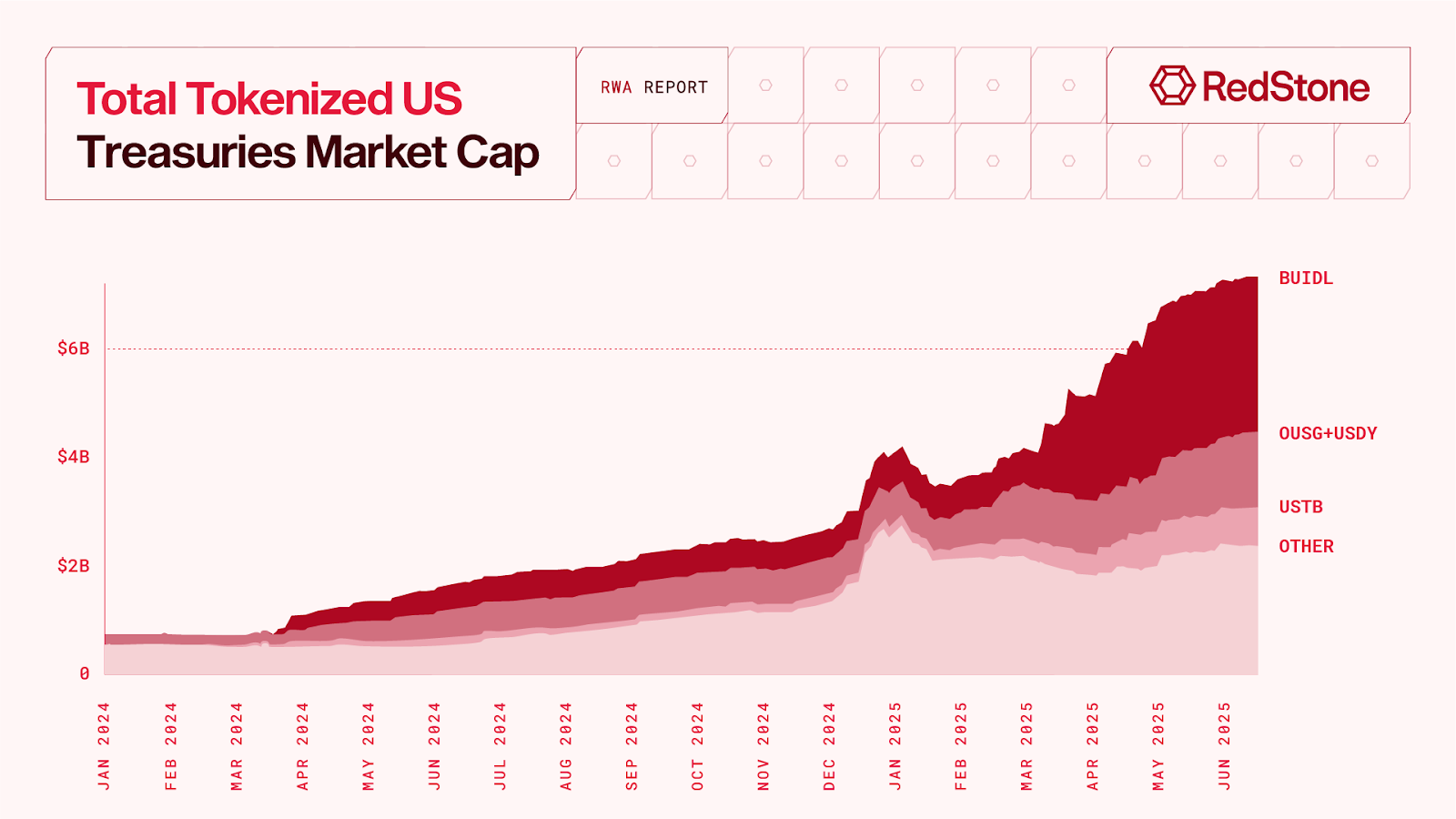

T-bills market demonstrates explosive institutional demand

The tokenized Treasury bills market exemplifies institutional blockchain adoption at scale, growing from $100 million in January 2023 to approximately $7.5 billion by June 2025 – a staggering 7,400% expansion. BlackRock’s BUIDL dominates with 40% market share ($2.9+ billion AUM), offering the best-in-class short term treasury yield across seven blockchains with Ethereum holding 93% of supply.

Franklin Templeton’s BENJI follows with $750 million AUM, attracting investors with its low 0.15% management fee. Ondo Finance’s USDY pioneered the yield-bearing approach for individual non-US investors, achieving over $650 million AUM by bootstrapping operations with zero management fees. The market demonstrates high concentration, with six major funds controlling 88% of all tokenized U.S. treasuries.

There are currently two major approaches to structuring tokenized T-bills onchain: yield-bearing and rebasing mechanisms. Yield-bearing tokens such as Ondo’s USDY and Circle’s USYC accrue underlying yield through increased asset pricing via various mechanisms. Under this model, USDY’s price six months from now will be higher than today due to accumulated yield. Conversely, rebasing tokens such as BlackRock’s BUIDL and Franklin Templeton’s BENJI maintain dollar parity by distributing yield through newly issued tokens at predefined intervals.

T-bills represent the ideal entry point for institutional tokenization adoption, providing ultra-low risk backed by U.S. government “full faith and credit” with well-established legal frameworks and predictable yields. The 24/7 trading capability and instant settlement contrast sharply with traditional market limitations, making them attractive for institutions seeking regulatory clarity and proven demand.

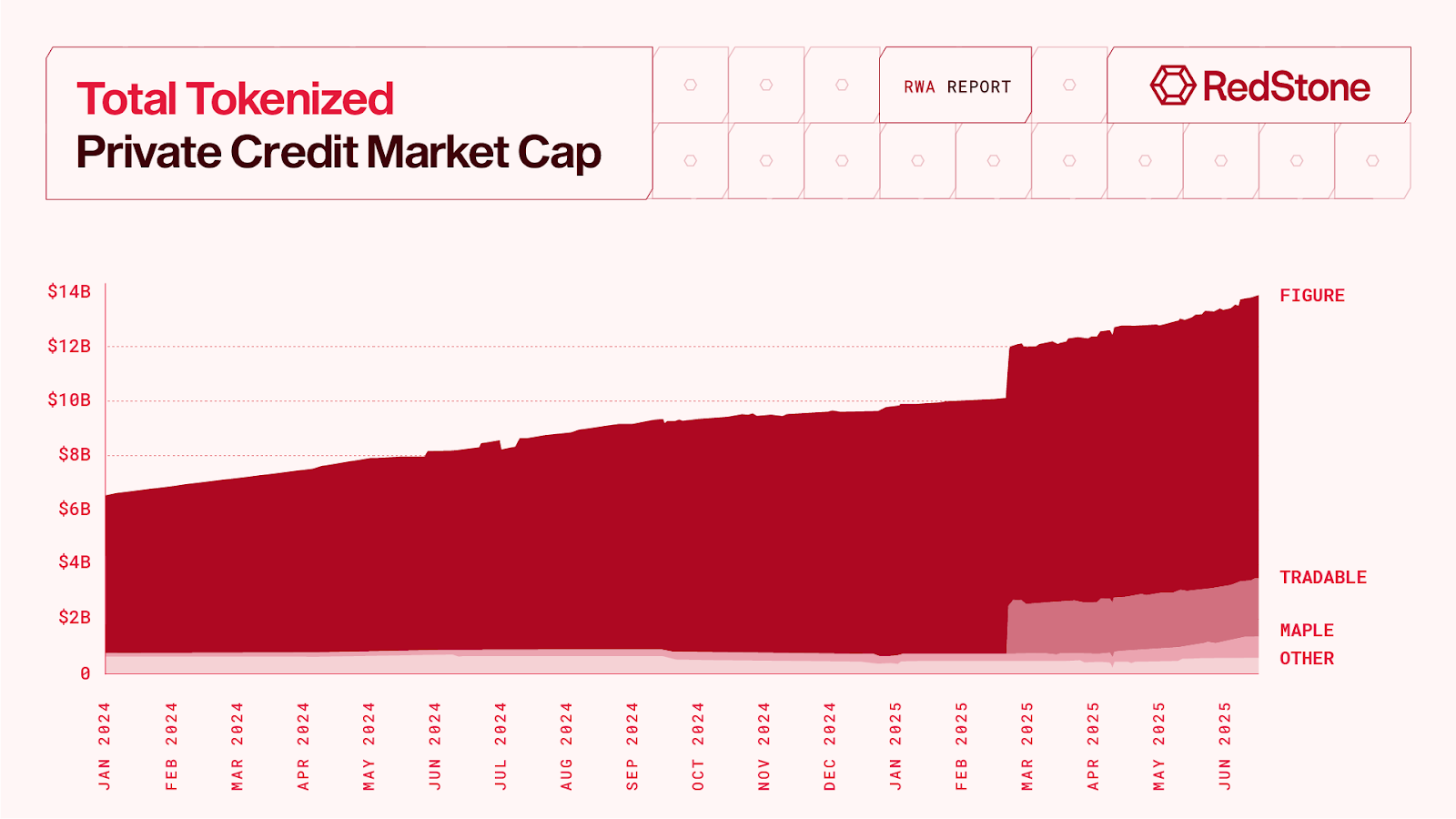

Private credit emerges as largest RWA tokenization segment

Tokenized private credit reached $14 billion, making it the largest RWA tokenization segment. The global $2 trillion private credit market projected to reach $3 trillion by 2028 presents massive tokenization opportunities. Figure dominates the tokenized private credit sector with over $10 billion in active loans, primarily Home Equity Lines of Credit tokenized on Provenance blockchain.

Apollo’s ACRED issued by Securitize demonstrates institutional innovation through sACRED’s DeFi integration, enabling yield amplification up to 16% through leverage looping strategies on Morpho, Kamino and Drift Institutional. The fund charges just 1.5% management fees with no carry, dramatically undercutting traditional 2% plus 20% carry structures.

Private credit offers attractive 8-12% yield premiums with portfolio diversification benefits uncorrelated to public markets. Tokenization addresses private credit’s primary pain point – liquidity – while maintaining institutional-grade underwriting standards. This combination of higher yields and improved liquidity makes private credit another optimal entry point for institutions exploring tokenization, complementing T-bills’ low-risk profile with higher-return opportunities.

Learn more about the potential of tokenized private credit and its applications in DeFi in our dedicated article.

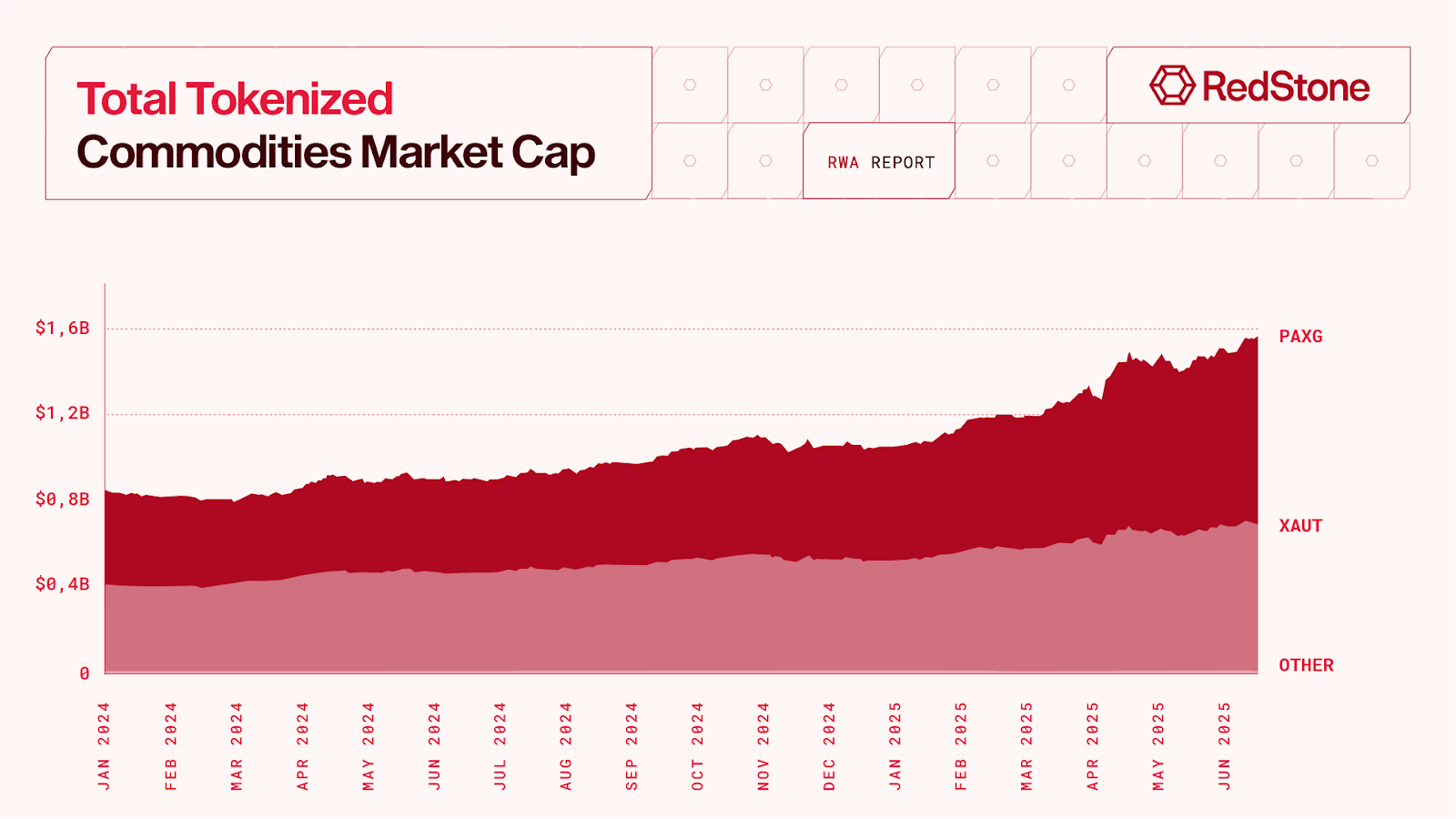

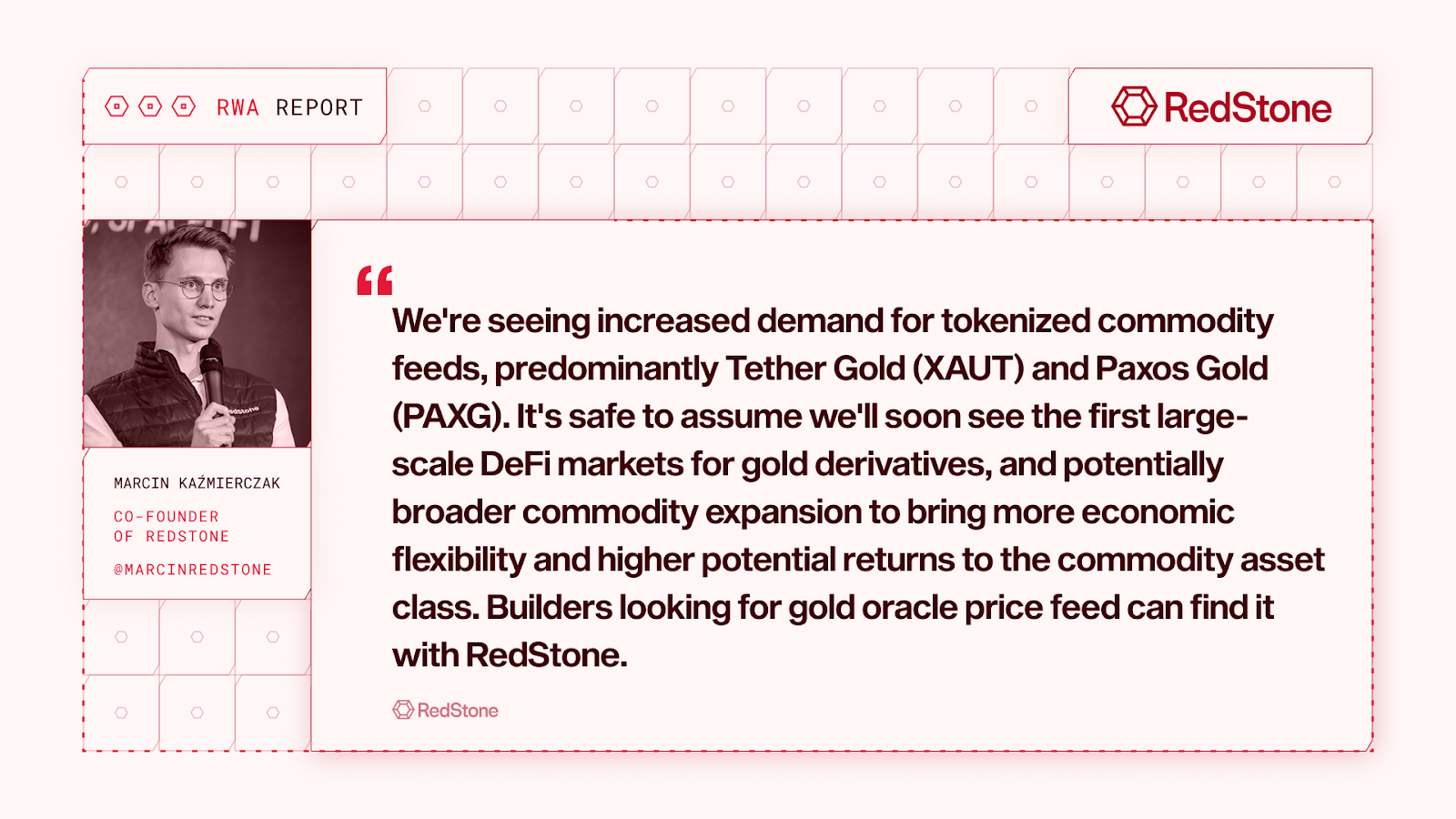

Commodities tokenization dominated by gold with emerging diversity

The commodities tokenization market reached $1.6 billion by June 2025, with gold representing nearly 100% of tokenized commodities. Paxos Gold (PAXG) leads with approximately $850 million market capitalization, offering tokens backed 1:1 by London Good Delivery gold bars stored in Brink’s vaults. Tether Gold (XAUT) follows closely with +$650 million market cap, providing divisibility down to 0.000001 XAUT.

Innovation extends beyond precious metals with Uranium Digital raising $7.8 million to create the first institutional-grade uranium spot trading platform on Solana blockchain. The platform addresses lack of financialization in uranium markets while capitalizing on nuclear energy’s revival driven by AI infrastructure power requirements. Founder Alex Dolesky reports “exceptional demand” from traditional market participants seeking exposure to uranium without physical settlement complexities.

