It’s been a while since I’ve opened a doc with no idea about what to write about. But the truth is that I miss free writing. Unfortunately, I do it seldom these days. So for now I’ve sat a timer on 1 hour, and whatever comes to mind during this hour will be published. No internet connection, no stimuli, just a blank screen and 1 hour (when you read the headline for this post now, it was actually the last thing that was decided. I didn’t know I was going to write about it).

The current market

Crypto has been rough lately with slow bleeding of altcoins for the last 3 months + $BTC going nowhere. In my opinion this will last for the whole summer, before we eventually start with up only August led by the $ETH ETF, president election preparations and rate cuts. But don’t take my word for it.

So what have I’ve been doing lately? Besides holding ETH, using Pendle and Gearbox for some yield farming and signing a lot of angel deals, I haven’t done much tbh. Trading has been ridiculosuly hard, and whatever airdrop coming to the market has been a sell (with a few exceptions, eg. $ENA up around 50% from TGE). This is a new environment. I’ve already written several newsletter posts about low float, high FDV tokens (you can read them here and here). From launching tokens in 2021 and 2022 which had some form of a price action after TGE (good for traders), this has been almost vanished for tokens launched in the last year. The price action for these tokens happened in the private phase as Cobie wrote about in his latest Substack. So unless you’re a founder, VC, angel, degen with connections to these people or KOL, chances are that this bull market has been incredibly hard for you. Yes, there are exceptions: October 2023 to March 2024 was in general a good period + if you were early to new meme coins. But other than that, most people will agree that this has been their hardest bull run by far. What’s interesting about this is that the old OGs haven’t had their usual advantage. Think about Hsaka for example. While he is definitely a key player still, we mostly see him when the market is in easy mode. The same is true for Ansem, he seems to have lost the plot. But can we really blame him though? After all, we are responsible for what we buy, when we sell or what we trade. Yes, influencers create FOMO, but we’re the ones that is taking the decisions on what we do with our money.

While I spent most of the time in 2023 and early 2024 glued to different trading terminals (PvP terminal, Tweetdeck/X Pro, Telgram alpha chats), I’ve now had a much more slow approach to the market lately. Basically because it has been more or less impossible to trade in any direction other than scalping (exception with the rumor of ETH ETF som weeks ago). This reminds me of the period after the Terra crash in May 2022. There was nothing to do, and you were forced to touch grass. While I see some similarities, I think DeFi is on its way up again. While I’ve been waiting for classic DeFi to return, it seems like points farming and airdrop hunting are the new kind of DeFi. The APR is collected in the private phases or the point phases. Eg. Ethena where you could lock USDe 3 months in advance and get your yield in terms of an airdrop later on. Few at that time knew how insanely popular Ethena would become. I wish I’d play it better, but there is a new protocol which gives me some kind of a similar vibe (Usual - a stablecoin protocol). They’re doing a private phase now with similar high APR. The question is if they manage to time it to the market equally good as Ethena (their airdrop is scheduled for October).

Stablecoins

While we’re talking about stablecoins, I still think this is the most important use case for crypto. The opportunity to store money in your own wallet, completely offline, and with the ability to send it to anyone within seconds no matter where they live in the world. We have stablecoins now with yield (Ethena, Open Eden, Usual, add more). While there is a discussion about how stable/reliable this yield is, we have definitely come further than with UST (Terra). Open Eden is for example a stablecoin protocol that is backed by T-bills (nets approx. 5% APR). Terra UST was sitting at 20bn at the top last run, Ethena is only at 3bn. Excited to see how big it can become, and/or if some of the others can challenge it. My absolute dream would be that after this bull run (in the deepest of the next bear), we’ve had some kind of a stablecoin that has become as “safe” as USDT/USDC and that it gave some kind of yield which was sustainable (5%?) as a minimum. There is definitely a market for this, just think about Wall Street and all the bonds that people hold in their portfolios. Step 1 is to make this 100% safe though (hopefully with the help from Larry Fink and Blackrock).

Other things I am excited for this run is EigenLayer, Pendle, Gearbox, Hivemapper and sportsbetting/prediction market protocols. One thing I do miss is the crazy yield farms from the last run. Eg. $TOMB on Fantom. Absolutely degen, high risk stuff. And while we do have degen stuff like this still, the TVL on these protocols are not high and the popularity is low. In general I am interested in backing more projects who do innovative stuff, because I am unsure of how many new forks of Pendle and EigenLayer we need tbh. I am also thinking more and more about launching my own project. This is still very much in the idea phase and if you’re a dev, consider reaching out.

Since the market has been slower lately, I’ve also had some more time to read books. I posted a picture of some books I’ve been reading lately.

Mostly it is books about philosophy, economy, and life hacks. I also want to read some books about venture capital as this is a field I’ve gradually entered into over the last year and a half.

Some basics about venture capital