The Rise of Tokenized Equity Markets

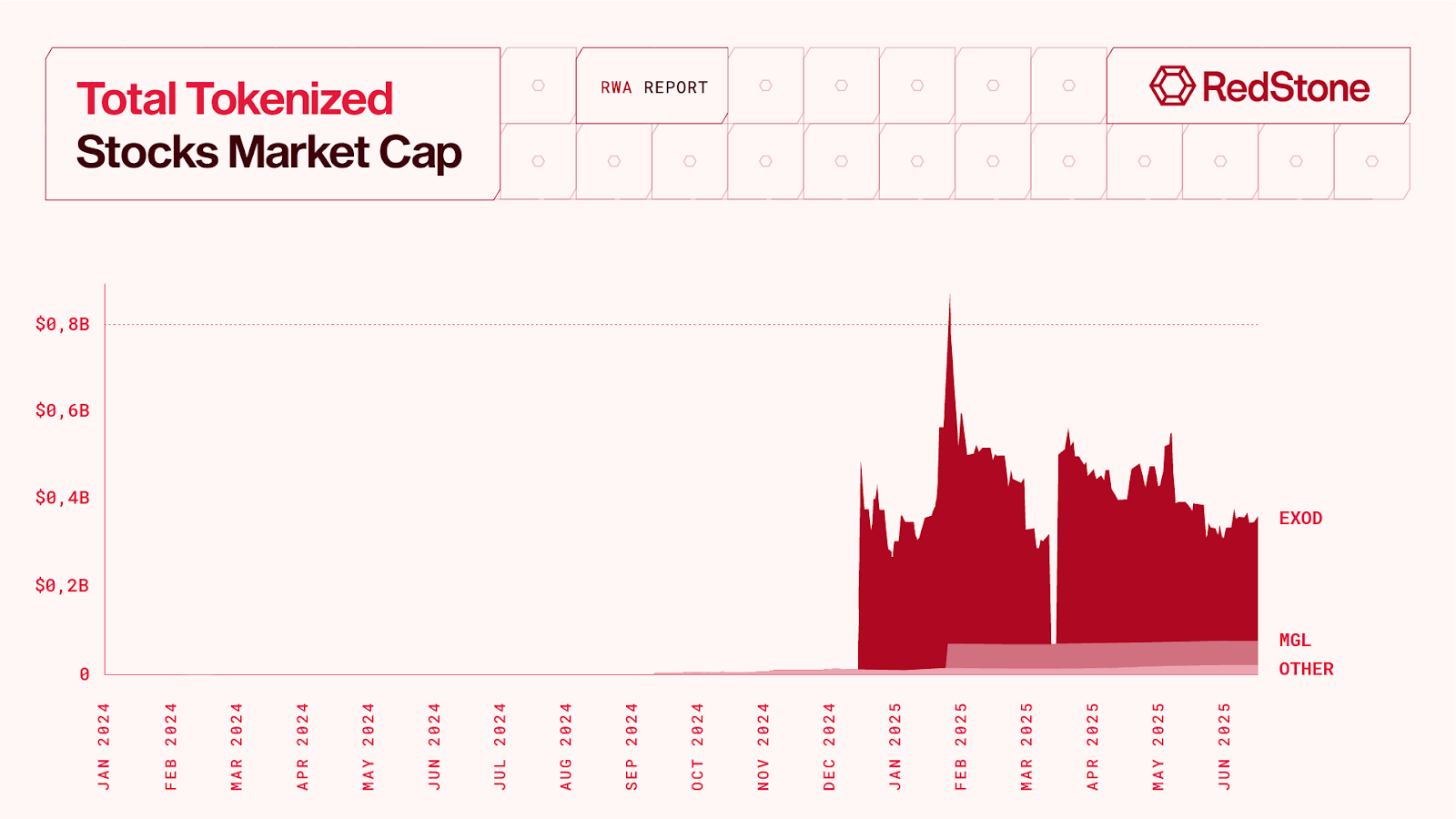

The equity tokenization landscape is evolving rapidly, though it’s crucial to distinguish between early-stage stock trading on crypto platforms and true blockchain-native tokenization. While having the possibility for users to trade traditional equity instruments on centralized exchanges doesn’t necessarily mean these assets are tokenized at their core, this represents a definitive first step toward full tokenization adoption.

However, exchanges aren’t the only innovators driving this transformation. The Exodus-Securitize partnership demonstrates how established crypto companies can pioneer genuine blockchain-native securities, creating the largest tokenized stock offering to date with their over $900 million market capitalization using Algorand’s infrastructure and SEC-compliant transfer systems. This precedent proves that true tokenization creates unprecedented optionality for ownership and trading that traditional platforms cannot replicate.

The strategic positioning becomes even more compelling when considering that both Coinbase and Kraken have developed strong vertical integration through their respective Layer 2 blockchain platforms – Base and Ink – which could eventually enable users to hold and trade these assets directly onchain just as any native blockchain instruments.

Crypto exchanges drive the convergence narrative

- Coinbase has positioned tokenized equities as a “huge priority,” with Chief Legal Officer Paul Grewal actively seeking SEC approval to offer blockchain-based stock trading. The company’s journey reflects the broader industry evolution – originally attempting to tokenize its own COIN stock during the 2020-2021 IPO before facing regulatory barriers. Now, emboldened by the Trump administration’s crypto-friendly stance and the establishment of a new SEC crypto task force, Coinbase has revived these ambitious plans in 2025, leveraging its Base Layer 2 network as potential infrastructure for future tokenized equity settlements.

- Kraken took a more aggressive approach, successfully launching xStocks in May 2025 through a strategic partnership with Backed Finance. The platform is soon to offer tokenized versions of 50+ U.S. stocks and ETFs including household names like Apple, Tesla, and Nvidia. Built on Solana blockchain, xStocks enables 24/7 trading for non-U.S. customers across Europe, Latin America, and select global markets, with the revolutionary capability of using tokenized stocks as collateral in ways that are simply not possible through TradFi.

- Bybit pursued a different path, expanding beyond crypto to offer U.S. stocks and commodities trading in May 2025. CEO Ben Zhou announced direct access to major stocks like Apple and Microsoft alongside commodities including gold and crude oil. While Bybit’s approach enables direct stock trading with USDT rather than full tokenization, it bridges traditional finance and crypto markets for over 60 million global users across a comprehensive multi-asset trading hub.

Private equity tokenization gains global momentum

Private equity represents tokenization’s ultimate prize, where the technology could solve decades-old structural problems. Traditional private equity suffers from extreme illiquidity with 7-10 year lock-ups and $25+ million minimums. Tokenization could democratize these investments through fractional ownership, liquid secondary markets, and 24/7 trading that could unlock trillions in dormant capital from the $4.5 trillion global PE market.

The Jupiter-Kazakhstan Stock Exchange partnership formalized in May 2025 creates a dual listing mechanism where companies complete traditional IPOs on AIX while simultaneously issuing tokenized shares on Solana. Major corporations including NAC Kazatomprom (world’s largest uranium producer) are to benefit from this hybrid approach. Behind the scenes, similar initiatives are developing across jurisdictions worldwide, with governments and financial institutions quietly exploring tokenization frameworks that could fundamentally reshape capital markets infrastructure in the coming years.

Note: All tokenized RWA capitalization data in this section is sourced from rwa.xyz, the industry-standard data platform for tokenized real-world assets (RWAs), and is current as of June 26th 2025.

4. RWA meets DeFi: Connectivity, Challenges and Breakthrough Solutions

The integration of Real-World Assets (RWAs) into decentralized finance (DeFi) represents one of the most significant multi-surface challenges in blockchain finance, but at the same time could mean one of the biggest growth opportunities for the whole DeFi space, unlocking tremendous growth potential by accessing traditional finance AUM. This convergence demands bridging the gap between traditional finance’s strict compliance requirements and DeFi’s permissionless architecture—a challenge that has spawned innovative solutions across technical standards, regulatory frameworks, and protocol design.

How to Institutionalize DeFi?

Picture this: you’re browsing a DeFi protocol, ready to invest in tokenized real estate or corporate bonds, but suddenly hit a digital velvet rope. “Accredited investors only,” it reads. This fundamental tension lies at the heart of bringing traditionally restricted assets into DeFi’s open environment. Under US regulations, most tokenized RWAs require accredited investor status—meaning you as an individual need either $1 million in net worth, $200,000+ annual income, or hold certain professional financial credentials like Series 7, 82, or 65. This creates barriers that on the surface contradict DeFi’s permissionless ethos, establishing a two-tier system where institutional-grade assets remain gated while retail users can have very limited access to these products.

But here’s where it gets technically interesting: this regulatory requirement creates a fascinating technical challenge on how to most effectively gatekeep and whitelist users for tokenized products onchain. There are three main approaches defining RWA tokenization: chain-level (permissioned chains), dApp-level (white-glove DeFi), and asset-level permissions (tokens with whitelisted mint and transfer functions). Each approach involves different trade-offs between security, user experience, and maintaining DeFi’s composability. The industry has extensively tested these models, with hybrid combinations now dominating implementation strategies.

An intriguing pattern has emerged in DeFi strategy construction. Through iterative development, builders discovered that bilateral restrictions aren’t necessary—strategies can operate with asymmetric permission structures. Consider money markets pairing permissioned tokenized treasuries (restricted to accredited investors) with unrestricted stablecoin pools accessible to retail participants. This architecture allows restricted assets to tap public liquidity while maintaining compliance boundaries.

The implications extend beyond individual protocols. Institutional assets gain access to DeFi’s deepest liquidity pools without regulatory compromise, while retail capital providers access yield streams traditionally reserved for accredited investors. These permissioned DeFi experiments continue revealing practical requirements for institutional adoption, demonstrating how traditional finance integrates with decentralized protocols through selective rather than comprehensive restrictions.

These insights crystallized through hard-won lessons from early institutional experiments. Aave Arc’s failure in 2022 revealed that regulatory compliance alone doesn’t guarantee adoption—despite attracting 30 whitelisted institutions, the permissioned pool achieved only $8 million peak TVL before shutting down. Flux Finance followed a similar trajectory, despite initially finding product-market fit through leveraged Treasury exposure. Launched by Ondo Finance in 2023, Flux created hybrid markets supporting both permissionless stablecoins and permissioned treasuries, targeting arbitrage opportunities between Treasury yields and DeFi borrowing costs. While the protocol demonstrated technical viability and achieved temporary adoption, it ultimately ceased operations, reinforcing that sustainable institutional DeFi requires more than compelling economics and regulatory clarity.

Both experiments highlighted critical challenges: permissioned pools face inherent liquidity constraints, market timing significantly impacts adoption, and the institutional DeFi value proposition must extend beyond compliance to address fundamental operational needs.

Looking at the current landscape of institutional DeFi adoption, several protocols have emerged as clear market leaders, demonstrating how tokenized products are reshaping traditional finance infrastructure. These platforms have moved beyond proof-of-concept implementations to capture billions in institutional capital through sophisticated tokenization strategies.

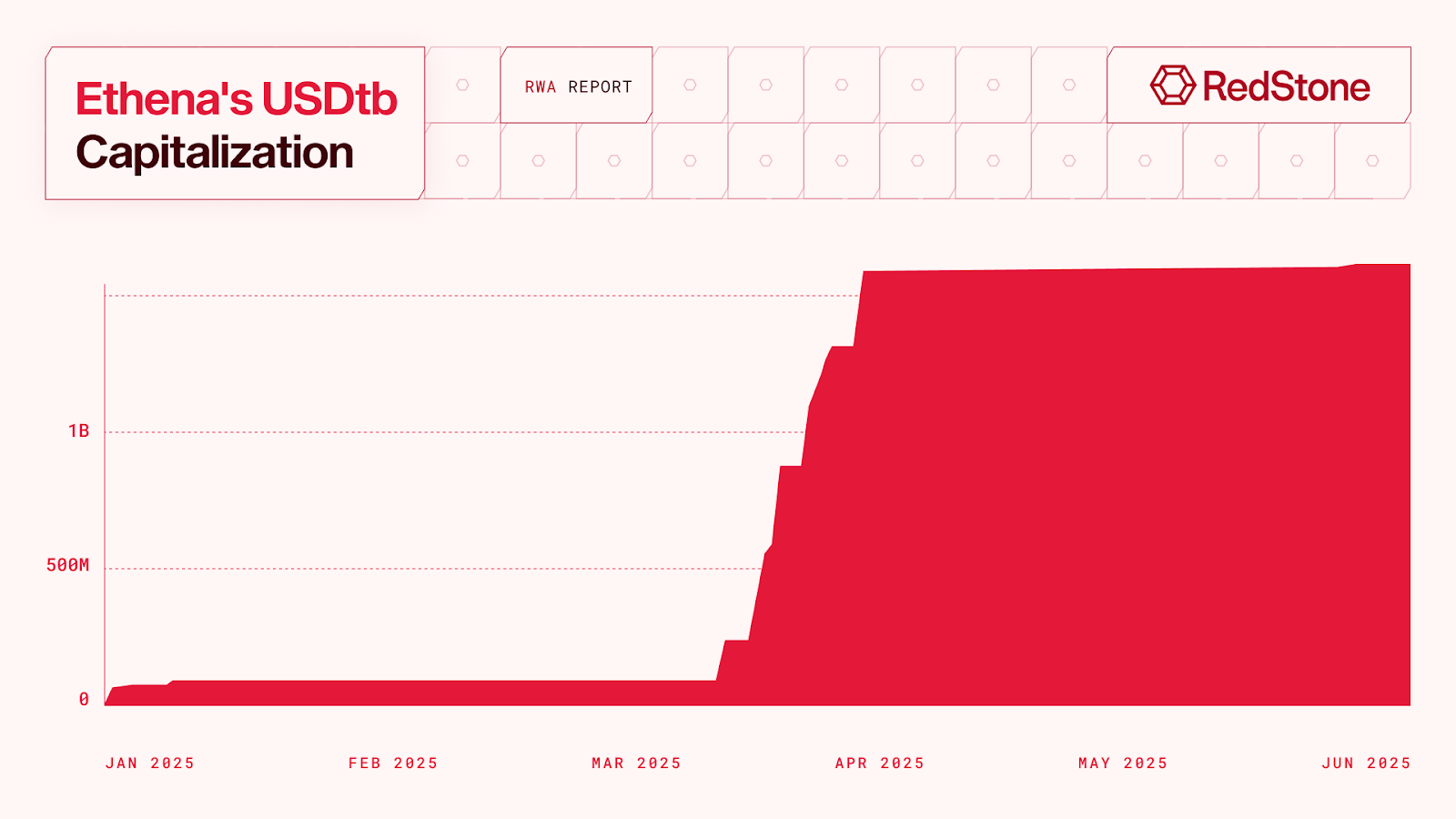

Ethena’s USDtb Drives Institutional Adoption Through BUIDL

Ethena’s USDtb has become a critical revenue driver for the protocol’s flagship USDe product, with the Risk Committee approving USDtb as a primary backing asset during periods when delta-neutral funding strategies reach local minimums. This strategic diversification allows Ethena to maintain safe margins while continuing yield generation when perpetual funding rates turn unfavorable against the protocol. USDtb’s explosive growth—growing to the sheer $1.5 billion size, becoming the 8th largest stablecoin by March 2025 based on DefiLlama data all in less than 6 months since inception—stems from its conservative backing structure, with 90% of reserves held in BlackRock’s BUIDL fund through Securitize’s tokenization infrastructure.

The system has attracted premier institutional partners including Copper, Zodia Custody, and Coinbase Institutional for custody services, while Jump Trading, Cumberland, and Amber Group provide institutional-grade liquidity. This institutional backing has been responsible for over 50% of the BUIDL Fund size, pushing BlackRock’s tokenized treasury fund to $2.9 billion capitalization by the end of May 2025. USDtb serves dual functions: providing low-risk collateral for margin trading on centralized exchanges and offering compliant treasury exposure during unfavorable funding environments.

The addition of USDtb backing for USDe has indirectly catalyzed the explosive growth of sophisticated DeFi yield strategies, particularly enabling the creation of robust money markets for Pendle’s split principal (PT) and yield tokens (YT)—instruments that traditional finance recognizes as interest rate markets. USDtb backing provides crucial yield floor stability (typically 4-5% APY) during periods when crypto derivatives funding rates turn negative or compress significantly. This predictable minimum yield foundation is essential for PT token valuation and AAVE’s oracle systems, enabling more accurate pricing models and safer liquidation mechanisms for zero-coupon bond mechanics.

The diversified yield structure allows DeFi participants to lock in fixed yields through PT tokens while speculating on multiple components: crypto volatility driving derivatives funding rates, ETH staking rewards, and traditional Treasury yields. This multi-factor yield generation creates the complexity that mature interest rate markets require, while the Treasury backing provides institutional comfort for larger capital allocations.

Market dynamics strongly support this thesis. As of June 2025, sUSDe and eUSDe PT markets across AAVE, Morpho, Euler, and Silo have accumulated over $2 billion in TVL across various maturity dates. This supply-demand imbalance creates a positive feedback loop that has legitimized USDe as a foundational asset for DeFi’s evolution toward sophisticated fixed-income markets, mirroring traditional finance structures while maintaining crypto’s unique composability advantages.

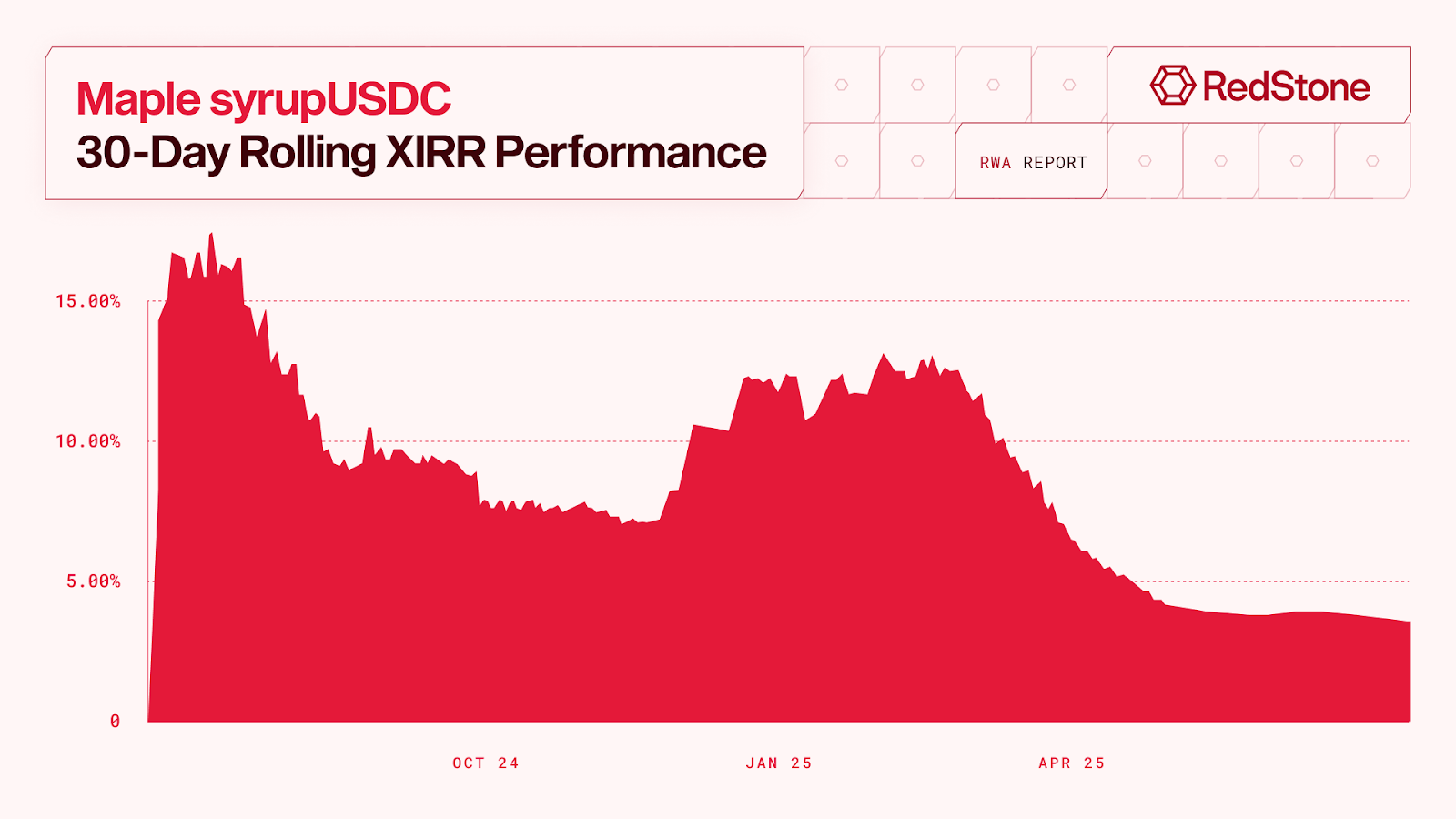

Maple Finance Accelerates Institutional Lending Onchain

Maple Finance surged past $1 billion in assets under management in 2025, establishing itself as DeFi’s premier institutional lending marketplace. Following extraordinary 1,500% growth in 2024, the protocol crossed $2 billion by mid-2025, representing one of DeFi’s most dramatic institutional adoption stories. Maple doesn’t tokenize traditional assets but bridges the gap between traditional finance and crypto by originating and matching sizable institutional loans.

The biggest growth accelerator for Maple’s operations has been the Earn platform (prev. syrup.fi), launched in mid-2024, which democratizes access to institutional yields previously reserved for accredited investors. This innovative platform aggregates retail capital into institutional-sized pools, allowing everyday DeFi users to earn from overcollateralized loans to premium borrowers.

Maple’s Earn products delivered highly attractive yields over the past year. The XIRR (Extended Internal Rate of Return) rates below show roughly double-digit returns for syrupUSDC, excluding loyalty rewards that made lending even more profitable.

Strategic DeFi integrations have multiplied Maple’s reach across the ecosystem. The Pendle integration allows users to lock fixed yields or speculate on future reward values, while the Morpho collaboration enables syrupUSDC holders to earn on average 11-12% yields while borrowing USDC at 5-6% rates, creating sophisticated leveraged strategies previously nearly impossible in traditional markets. Maple’s Bitcoin yield products, launched in early 2025, have averaged 5.28% net APY since inception paid natively in BTC, which is extremely lucrative. This innovation has attracted significant institutional interest, particularly from family offices seeking yield-bearing Bitcoin exposure.

The protocol’s transition to fully overcollateralized lending has eliminated historical vulnerabilities, achieving zero defaults throughout 2024-2025 while consistently delivering institutional-grade yields that significantly exceed traditional finance benchmarks.

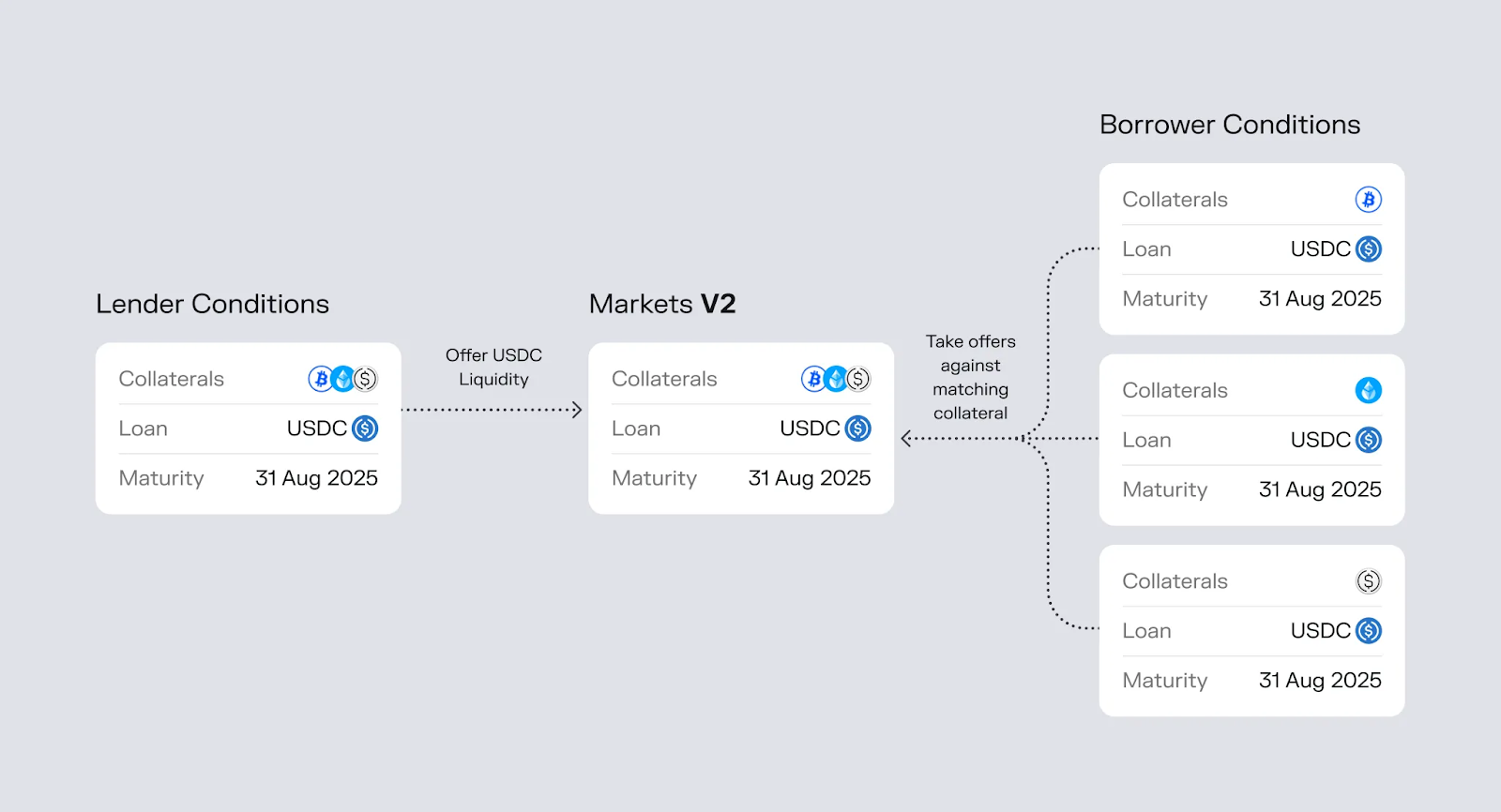

Morpho v2: When DeFi Learned to Speak Institutional

While traditional DeFi lending protocols forced institutions to accept rigid, one-size-fits-all terms, Morpho v2 flips this dynamic entirely with its revolutionary intent-based architecture that finally delivers what institutions have been waiting for—fixed-rate, fixed-term loans with fully customizable parameters.

Source: Morpho Labs

Think of it as the difference between shopping at a department store versus having a bespoke tailor: instead of accepting whatever rates and terms a liquidity pool dictates, lenders and borrowers can now express exactly what they want and watch the protocol work its magic to find the perfect match. The platform’s impressive 70% gas cost reduction and support for everything from single assets to entire portfolios as collateral (including those coveted real-world assets) means institutions can finally operate with the efficiency and sophistication they’re accustomed to in traditional finance. Perhaps most crucially, fixed-rate lending eliminates the interest rate roulette that kept institutional balance sheets on the sidelines, while customizable terms let them craft loan structures that actually make sense for their complex risk frameworks and regulatory requirements. Importantly, Morpho v2 doesn’t abandon the flexibility that made DeFi popular—users can still choose between the traditional variable-rate, open-term lending of v1 or embrace the new fixed-term predictability, giving everyone the best of both worlds.

The protocol’s compliance features cleverly integrate KYC and whitelisting without the usual DeFi headache of liquidity fragmentation—essentially having your regulatory cake and eating it too. When Coinbase decided to power their Bitcoin-backed loans through Morpho, processing over $400 million and serving millions of users, it sent a clear signal: this isn’t just another DeFi experiment, it’s enterprise-ready infrastructure. With an impressive security track record of 27 audits and formal verification, Morpho v2 has essentially built the bridge that institutions have been waiting for to cross into DeFi.

The platform’s $4.2 billion TVL as of June 2025 tells a story that reads like a case study in institutional appetite for sophisticated DeFi infrastructure that doesn’t compromise on predictability and control. In essence, the second iteration of the battle-proven Morpho protocol represents the moment when DeFi matured and learned to speak fluent institutional finance, creating a pathway for trillions of dollars to flow from traditional markets into decentralized ones.

Pendle Citadels targets trillion-dollar institutional yield markets

Pendle’s ambitious Citadels initiative, announced in January 2025, represents a strategic expansion beyond traditional DeFi to capture institutional fixed-yield demand across multiple sectors. The protocol plans three specialized Citadels: a Cross-Chain Citadel extending to Solana and Hyperliquid ecosystems, an Institutional Citadel offering KYC-compliant access to crypto-native fixed yields, and a Shariah-Compliant Citadel targeting the $3.9 trillion Islamic finance market.

Built on Pendle’s proven V2 AMM technology, which facilitated extraordinary growth from $230 million to $4.4 billion TVL throughout 2024—a 20x increase—the Citadels create regulated pathways for traditional finance entities to access premium DeFi yields. The protocol’s daily trading volume expanded from $1.1 million to $96.4 million, establishing Pendle as the 7th largest Ethereum protocol. Integration with Ethena’s Converge blockchain for institutional KYC capabilities and the new Boros perpetual yield product targeting $150 billion daily markets position Pendle to capture significant institutional flow in 2025.

Spark Protocol: Vertical Integration Across Finance

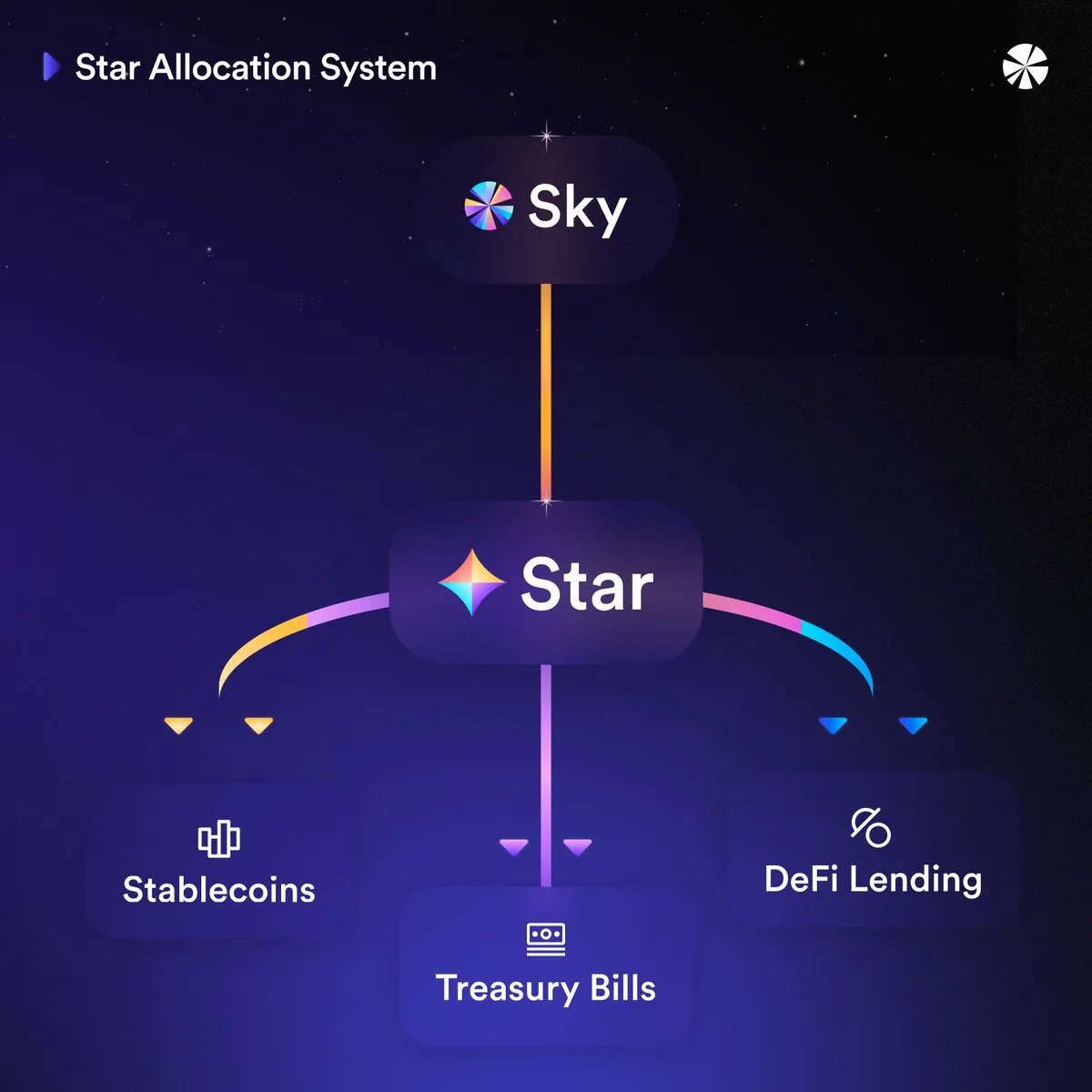

Spark Protocol operates as the most advanced onchain yield engine within the Sky ecosystem, functioning as Sky’s first “Star” – an autonomous capital allocation unit that sources low-cost liquidity from Sky (prev. MakerDAO) and deploys it strategically across both DeFi protocols and real-world assets. Through its Spark Liquidity Layer (SLL), the protocol manages over $3.5 billion in assets, automatically rebalancing capital across Morpho, Aave, Ethena, and tokenized Treasury products like BlackRock’s BUIDL fund. What sets Spark apart is its ability to offer fixed-rate borrowing through SparkLend, made possible by Sky’s governance-controlled Sky Savings Rate (SSR) that provides predictable borrowing costs independent of short-term liquidity fluctuations. This structural advantage allows users to borrow USDS at stable rates while using sUSDS as collateral, creating a self-reinforcing cycle where yield-bearing deposits expand lending capacity.

Spark’s institutional appeal stems from its balanced exposure to both DeFi-native revenues and traditional finance through strategic RWA allocations totaling over $1.5 billion – including $800 million in BlackRock’s BUIDL Fund, $400 million in Janus Henderson’s Anemoy Treasury Fund, and $300 million each across Superstate’s Short Duration US Government Securities Fund, Maple’s syrupUSDC, and Ethena’s sUSDe. The protocol further enhances yield through indirect exposure via Pendle’s PT-sUSDe positions, which provide fixed-yield collateral options while maintaining direct access to both Treasury-backed stability and DeFi’s higher-yield opportunities. Additionally, the $1 billion Tokenization Grand Prix initiative, which attracted proposals from 39 traditional finance firms including BlackRock and Janus Henderson, demonstrates its role as a bridge between institutional capital and DeFi infrastructure. Going forward, Spark plans to expand its cross-chain PSM infrastructure and deepen its RWA integration, positioning itself as the primary hub for institutional onchain capital allocation as traditional finance continues its tokenization journey.

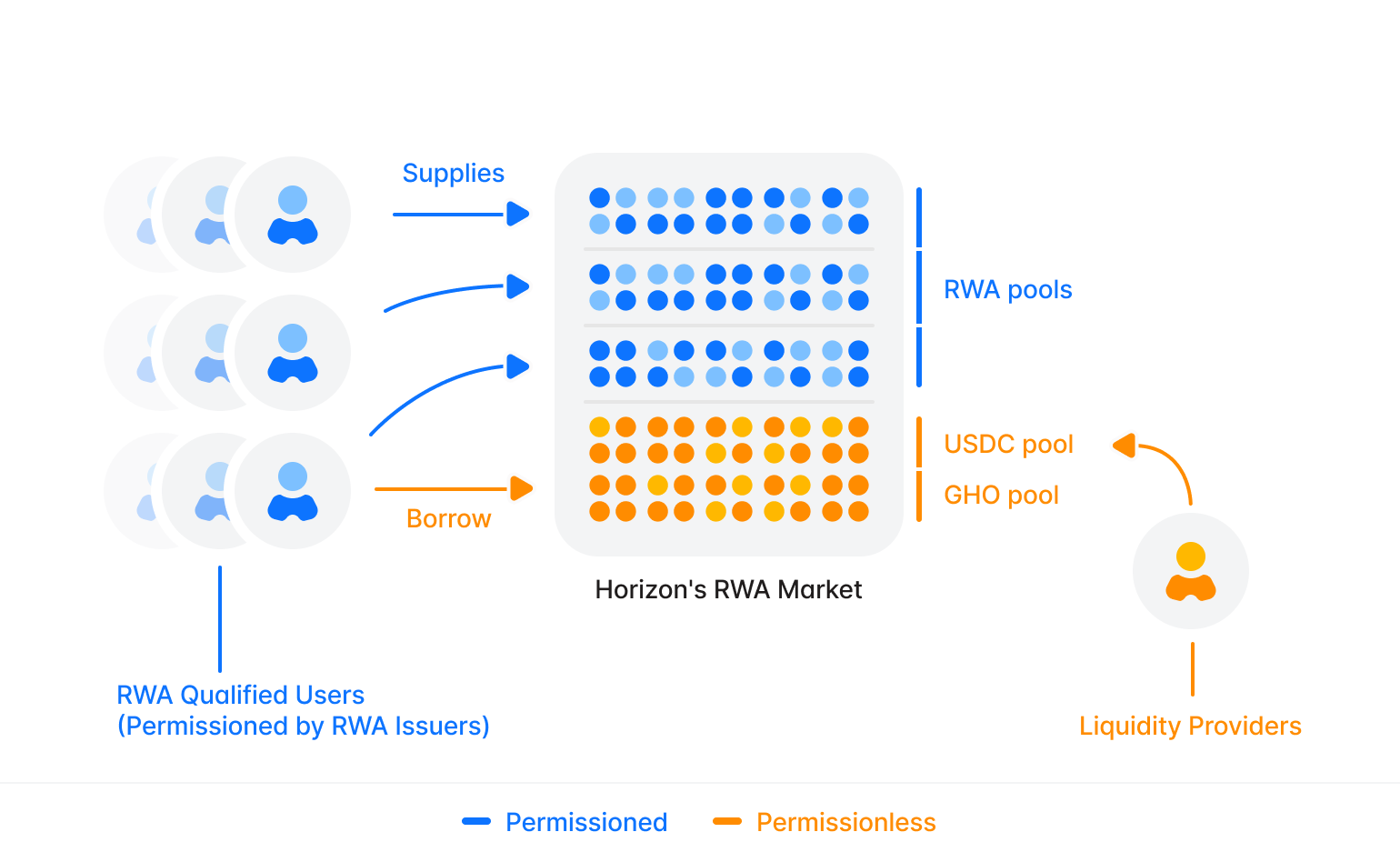

Horizon: AAVE’s Road to RWA DeFi

AAVE’s proposed Horizon protocol represents a bold strike for institutional DeFi lending, creating a hybrid model that combines permissionless liquidity with permissioned collateral.

Announced in March 2025 and currently undergoing DAO approval, Horizon would enable institutions to use tokenized money market funds as collateral for borrowing stablecoins like USDC and GHO.

Source: AAVE’s DAO

The protocol features a unique revenue-sharing structure that starts at 50% to AAVE DAO in Year 1, declining to 10% by Year 4, targeting the projected $16 trillion RWA tokenization market. Unlike AAVE Arc’s fully permissioned approach, Horizon maintains open liquidity pools while restricting collateral to approved RWA tokens, creating an optimal balance between institutional compliance requirements and DeFi composability. The protocol includes dedicated GHO facilitators for on-demand minting and asset-level permission management for RWA issuers, positioning it as a potential gateway for traditional finance institutions seeking structured DeFi exposure.

Institutionalized DeFi on Solana

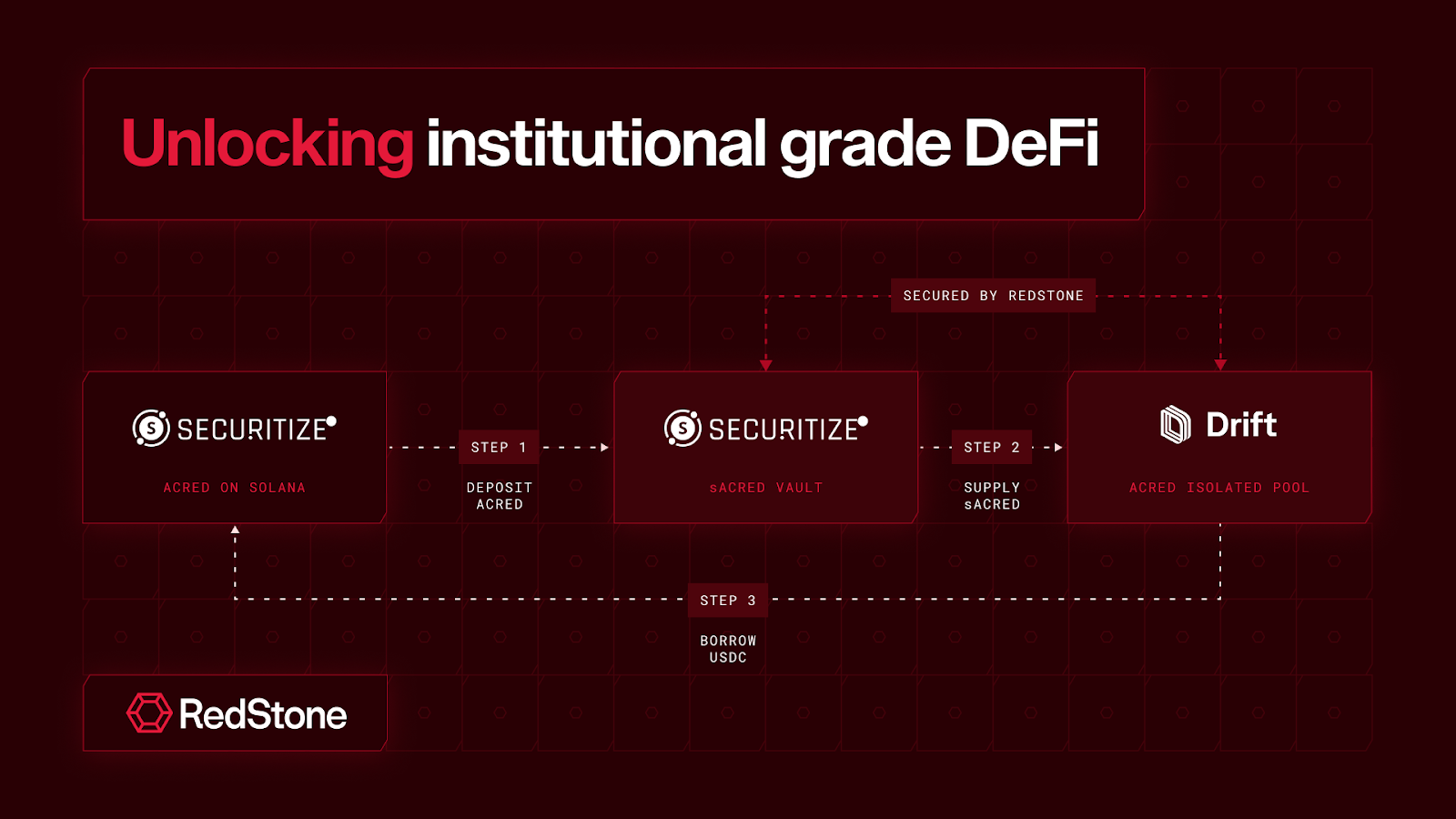

Drift has transformed into the premier institutional DeFi platform with its white-glove service named Drift Institutional, and pioneering the first-ever use of yield-bearing stablecoins as collateral for perpetual futures trading through partnerships with Ondo Finance’s USDY token and BlackRock’s BUIDL fund. These actions helped the platform achieve over $55 billion in cumulative trading volume while attracting major institutional capital, including Apollo Global Management’s $785 billion AUM tokenized credit fund ACRED.

Learn more about tokenized private credit growth in DeFi at the RedStone blog

Kamino Finance has emerged as another major contender, achieving over $2 billion TVL as of June 2025 through a comprehensive strategy that includes institutional-focused features such as enhanced KYC/AML frameworks, strategic partnerships with Steakhouse Financial for risk management, and formal verification through Certora. Both platforms now host Apollo’s ACRED token, bringing unprecedented institutional capital to the ecosystem.

Note: All quantitative data in this section is sourced from DeFiLlama or official project analytics and is accurate as of June 26, 2025

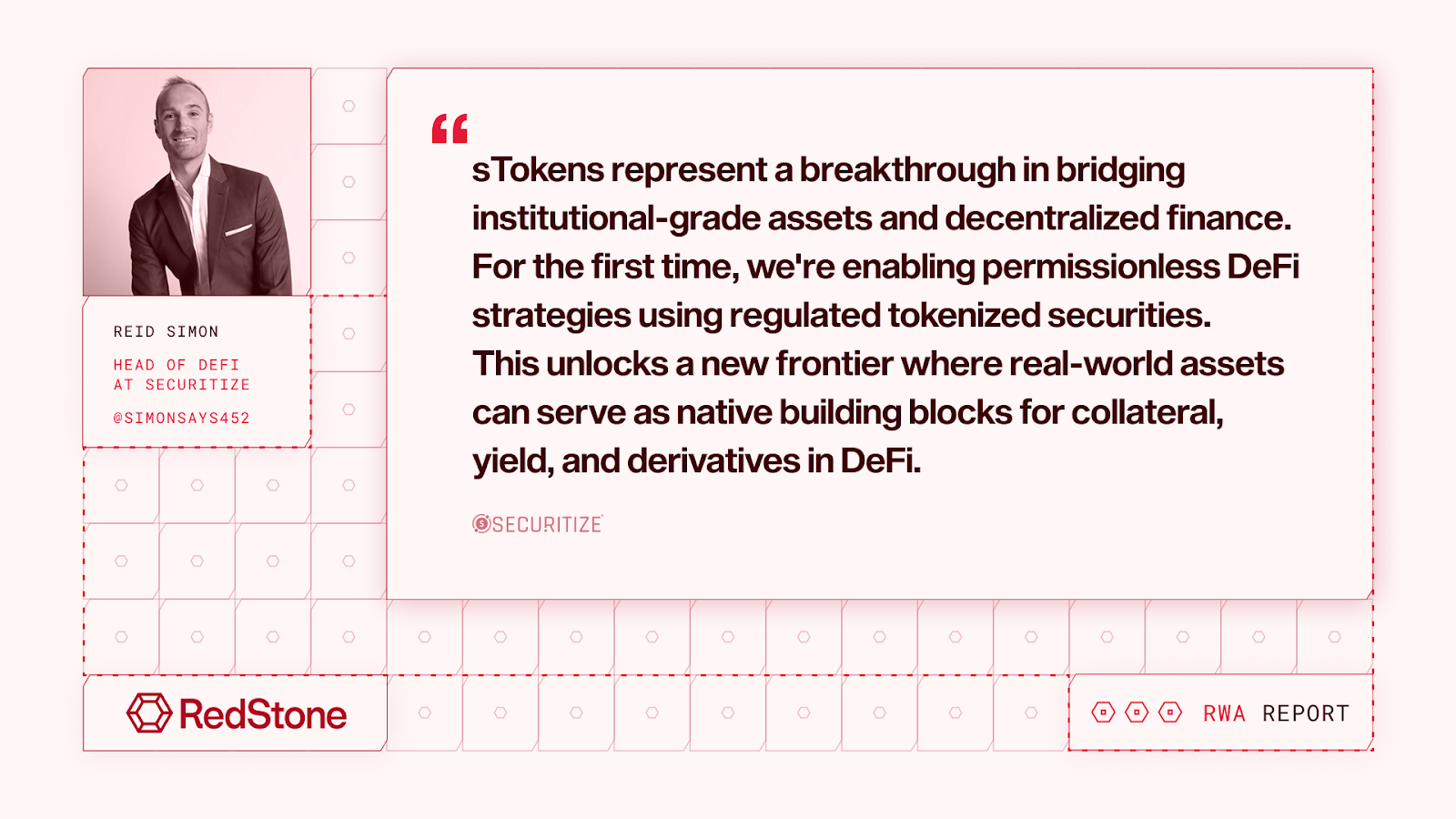

The sTokens Revolution: Enabling Tokenized Assets in DeFi

Securitize has emerged as the world’s largest tokenized asset issuer with over $4B (as of May 2025) in assets under management and roughly 30% of the tokenization market share, pioneering a revolutionary approach to bringing institutional-grade real-world assets (RWAs) into the DeFi ecosystem through their innovative sToken framework.

It’s important to note that Securitize’s native tokenized securities cannot be directly utilized within DeFi protocols due to their embedded regulatory restrictions – tokens must first be deposited into their proprietary sVault technology, which then mints DeFi-compatible versions that maintain a regulated framework while enabling broad onchain activity.

Beyond efficiency gains for tokenization clients, Securitize aims to unlock economic flexibility and potential higher returns via DeFi integration – key word being potential. To fulfill this goal, Securitize built the sToken framework that transforms tokenized securities into permissionless tokens, creating a net-new growth driver for decentralized finance by enabling traditional securities to function as composable DeFi primitives within a regulated framework.

sToken: What It Is & How It Works

The legal framework powering DeFi-compliant tokenization

Think of Securitize as the ultimate regulatory bridge between Wall Street and DeFi – they’ve built the most comprehensive legal framework in the tokenization industry by becoming an SEC-registered transfer agent, FINRA member broker-dealer, and operating their own Alternative Trading System. The magic happens through their Digital Securities (DS) Protocol, which acts like a regulatory computer built into every token, automatically checking investor credentials, enforcing geographic restrictions, and ensuring every trade follows securities law. This breakthrough allows traditional investment funds to operate as DeFi collateral while maintaining full regulatory adherence – something previously impossible in the crypto space.

Technical architecture enabling white-glove tokenized DeFi

The sToken framework is essentially a smart wrapper that transforms traditional investment funds into DeFi-compatible assets without losing their regulatory protections. Built on ERC-4626, these tokens automatically calibrate their backing to underlying assets – in some cases based on reported fund NAV (Net Asset Value) like Apollo’s ACRED – while functioning as standard DeFi tokens that can earn yield, serve as collateral, and interact with protocols across multiple chains. The technical breakthrough lies in embedding regulatory controls directly into smart contract code – transaction execution is enabled only for a whitelisted investor set, making institutional-grade assets accessible in DeFi for the first time.

Future Implementations and Use Cases

We’re still in the early testing phase of DeFi-compliant integrations, even as massive tradfi capital begins flooding these ecosystems. The first wave has already begun – we’ve seen pioneering RWA DeFi integrations like sACRED’s leverage strategy curated by Gauntlet and Steakhouse Financial and sBUIDL’s strategy by Re7 deployed across Morpho, Kamino, Drift Institutional and Euler markets.

But these are just the opening moves. As the infrastructure matures, we’re looking at exponentially more capital flowing into RWA DeFi positions, with strategies evolving far beyond simple secondary liquidity provision or leverage looping on underlying RWA assets. Picture using sBUIDL as collateral for derivative trading on Hyperliquid, or creating entirely new yield speculation markets through interest rate swaps on products like sACRED – one side locking in guaranteed returns, the other leveraging up on yield speculation.

The foundation is being laid for something much larger.

RedStone is excited to serve as Securitize’s primary blockchain oracle provider, supporting all current and future sToken use cases as we extend DeFi into the trillion-dollar tokenized assets industry. Read more about the partnership in the blogpost.

Leveraged RWA Positions in DeFi

Note: This section has been authored by Gauntlet, a leading provider of institutional-grade vault strategies and risk management solutions for decentralized finance.

Leveraged RWA strategies enable participants to amplify returns on tokenized assets by utilizing DeFi’s borrowing infrastructure, creating enhanced yields while navigating the complex operational constraints inherited from both TradFi and DeFi ecosystems. Operating at this intersection creates a multifaceted challenge matrix spanning composability, cost structures, and market infrastructure limitations. The following insights from Gauntlet explore these implementation challenges, breakthrough solutions, and the future of sophisticated RWA strategies in decentralized finance.

Bringing RWAs to DeFi: Technical and Structural Challenges

DeFi-Inherited Constraints

- Variable Cost of Capital: The dynamic cost of capital environment in DeFi may create unpredictability. Borrowers utilizing RWA strategies face fluctuating borrowing costs based on real-time market conditions and liquidity availability, contrasting with fixed-rate structures common in traditional finance.

- Portfolio Integration Challenges: As novel onchain assets, RWAs have not yet established clear positioning within crypto-native investment portfolios. Despite offering non-correlated returns that could serve as effective hedges against crypto market volatility, adoption remains limited due to unfamiliarity and integration complexity.

- Price Discovery Limitations: Single-source pricing can create risks around pricing accuracy and timing. DeFi markets typically rely on multiple blockchain oracle sources and real-time price feeds. Still, many RWAs depend on periodic valuations from single sources, creating trust and accuracy concerns that further limit liquidity provision.

TradFi-Inherited Constraints

- Onboarding and Compliance: KYC requirements and onboarding processes can reduce the potential user base and limit liquidity provisioning for RWAs. These processes often require extensive documentation and verification periods that may be unfamiliar to DeFi-native users.

- Redemption Timeline Asymmetries: Extended redemption timelines for certain RWAs may create fundamental liquidity mismatches. Where DeFi users are used to immediate settlement, RWAs may require weeks or months for redemption processing.

- Education: While TradFi institutions and investors are increasingly exploring opportunities in DeFi, there remains a knowledge gap in how DeFi operationally fits into the TradFi ecosystem. The complexity of DeFi systems often means TradFi institutions and investors need to examine unfamiliar market structures and underlying mechanisms. This also applies vice versa, as DeFi-native users may be less familiar with TradFi products that can have DeFi implementations (e.g. private credit).

Breakthrough Solutions and Market Infrastructure

- Enhanced Market Design: Developing robust markets specifically designed for assets with asymmetric redemption profiles represents a critical infrastructure advancement. Fixed-rate lending protocols and specialized borrowing mechanisms can address the fundamental mismatch between DeFi’s immediate liquidity expectations and RWA redemption timelines.

- Multi-Source Price Discovery Systems: Establishing reliable, multi-oracle pricing systems that meet DeFi standards for accuracy and frequency while accommodating RWA valuation methodologies. This infrastructure development is essential for building trust and enabling deeper liquidity provision.

- Partial Composability Solutions: Creating systems that enable limited composability while respecting transfer restrictions and compliance requirements allows RWAs to participate in DeFi ecosystems without compromising regulatory frameworks.

Gauntlet’s Strategic Approach to RWA Growth

RWAs represent an important component of the company’s broader strategy to serve diverse users while leveraging our core vault curation and risk management expertise across DeFi and TradFi.

- Cross-Asset Yield Amplification: Gauntlet’s approach leverages the symbiotic relationship between levered RWA strategies and existing vault infrastructure. RWA borrowing increases demand across markets where Gauntlet’s vaults allocate capital, creating positive feedback loops that enhance yields for all participants while expanding strategy utility.

- Portfolio Diversification: RWAs offer compelling diversification benefits to crypto-native portfolios through access to non-correlated assets that maintain consistent yields even in the case of significant amounts of capital inflows. For institutional and sophisticated retail participants, RWAs expand the available opportunity set by providing access to previously unavailable asset classes through tokenization.

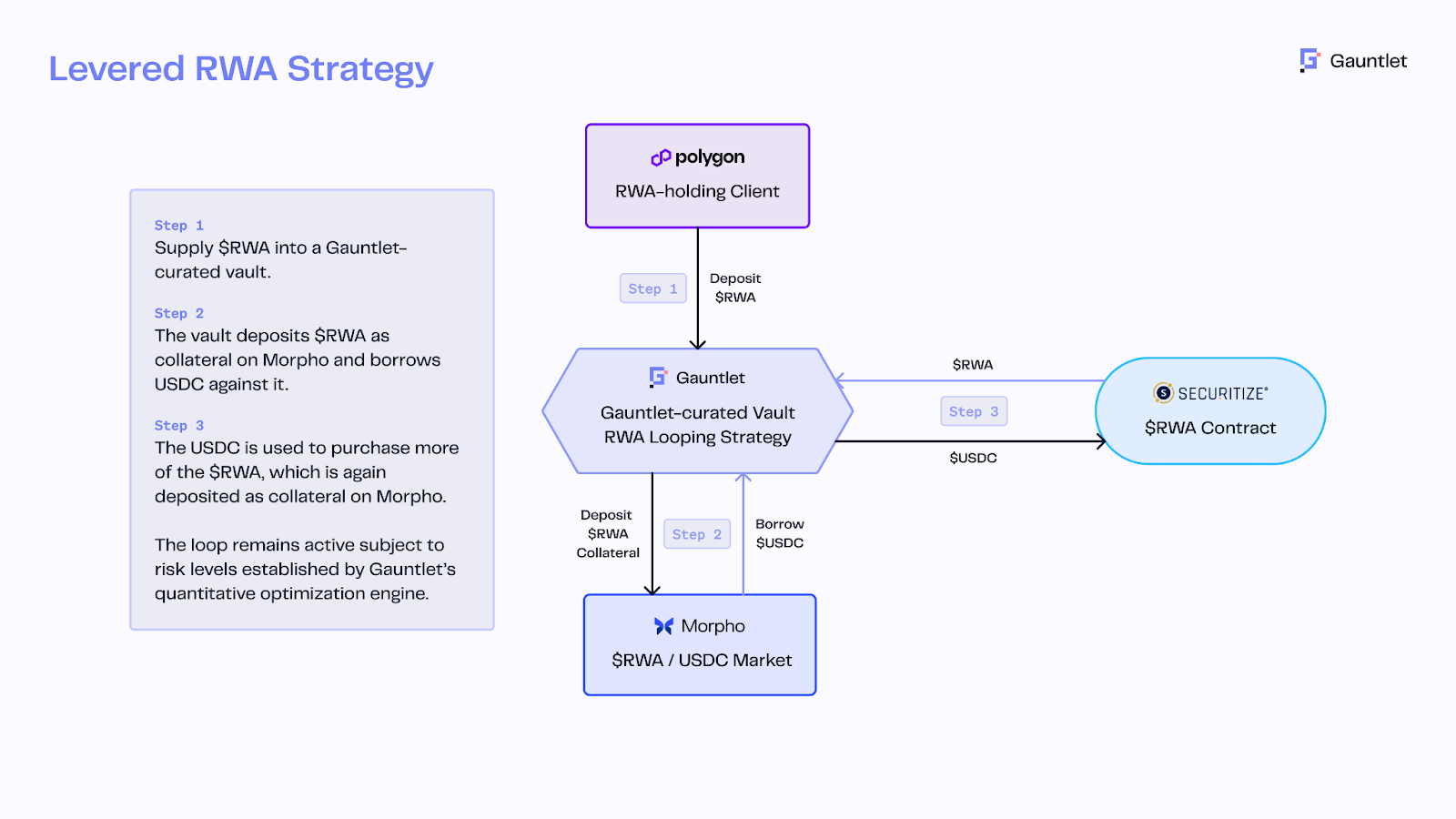

Proven Implementation: Apollo ACRED Strategy

Gauntlet’s leveraged RWA strategy utilizing Securitize’s sACRED—a tokenized fund providing access to Apollo’s diversified credit fund—demonstrates the significant potential of bringing DeFi rates to traditional finance structures. This implementation serves as both proof of concept and foundation for broader RWA strategy exploration, showing how sophisticated leverage strategies can enhance returns on traditional credit assets while maintaining appropriate risk management.

Source: Gauntlet

Future Expansion Plans

Beyond current implementations, Gauntlet plans to develop more sophisticated collateral and asset configurations. The levered strategy framework can expand to include additional stablecoins beyond USDC and incorporate a broader range of blue-chip RWAs, scaling the approach across multiple asset classes

Evolving Complexity: Next-Generation RWA Strategies

As RWA markets mature, industry participants are developing plans for more sophisticated strategy architectures. These approaches target structural limitations through innovative instrument design and enhanced operational frameworks.

- Interest Rate Derivatives and Yield Component Trading: The emergence of sophisticated RWA strategies leveraging DeFi primitives addresses inherent liquidity constraints through innovative approaches. Interest rate derivatives markets for RWAs—essentially “Pendle for RWAs”—would enable participants to trade yield components of fixed-rate tokenized assets, providing hedging mechanisms and additional liquidity venues.

- Multi-Collateral and Blended Strategies: Combining RWA exposure with liquid DeFi assets optimizes yield while maintaining operational flexibility. These approaches address RWA illiquidity by maintaining portfolio portions in liquid assets that provide exit liquidity and rebalancing capabilities, creating more robust and flexible investment structures. Gauntlet’s risk optimization engine handles unique challenges in complex RWA strategies, including liquidity risk modeling, real-time monitoring, and parameter optimization. This infrastructure enables sophisticated risk management across hybrid TradFi-DeFi strategies.

Market Growth Outlook

Strong growth in RWAs is anticipated, driven by increasing institutional adoption of tokenized assets, improving regulatory clarity around digital asset frameworks, and continued infrastructure development addressing current market limitations. The convergence creates new opportunities for sophisticated yield generation while requiring advanced risk management approaches.

Blockchain Oracles in RWA: The Enablers of onchain Markets

But let’s take two steps back and first establish what blockchain oracles are. At their core, blockchain oracles are services that feed external data into blockchain networks, acting as trusted intermediaries that translate arbitrary information into formats that smart contracts can understand and act upon. In traditional DeFi, oracles primarily aggregate price data from multiple cantralized and decentralized exchanges, i.e. Coinbase, Binance, Uniswap, to provide accurate, real-time valuations for crypto assets—enabling everything in DeFi from lending protocols to automated trading strategies. One could say that besides traditional DEXes, DeFi couldn’t exist without blockchain oracles.

Oracle services specializing in pricing Real-World Assets represent the foundational infrastructure that enables blockchain protocols to interact with traditional finance, serving as the critical bridge between off-chain asset valuations and onchain security mechanisms. Unlike DeFi’s continuous price feeds that theoretically could be updated every block, RWA oracles operate on fundamentally different temporal and trust assumptions, creating cascading effects on how liquidations must be structured and executed.

To illustrate these complex dynamics, we’ll examine Securitize’s sACRED token—derived from Apollo’s $1.3 billion Diversified Credit Fund—as it exemplifies the sophisticated oracle architecture and unique challenges that define RWA pricing systems across the industry.

RWA Oracle Dilemma: Beyond Real-Time Pricing

The fundamental oracle architecture reveals the complexity of pricing illiquid, real-world assets onchain. While traditional DeFi relies on push model oracle data feeds that aggregate prices from multiple sources at predefined intervals, RWA systems like sACRED typically depend on Net Asset Value (NAV) oracles that update daily with cross-check validation from a single source of truth. Most of the Securitize’s sTokens have these NAV feeds integrated directly into smart contracts, but the pricing methodology differs dramatically—rather than spot market prices, sACRED’s oracle reflects the underlying portfolio’s book value, accrued interest, and credit adjustments calculated by Apollo’s fund administrators.

RWA Oracles vs. Traditional DeFi: A New Pricing Paradigm

It’s quite remarkable how quickly we’ve begun referring to “traditional DeFi” and AAVE’s or Compound’s or Morpho’s liquidations as the “normal liquidation model”—DeFi has become so commonplace that we now take its distinctive approach as the status quo, when in reality it represents a radical departure from centuries of financial infrastructure.

The technical mechanisms reveal stark contrasts with what we now consider standard DeFi oracle infrastructure. Where oracles for protocols like Morpho or Compound aggregate multiple price sources with continuous updates, sACRED’s oracle system relies on a single authoritative source—Apollo’s fund administrator—creating both operational simplicity but introducing a potential single point of failure. Additionally, the oracle data’s end-game might involve qualitatively different pricing mechanisms: instead of market-determined prices reflecting real-time trading activity, RWA systems might incorporate trailing averages, credit assessments, and illiquidity discounts that smooth volatility but sacrifice immediate responsiveness to market changes. This potential evolution becomes apparent when sACRED updates daily with new NAV calculations, meaning it cannot capture intraday credit events or sudden market dislocations that would immediately trigger liquidations in standard DeFi protocols—highlighting how RWA integration might fundamentally reshape DeFi’s risk management paradigms rather than simply adapting to existing ones.

This fundamental shift in trust models represents perhaps the most significant departure from traditional DeFi oracle price feeds. sACRED’s pricing relies on Apollo’s internal valuations, audited financial statements, and regulatory oversight rather than market trading activity—creating stability against oracle manipulation attacks while introducing issuer-specific risks absent in market-based pricing. The validation mechanisms reflect this hybrid nature: while DeFi oracles employ multiple data sources and automated circuit breakers, RWA oracles depend on traditional audit trails, regulatory filings, and legal frameworks for accuracy verification, effectively bridging two entirely different approaches to financial truth.

Liquidation Implications and Risk Cascades

The oracle architecture directly shapes liquidation mechanics and risk propagation. The daily NAV updates for some tokenized assets mean liquidation triggers operate on, i.e. T+1, if not longer, timing rather than real-time, preventing the immediate cascade effects that can devastate DeFi protocols during market stress but also delaying necessary risk management actions. Then, the common quarterly redemption structure, informed by these same NAV oracles, creates liquidity constraints that wouldn’t exist with continuous market pricing. When Goldfinch experienced defaults like the $20 million Stratos Credit Fund issue, the oracle infrastructure couldn’t immediately reflect the credit deterioration, requiring human intervention and off-chain asset recovery processes—highlighting how RWA oracle limitations extend beyond pricing into operational complexity. This fundamental tension between blockchain’s desire for automation and real-world assets’ inherent complexity continues to shape how oracle infrastructure evolves, balancing accuracy, timeliness, and decentralization in ways that purely digital assets have never required.

What Will Be the RWA Oracle End-Game?

As the integration of Real-World Assets into DeFi accelerates, reliable pricing mechanisms emerge. Constructing these mechanisms is perhaps an even greater challenge than building oracle infrastructure for high-speed blockchains like MegaETH with millisecond block times. The complexity lies not in speed but in robustness and accuracy—how do you price illiquid private credit funds or real estate assets that don’t trade on open markets? RedStone currently leads the market with the most innovative yet reliable solutions for RWA oracle pricing, but what’s publicly available represents just the tip of the iceberg compared to what’s currently in development.

Oracle innovation over the past few years has been defined by pricing increasingly exotic assets where simple market quotes prove inadequate—Bitcoin LSTs Proof-of-Reserve verification, fundamental data oracles, and hybrid models applied to quoting the assets. RWA oracles represent the next frontier of this innovation, requiring entirely new methodologies that blend traditional financial analysis with blockchain-native verification. RedStone is working extensively behind the scenes to establish what could become the true market standard for tokenized asset pricing, fundamentally reshaping how we view oracle infrastructure in an increasingly tokenized world. The challenge isn’t just technical—it’s about creating pricing mechanisms that satisfy both DeFi’s need for transparency and traditional finance’s standard requirements.

Talking about the future of RWA oracles, we have to understand that a single source of truth creates a fundamental problem – a single point of failure. Therefore, the question is: how can we verify the authority? One solution would be to orchestrate independent nodes querying the same endpoints, then reaching consensus. That’s how many RWA oracle solutions strive to operate. But tomorrow, zero-knowledge “magic” along with web proofs can bring mathematically secured solutions. The blockers for now are the costs and time required for such technologies to operate at satisfactory scale, plus the inherent limitations of web proof technologies due to the architecture of the underlying TLS protocol that runs the Internet.

However, RedStone continuously conducts research on these verticals to satisfy the evolving needs of RWA and onchain finance convergence. Thankfully, there is an available and improved solution. A new standard will be soon revealed by RedStone in cooperation with one of the leading RWA partners, so stay tuned and follow RedStone’s announcements.

5. Comparative Analysis of Public RWA Chains

RWA Adoption Across Blockchain Networks

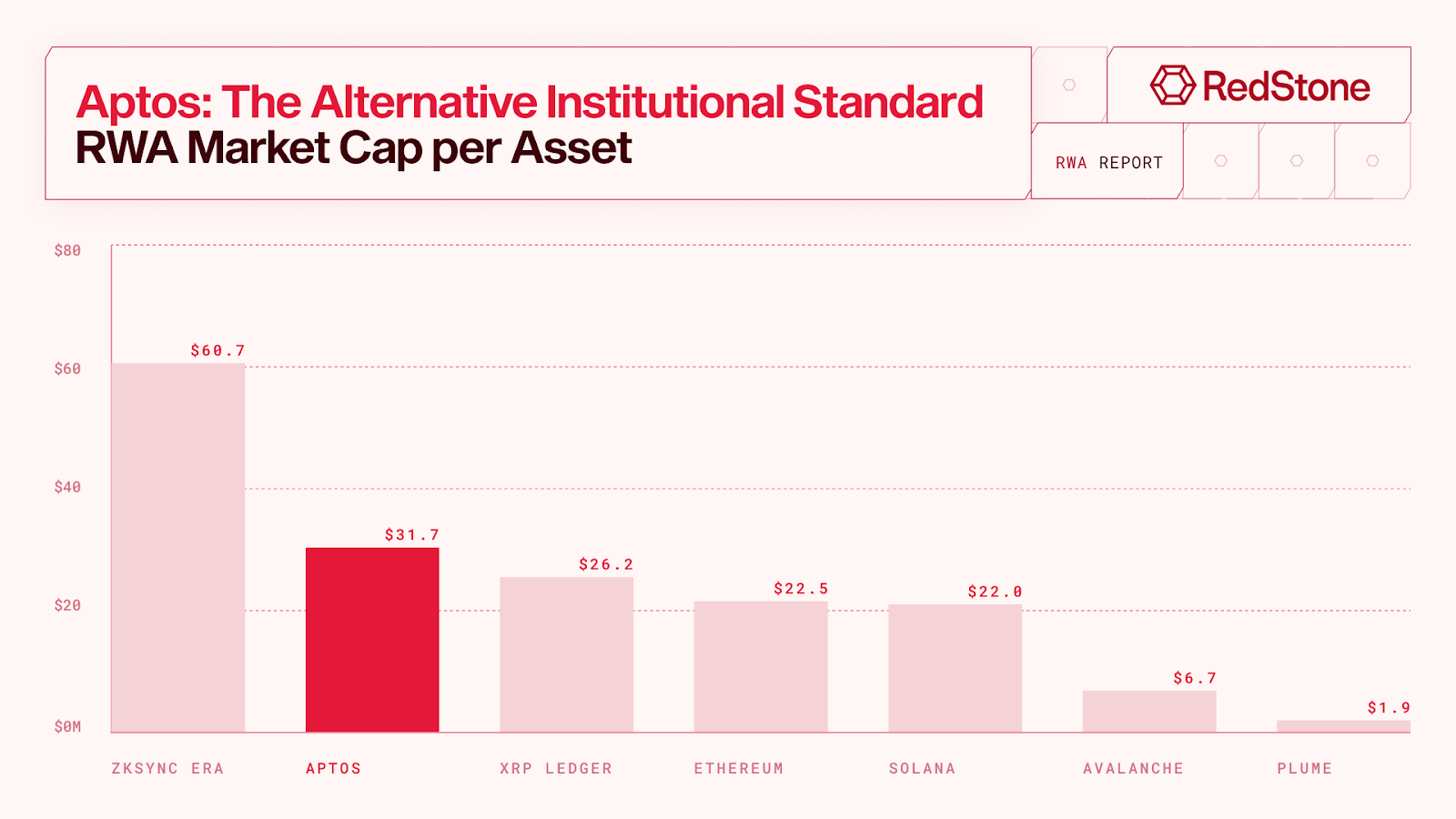

(Data as of 6/17/25) | RWA | ||

| Networks | Market Cap(Market Share %) | No. of Assets(% of Total) | Holders(% of Total) |

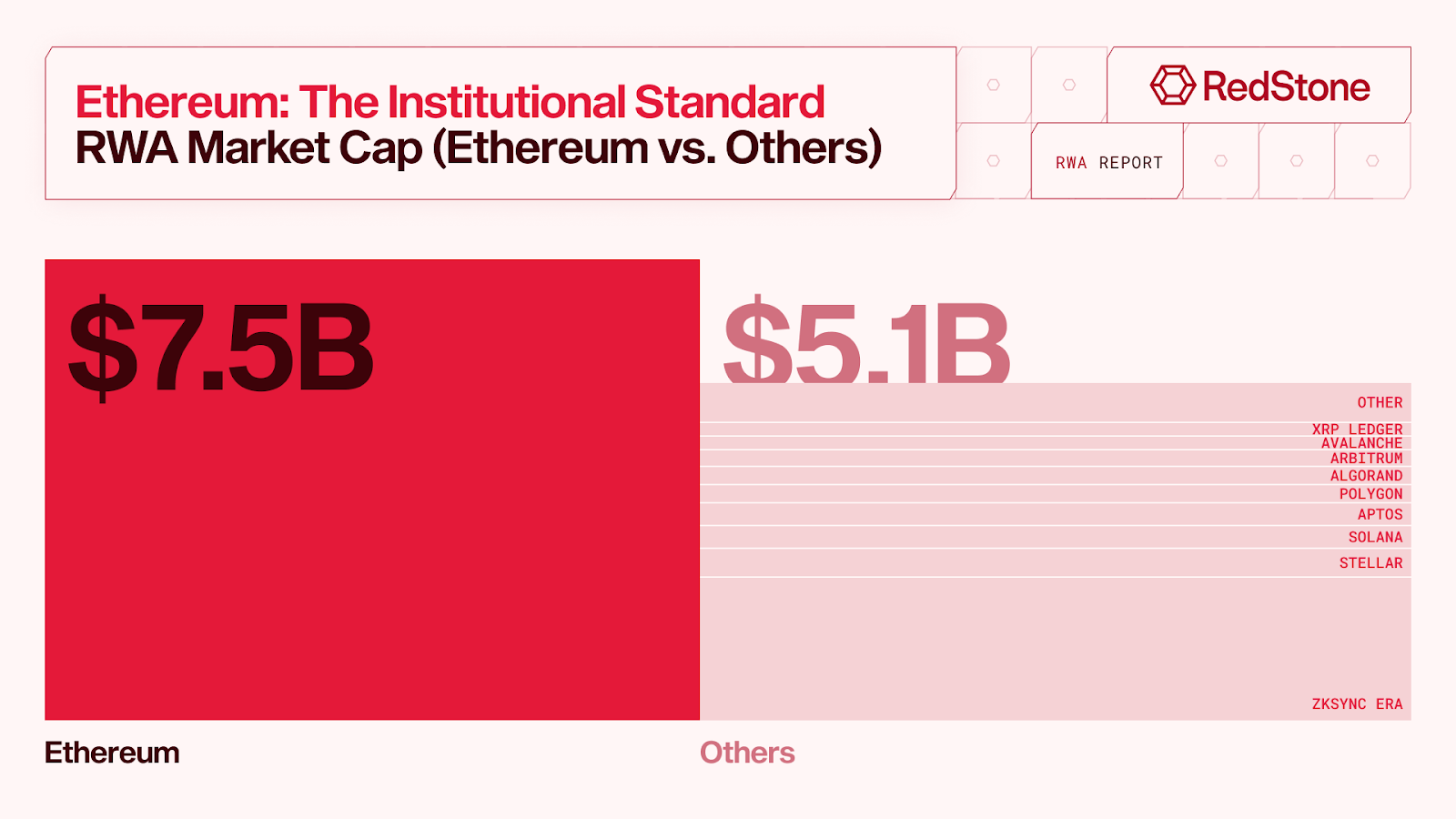

Ethereum | $7.5B (59%) | 335 (32%) | 76,780 (38%) |

ZKsync Era | $2.2B (18%) | 37 (4%) | 67 (0%) |

Solana | $351M (3%) | 16 (2%) | 7,250 (4%) |

Aptos | $349M (3%) | 11 (1%) | 2,433 (1%) |

Avalanche | $188M (1%) | 28 (3%) | 7,622 (4%) |

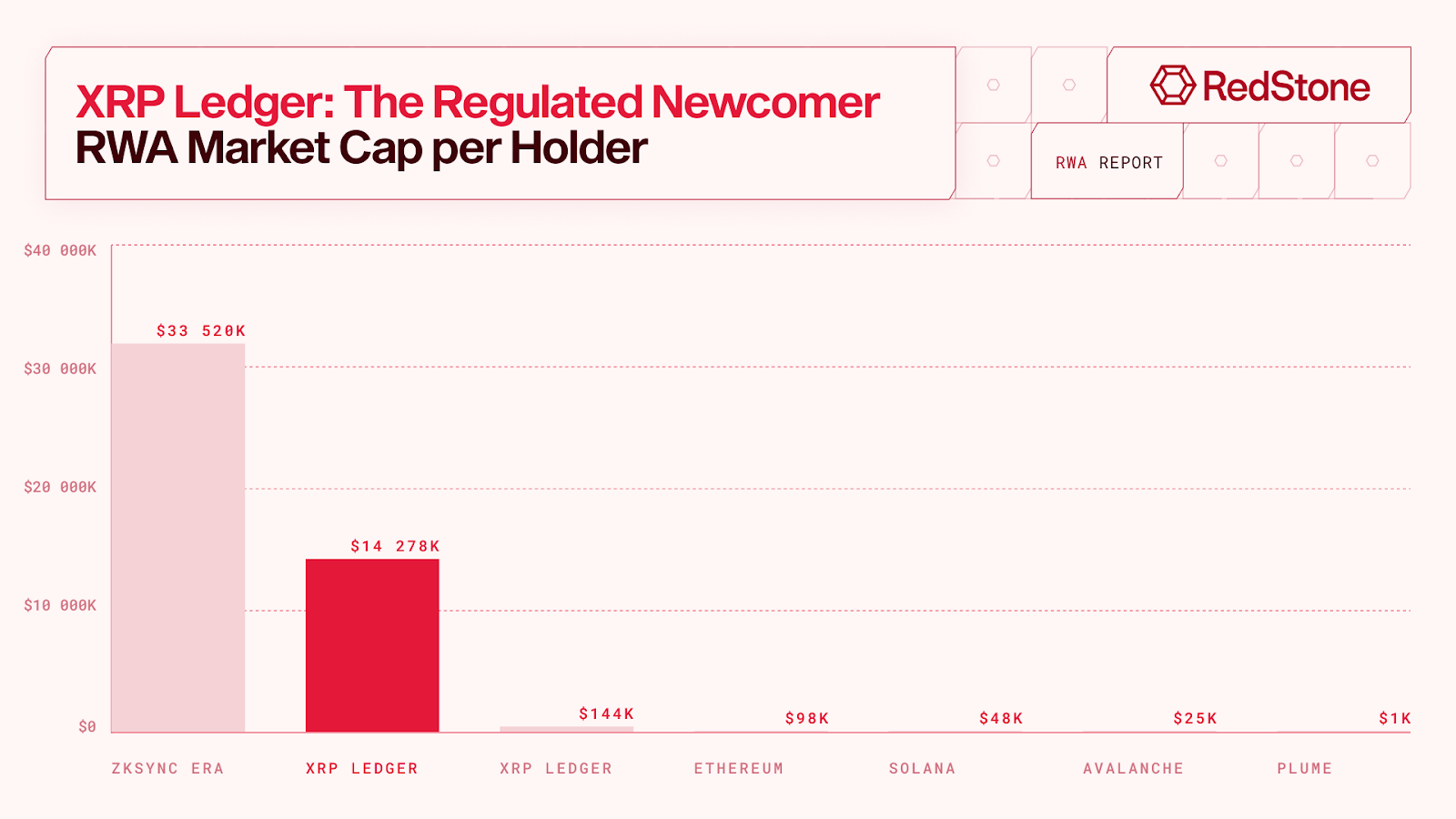

XRP Ledger | $157M (1%) | 6 (1%) | 11 (0%) |

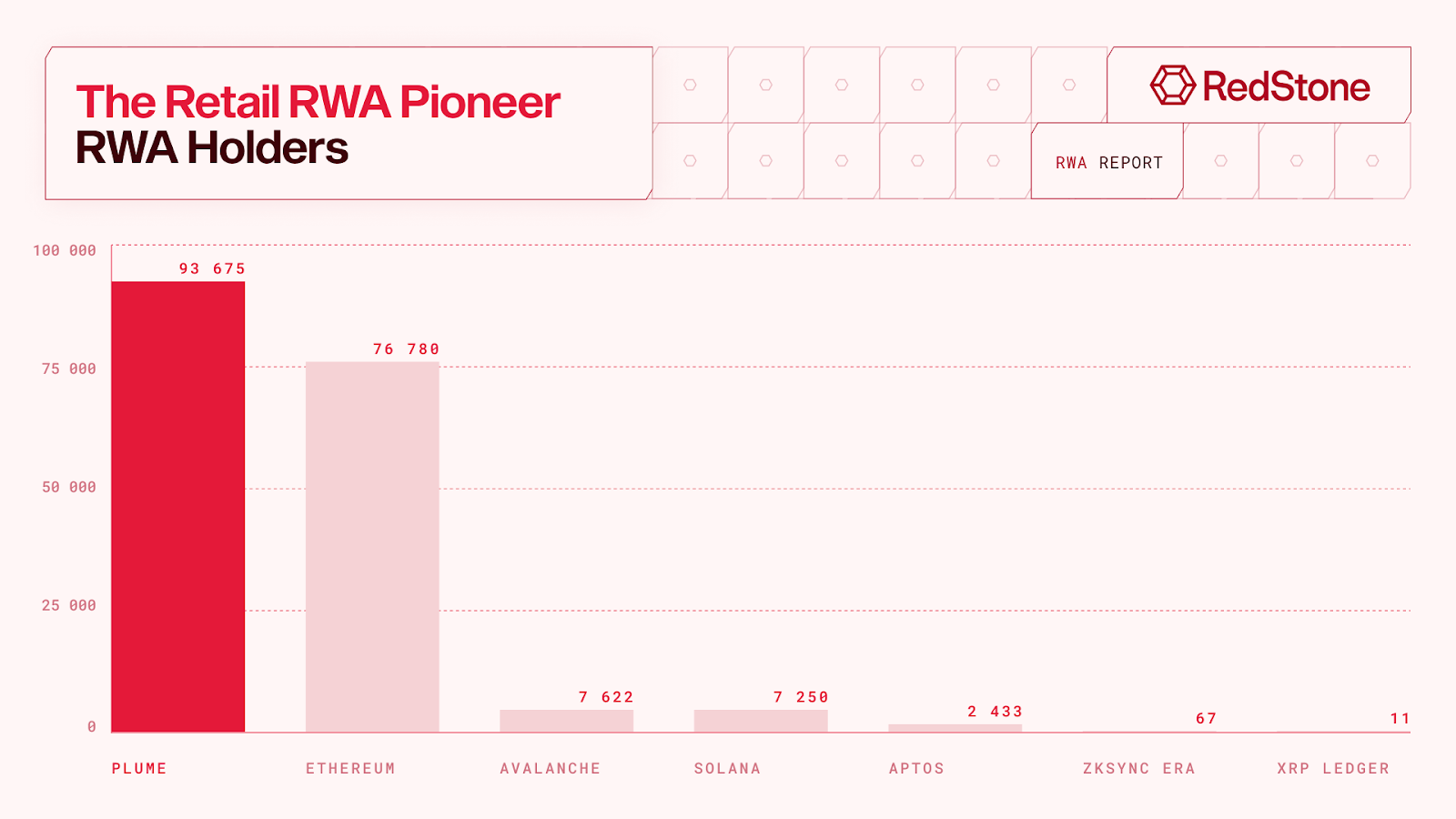

Plume | $84M (1%) | 45 (4%) | 93,675 (47%) |

Source: RWA.xyz

Note: This analysis is brought by RWA.xyz and focuses on blockchain networks where we have the deepest integrations and most reliable data insights. As the tokenized asset industry continues to grow, RWA.xyz aims to provide the broadest integrations and most comprehensive insights

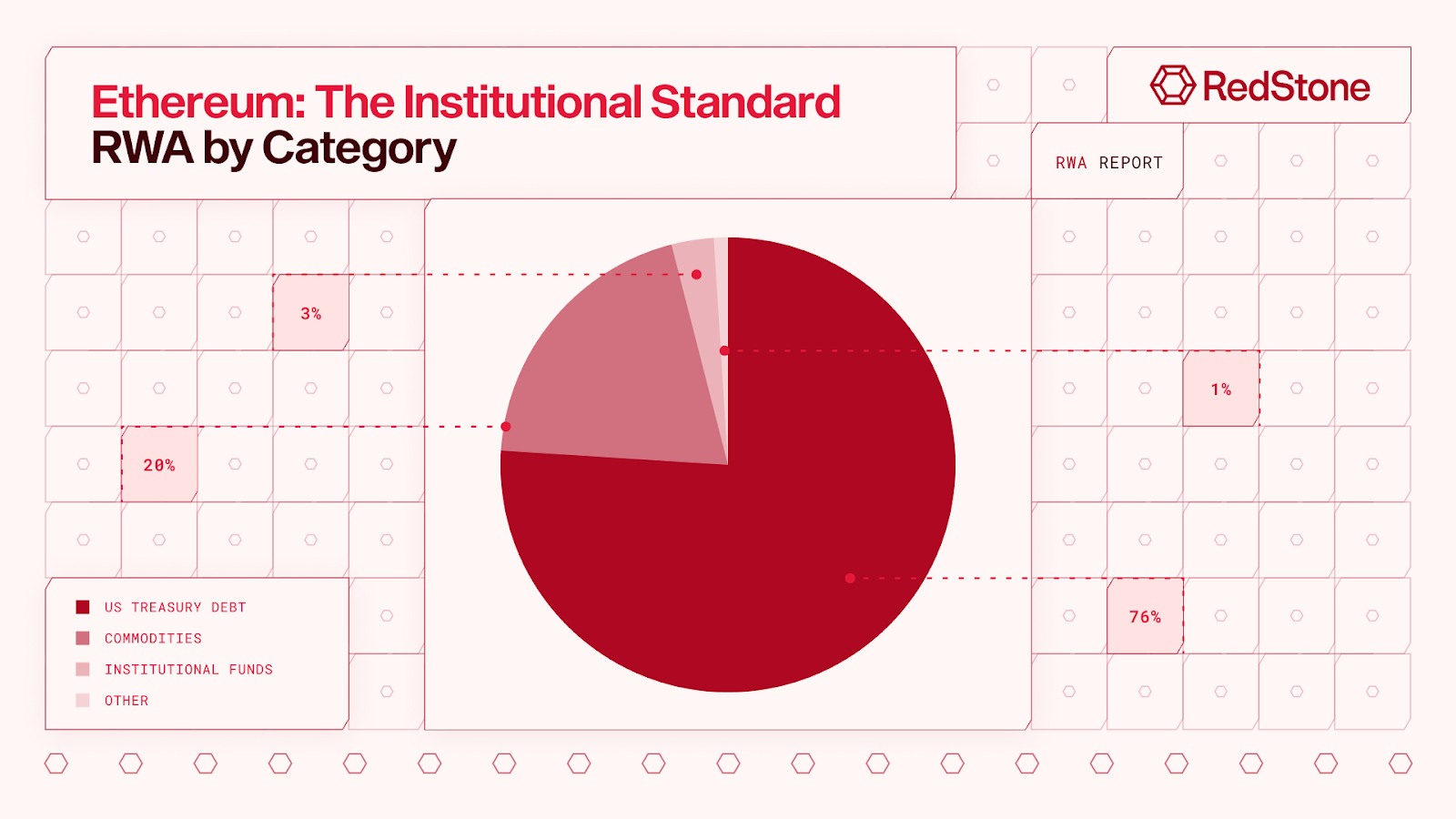

Ethereum: The Institutional Standard

Source: RWA.xyz

Ethereum remains the dominant platform for RWAs, hosting approximately $7.5 billion in tokenized value (59% of the market) across 335 distinct products. Major institutions consistently choose Ethereum for its broad network of users, developers, and DeFi protocols, as seen with BlackRock’s $2.7 billion BUIDL fund, the largest tokenized U.S. Treasury product to date. This trust is anchored in Ethereum’s decade-long security track record and deep liquidity, including $131 billion in stablecoins.

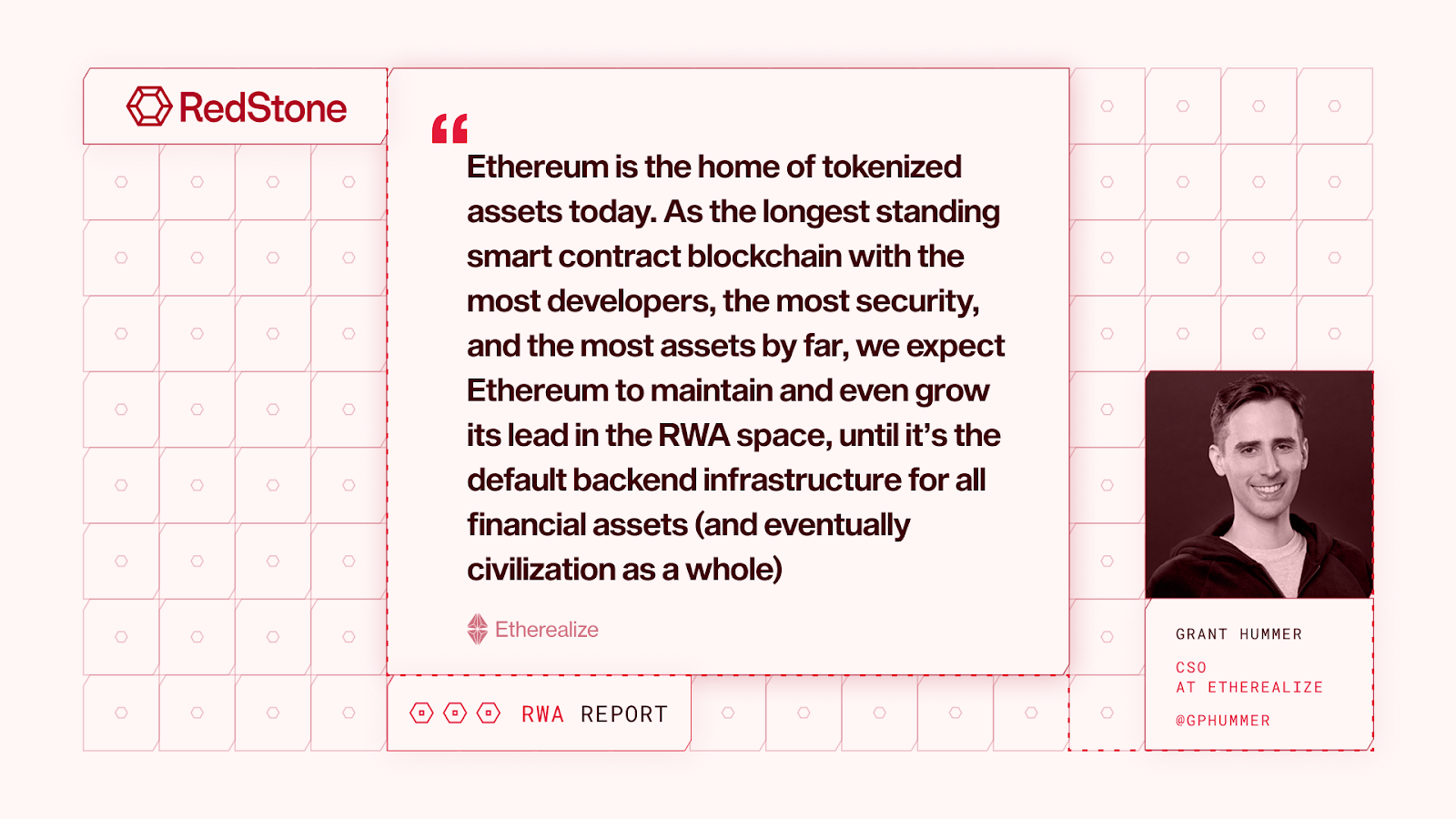

While Ethereum’s decentralized governance has historically limited its institutional outreach, the launch of Etherealize in January 2025 marked a strategic pivot. Led by former Wall Street banker Vivek Raman and Ethereum Foundation veteran Danny Ryan, Etherealize aims to position Ethereum as the “digital oil” of a tokenized financial system. Scalability and transaction costs remain hurdles, but Ethereum’s network effects and institutional credibility create a durable moat as tokenized assets accelerate into the mainstream.

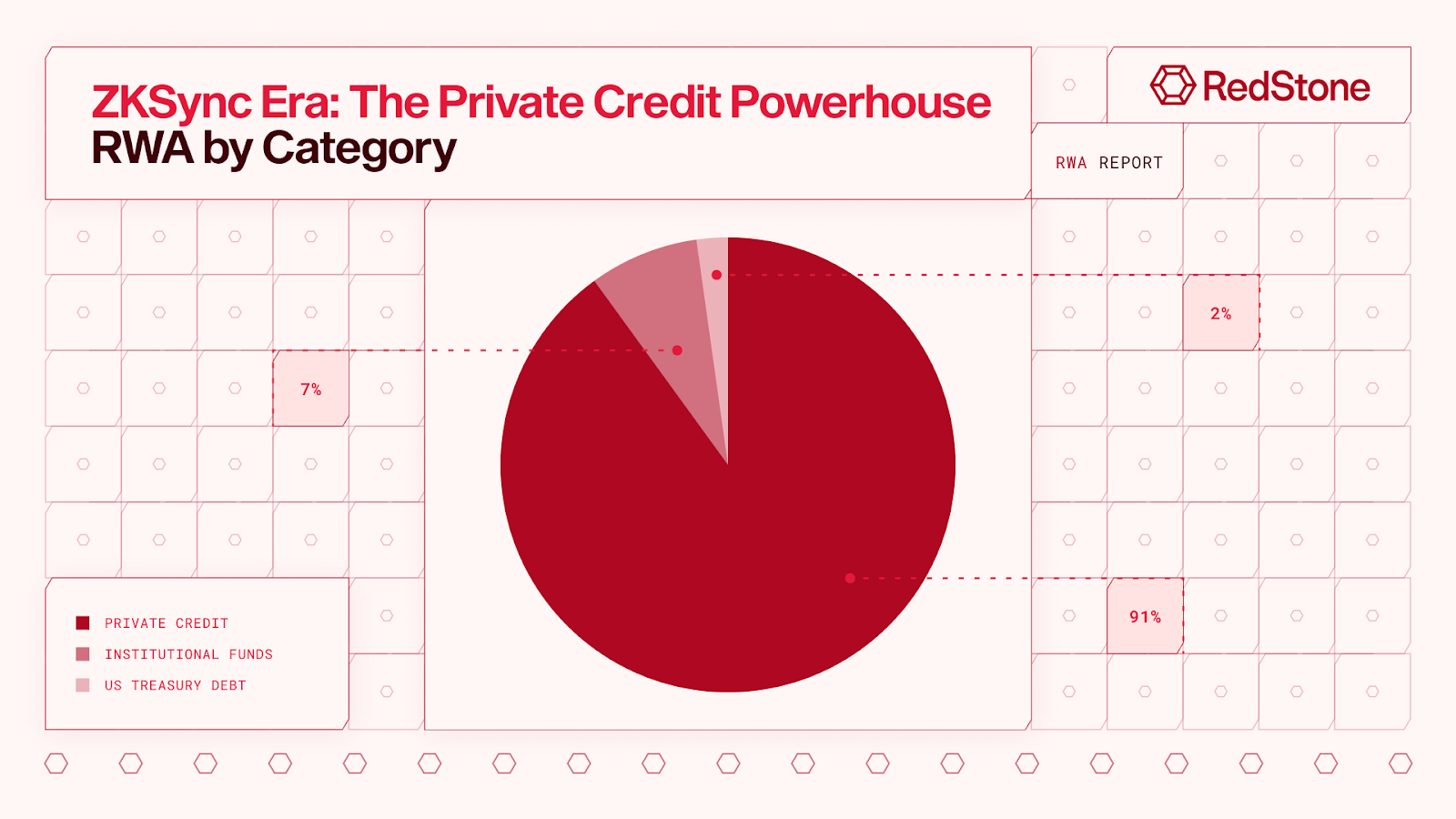

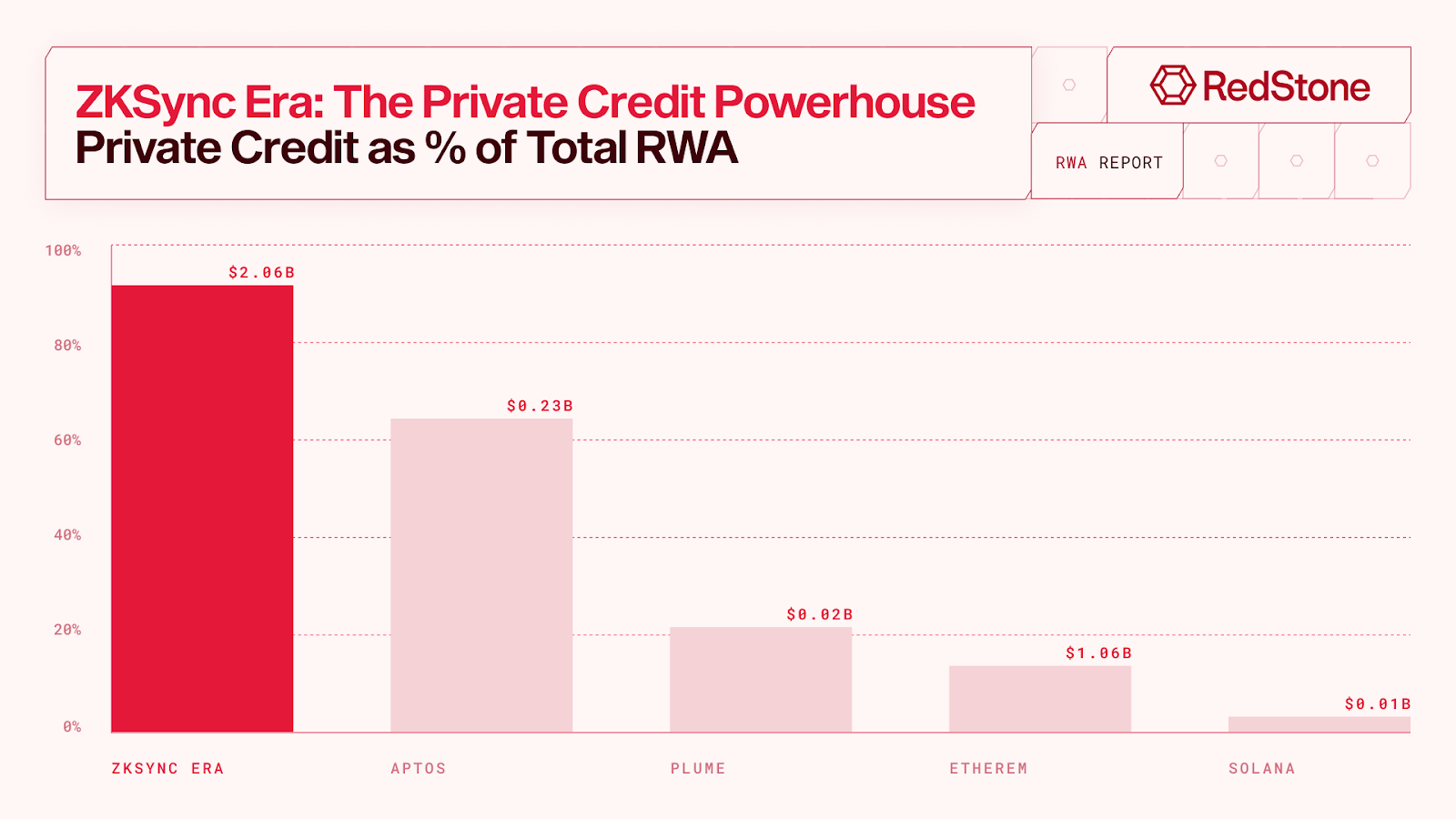

ZKSync Era: The Private Credit Powerhouse

Source: RWA.xyz

ZKsync Era, an Ethereum Layer-2 network built on zero-knowledge proofs, has rapidly become the second-largest platform for tokenized real-world assets, hosting $2.2 billion in value (18% of the market). This growth is driven almost entirely by Victory Park Capital’s $2.1 billion in tokenized private credit issued through the Tradable platform. ZKsync’s architecture offers a privacy-first approach to onchain assets, meeting critical institutional demands for confidentiality and compliance. Its RWA footprint includes 35 institutional-grade products across fintech loans, legal receivables, and structured credit, reflected in a concentrated structure with fewer but significantly larger offerings, averaging $61 million per asset. This profile suggests that large custodians and institutional players dominate usage, rather than a distributed retail base.

The launch of ZKsync Prividium in May 2025 further underscores the network’s institutional orientation, enabling financial institutions to run permissioned, privacy-preserving ledgers with native Ethereum interoperability. As confidentiality becomes a priority for tokenization at scale, ZKsync’s technical lead in zero-knowledge infrastructure puts it in a strong position to grow, especially if it can broaden its issuer base beyond early anchors like Tradable.

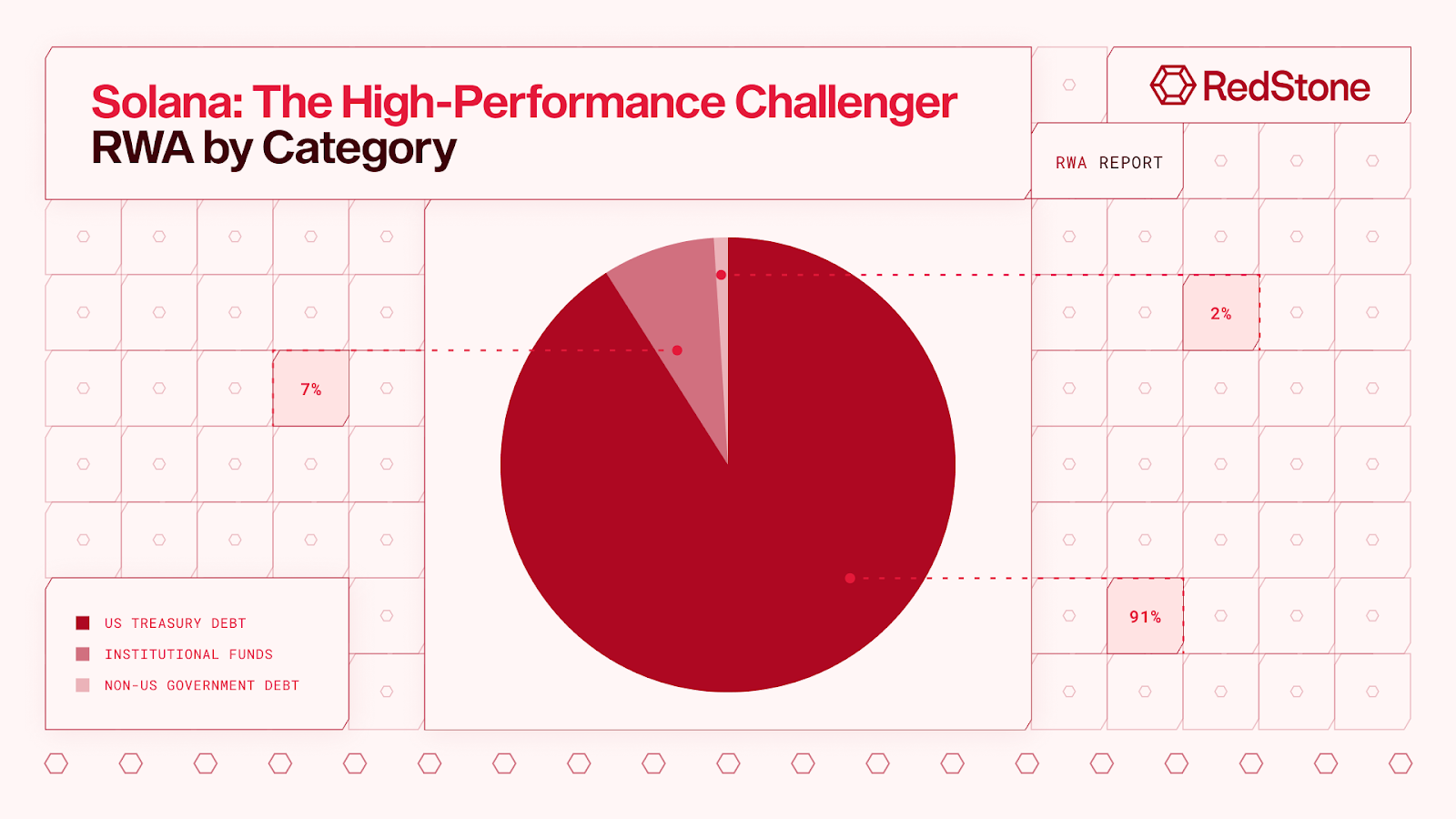

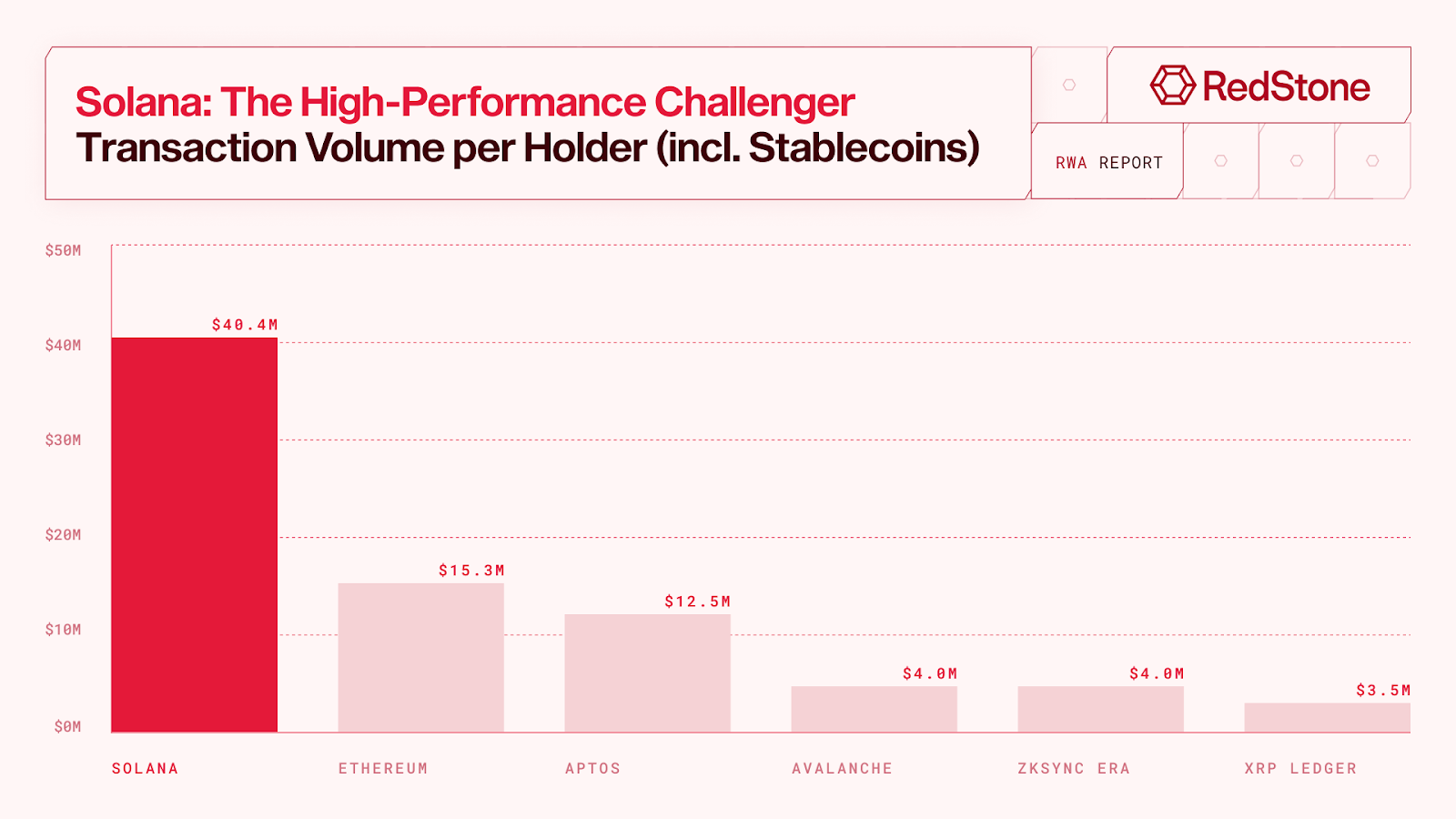

Solana: The High-Performance Challenger

Source: RWA.xyz

Solana reemerged in 2024 as a serious contender in the tokenized asset space, leveraging its high-speed architecture and near-zero transaction fees to support use cases requiring fast settlement and high throughput. While a later entrant than Ethereum, Solana currently houses $351 million of tokenized assets and has gained momentum through key institutional partnerships, most notably Ondo Finance’s tokenized Treasury products (USDY and OUSG, totaling $254 million) and Apollo Global Management’s ACRED fund, the firm’s first onchain offering.

This institutional traction reflects the Solana Foundation’s agile, coordinated structure, which aligns core developers, leadership, and ecosystem partners under unified strategic initiatives. In contrast to Ethereum’s decentralized but diffuse business development, Solana’s cohesive strategy was on full display at the Accelerate conference in NYC, where it showcased a clear vision for institutional-grade RWAs. With its focused execution and high-throughput design, Solana is well positioned for high-frequency, payment-oriented, and tradable RWA products.

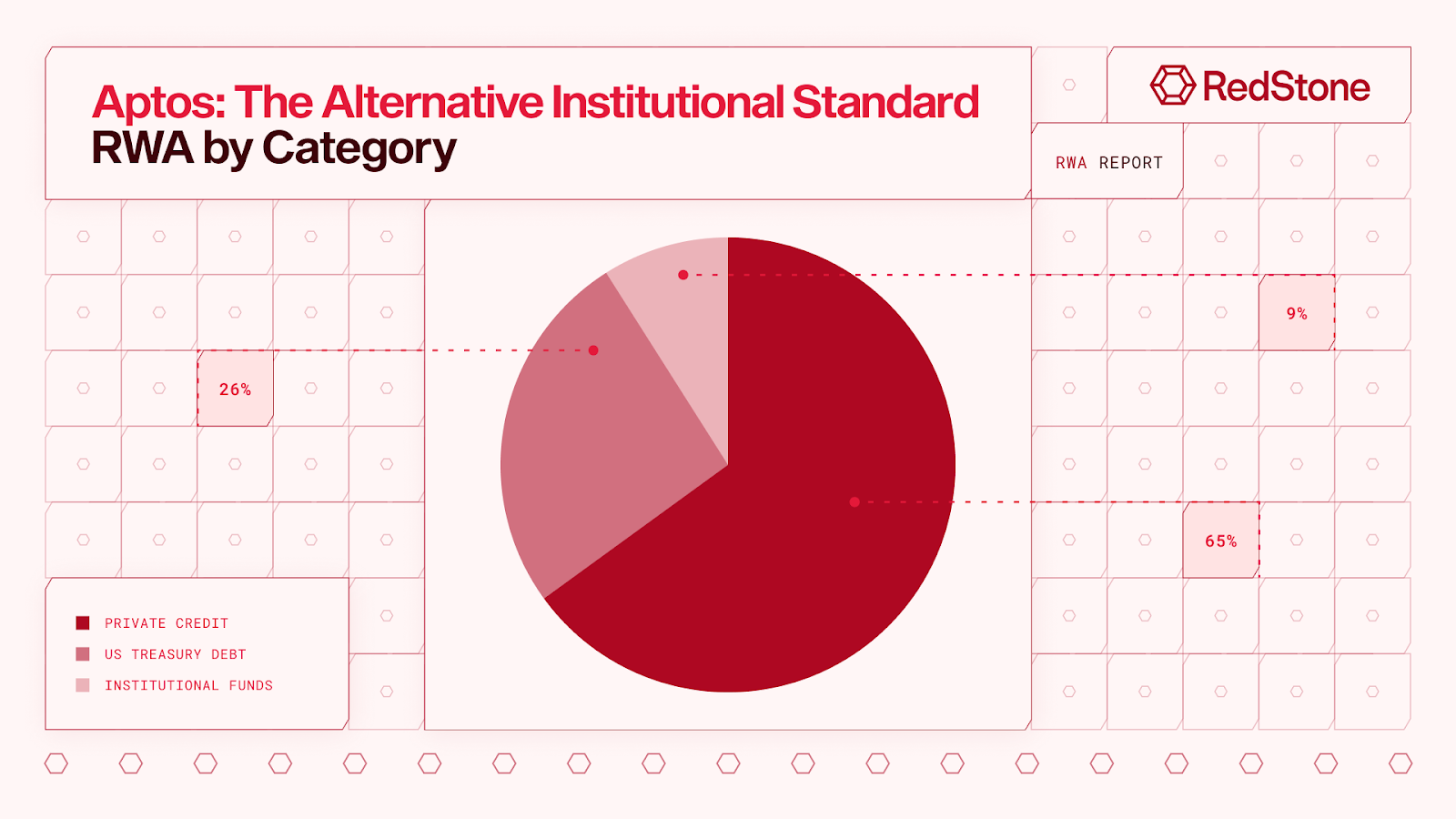

Aptos: The Alternative Institutional Standard

Source: RWA.xyz

Aptos has quickly emerged as another non-EVM blockchain for institutional RWA deployment, hosting $349 million in tokenized assets despite launching in late 2022. Born from Meta’s discontinued Diem project, Aptos leverages the Move programming language to appeal to institutions seeking performance and safety beyond Ethereum. In November 2024, BlackRock selected Aptos as the first non-EVM network for its BUIDL fund, citing lower fees and strong technical infrastructure. Other major issuers like PACT Protocol have followed suit, launching its emerging markets private credit portfolio on Aptos, drawn by its high throughput, low latency, and native stablecoin support.

Aptos’s strategy centers on targeting fewer, high-impact partnerships that bring significant value onchain. By emphasizing institutional alignment and offering a technically robust, cost-effective alternative to Ethereum, Aptos positions itself as a compelling alternative for developers and asset managers looking to escape the limitations of EVM-based networks.

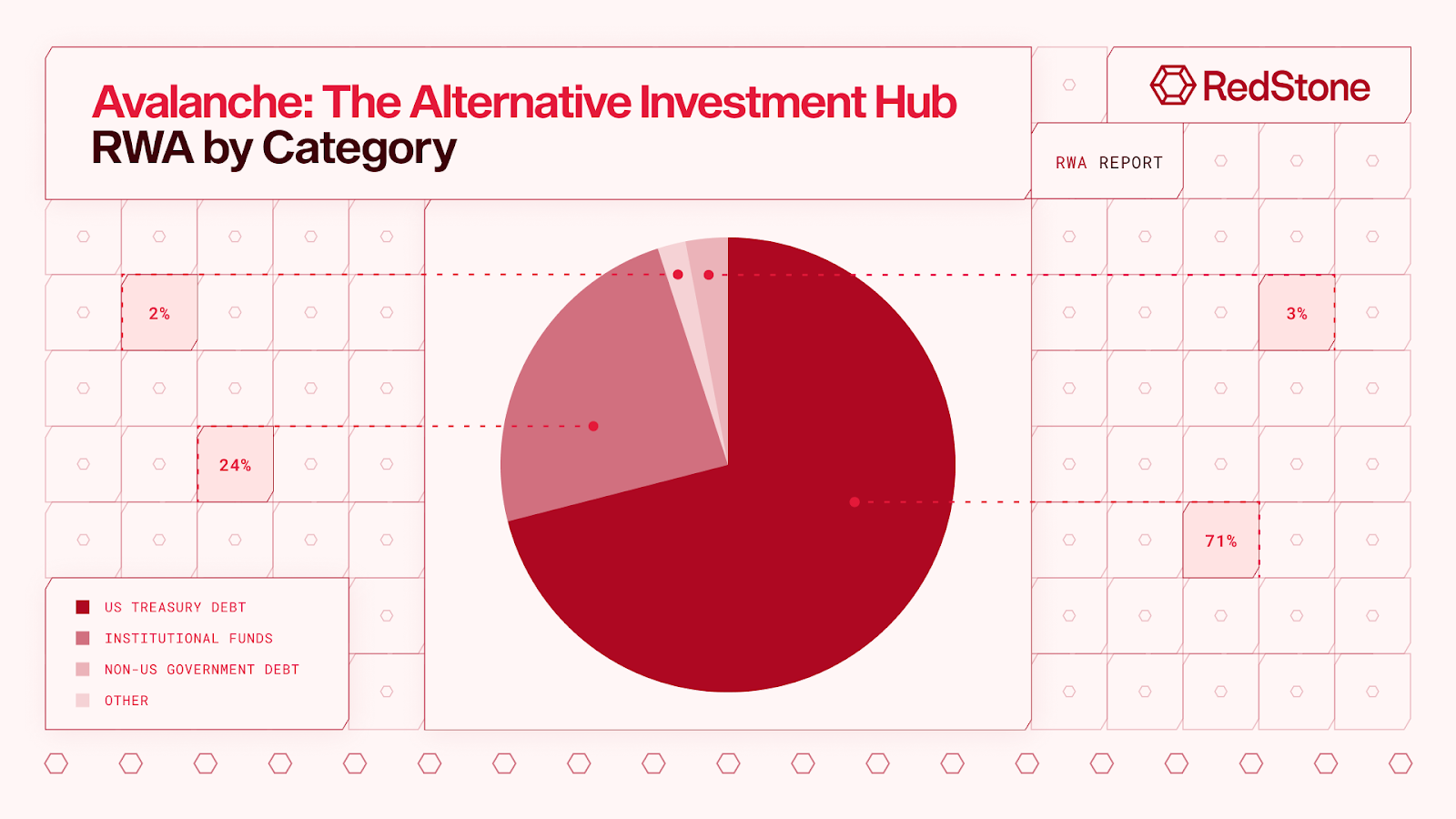

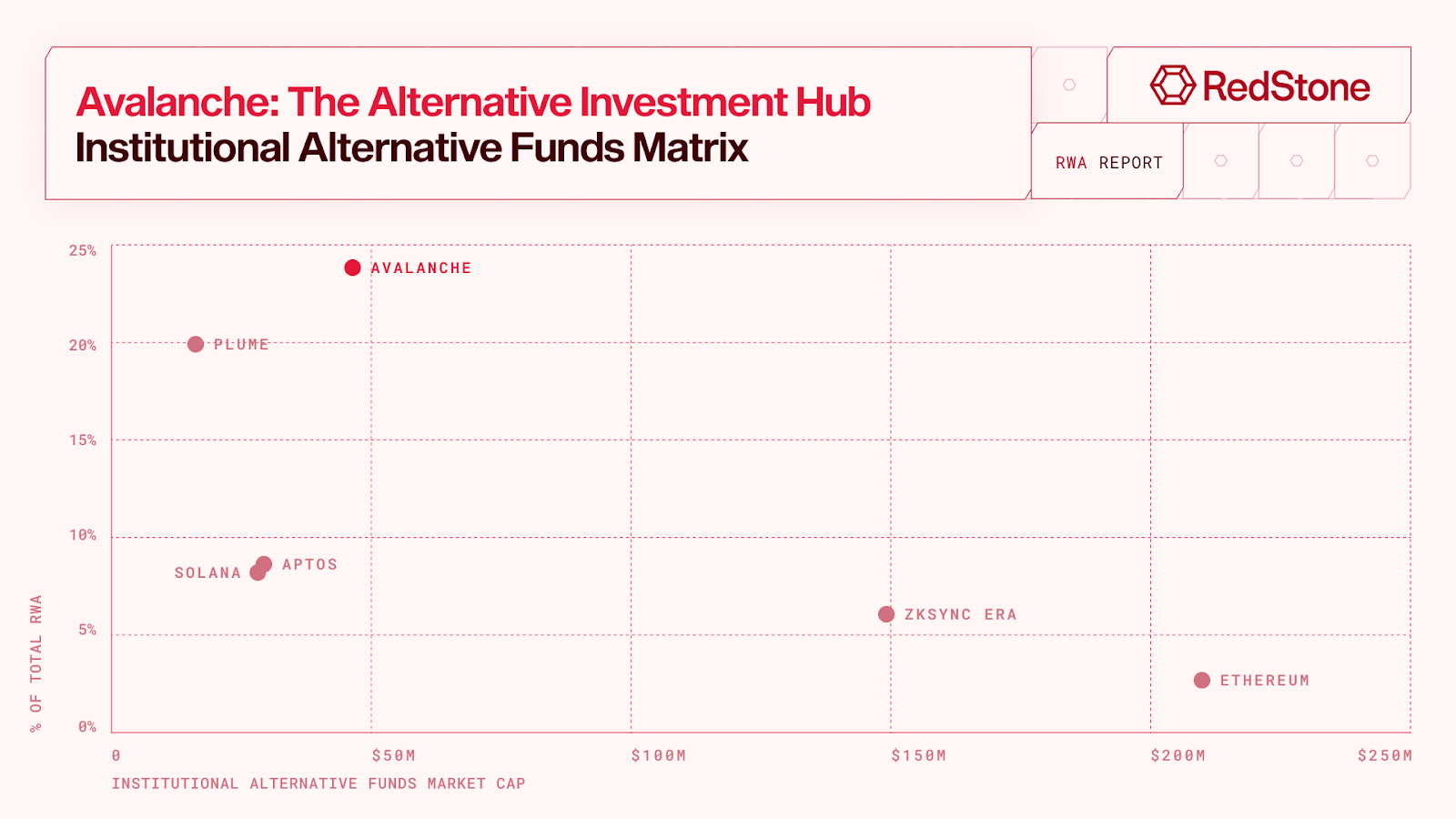

Avalanche: The Alternative Investment Hub

Source: RWA.xyz

Avalanche has positioned itself as a leading enterprise-grade blockchain through its unique subnet architecture, allowing institutions to deploy custom, interoperable blockchains tailored to specific regulatory or operational requirements, while still accessing broader DeFi liquidity. With $188 million in tokenized assets, Avalanche has attracted early, high-profile deployments such as KKR’s tokenized fund, one of the first major security token cases. These compliant subnets offer a compelling mix of regulated asset support, EVM compatibility, and fast finality, positioning Avalanche as a practical bridge between legacy finance and onchain execution, backed by a business development team deeply connected to institutional players.

Avalanche’s vision is that future investment funds will launch within regulated subnets, gaining compliance and control before connecting to global liquidity. By offering a middle ground between full decentralization and enterprise customization, Avalanche aims to become the institutional blockchain of choice. Its long-term success, however, hinges on sustaining institutional adoption and demonstrating clear advantages over traditional infrastructure through superior distribution, efficiency, and flexibility.

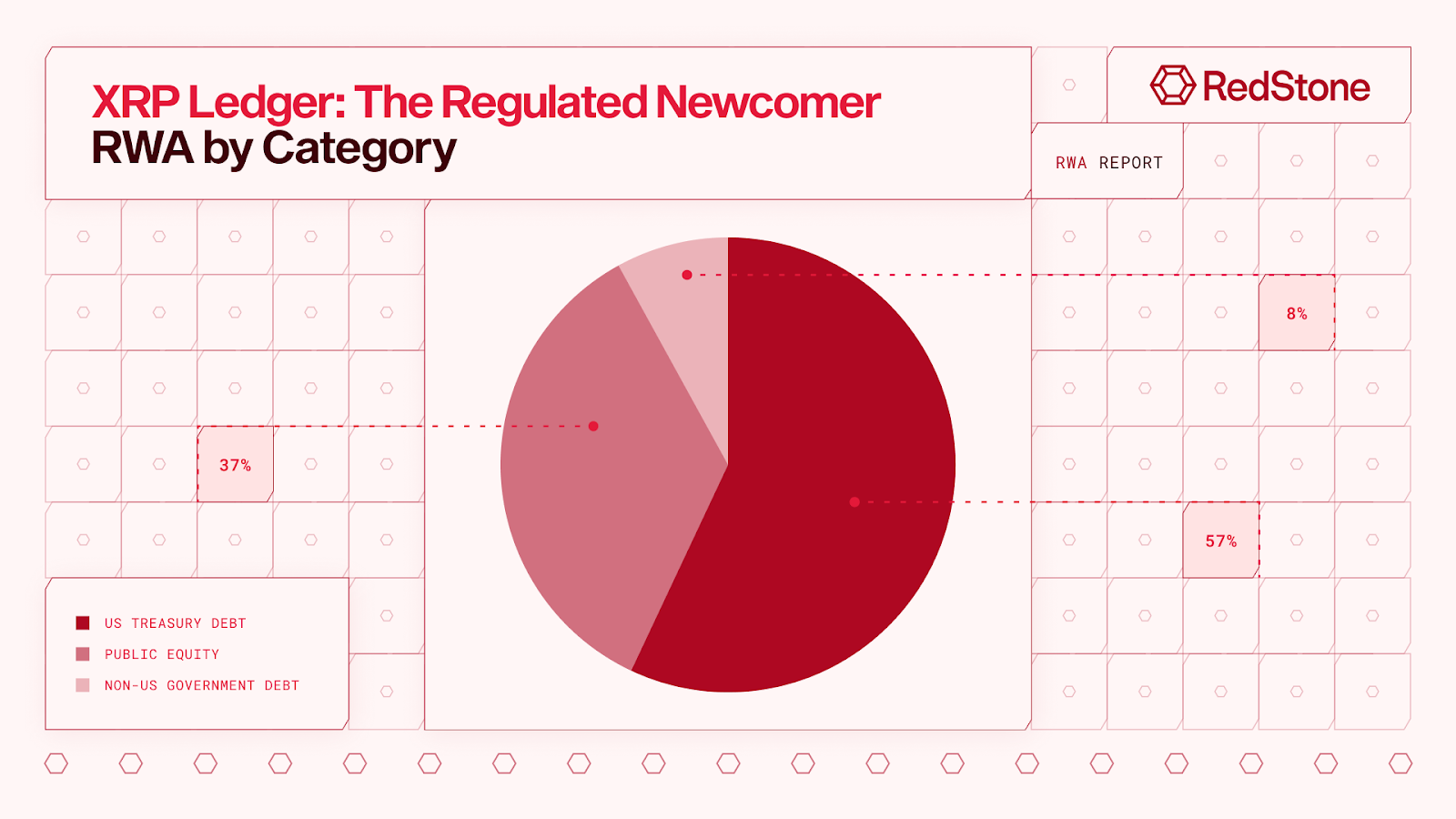

XRP Ledger: The Regulated Newcomer

Source: RWA.xyz

The XRP Ledger, one of the longest-running blockchain networks (launched in 2012), has recently emerged as a specialized platform for real-world assets, leveraging its track record of reliability and built-in compliance features. With $157 million in tokenized assets, it has attracted institutional partnerships such as Archax’s tokenized money market funds and the NYDFS-regulated RLUSD stablecoin. XRPL’s native features, such as issuer-enforced account whitelisting, token freezing, and protocol-level compliance, eliminate the need for complex smart contracts, offering institutions a streamlined path to KYC/AML enforcement and investor eligibility controls.

These capabilities helped secure its selection by the Dubai Land Department for the May 2025 launch of Prypco Mint, a platform that directly tokenizes property title deeds. While its institutional focus and deep resources position it well to compete in the RWA space, long-term success will depend on expanding developer adoption beyond its non-EVM ecosystem and unlocking broader engagement from its strong retail user base.

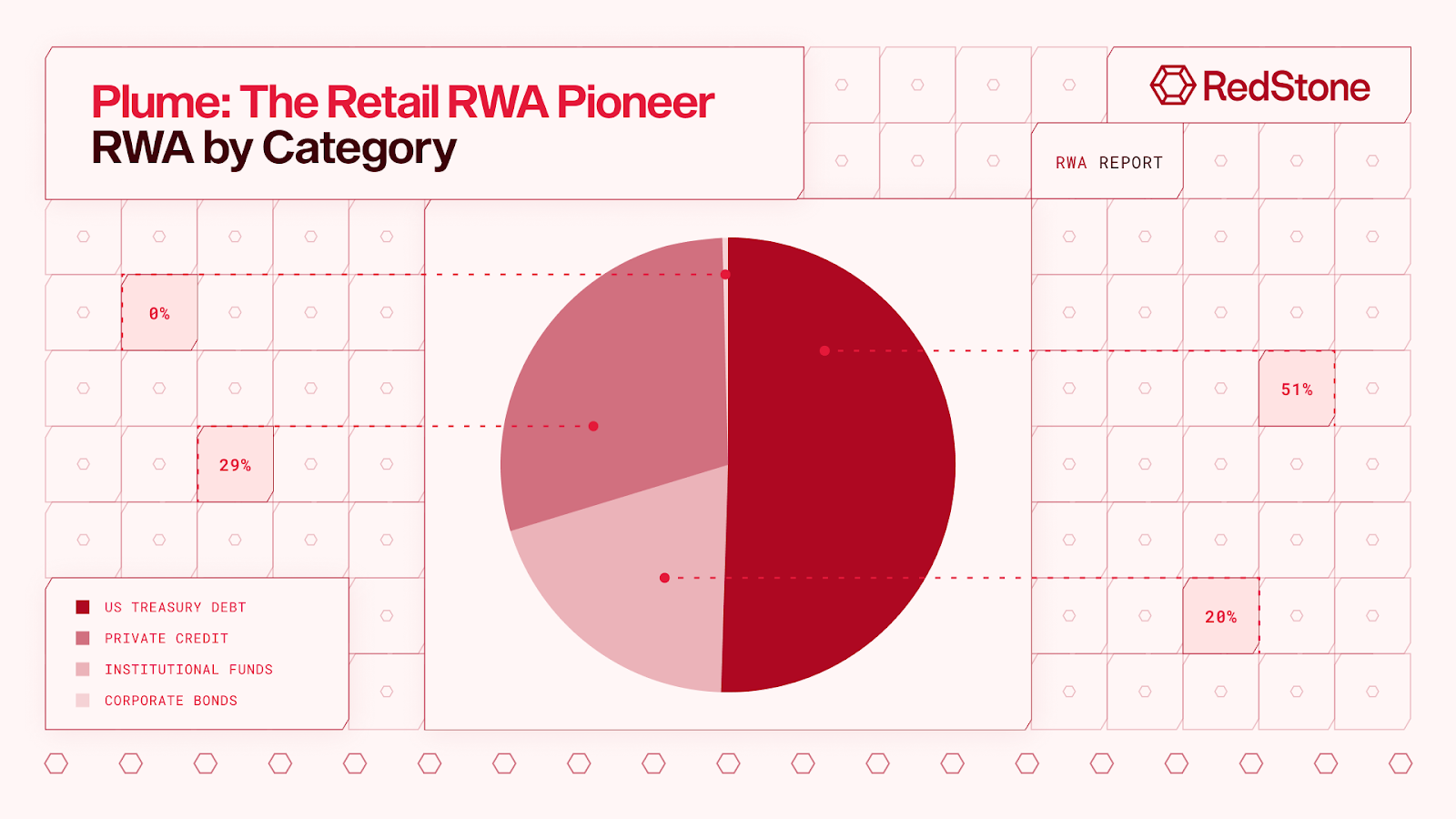

Plume: The Retail RWA Pioneer

Source: RWA.xyz

Launched in May 2025, Plume Network is a purpose-built Layer-1 chain designed specifically for real-world asset finance (RWAfi). While its $84 million in tokenized assets remains modest in absolute terms, Plume has quickly gained traction through a blend of institutional partnerships, including Blackstone and Invesco, and notable retail adoption. Through its flagship protocol, Nest Credit, Plume enables RWAs to behave like native crypto assets. By pairing blended RWA exposures with stablecoin pools accessible to retail participants, this structure allows users to lend, borrow, and trade traditionally illiquid assets while earning yield. This approach significantly expands both utility and liquidity, bringing private markets closer to the average crypto user.

Plume’s most distinctive feature is SkyLink, a cross-chain yield solution that streams RWA returns directly to user wallets across multiple blockchains. By addressing the fragmentation of tokenized assets across networks, SkyLink transforms RWAs into interoperable “money legos”,. If Plume can continue onboarding institutional originators while sustaining retail momentum, it could establish itself as the specialized liquidity layer for RWAs, complementing the broader multi-chain tokenization ecosystem.

This section has been authored by rwa.xyz, industry-standard data platform for tokenized real-world assets (RWAs).

6. Under the Radar: Chains With Institutional Backing

In the previous section, we evaluated public chains based on quantitative RWA activity data. However, there are chains where this data is either not widely accessible or platforms are in very early or permissioned stages of their onchain adoption. These networks are still extremely important to evaluate, since they represent some of the most significant institutional capital allocation in blockchain infrastructure, operating largely outside typical public visibility. The majority of these institutional platforms prioritize regulatory compliance, privacy controls, and seamless integration with traditional financial infrastructure as core design principles. Understanding their technical architectures and go-to-market strategies reveals the full picture of how major financial institutions are actually adopting blockchain technology, whether through fully private networks, hybrid permissioned models, or public chains with institutional-grade features that don’t generate easily trackable RWA metrics but handle substantial institutional adoption.

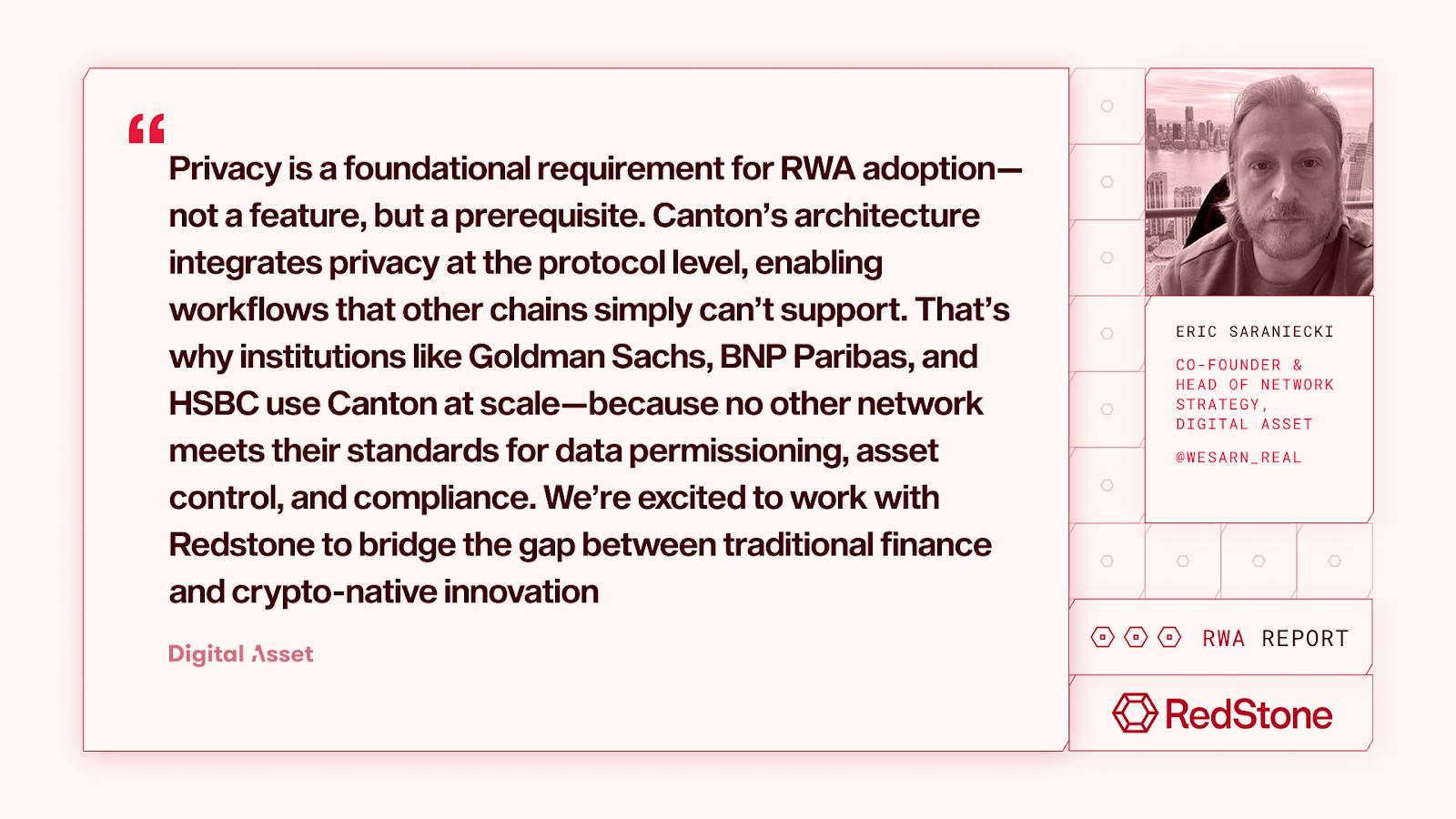

Canton Network: The Silent Giant of Institutional Finance

Canton Network has quietly assembled the most impressive coalition of financial institutions in blockchain history, processing over $4 trillion in tokenized assets and handling $2 trillion monthly in tokenized U.S. Treasury repurchase agreements (UST repo) volume – figures that dwarf most public blockchain ecosystems yet remain largely invisible to retail markets. The Canton Network represents the live production implementation of Digital Asset’s Canton protocol, which serves as the underlying blockchain interoperability framework that enables a privacy-preserving network of networks. Digital Asset, the financial technology company and primary contributor to both the Daml smart contract language and Canton protocol, has positioned itself as the primary technology provider for institutional blockchain infrastructure, working directly with major banks and financial institutions to deploy production-grade distributed ledger solutions. Over 50 major buy and sell side institutions are actively connected on the network, with HSBC Orion, Goldman Sachs GS DAP, BNP Paribas Neobonds, and Broadridge’s DLR running as live production systems. Indeed, since 2022, over half of all digital bond issuances were executed on Canton applications.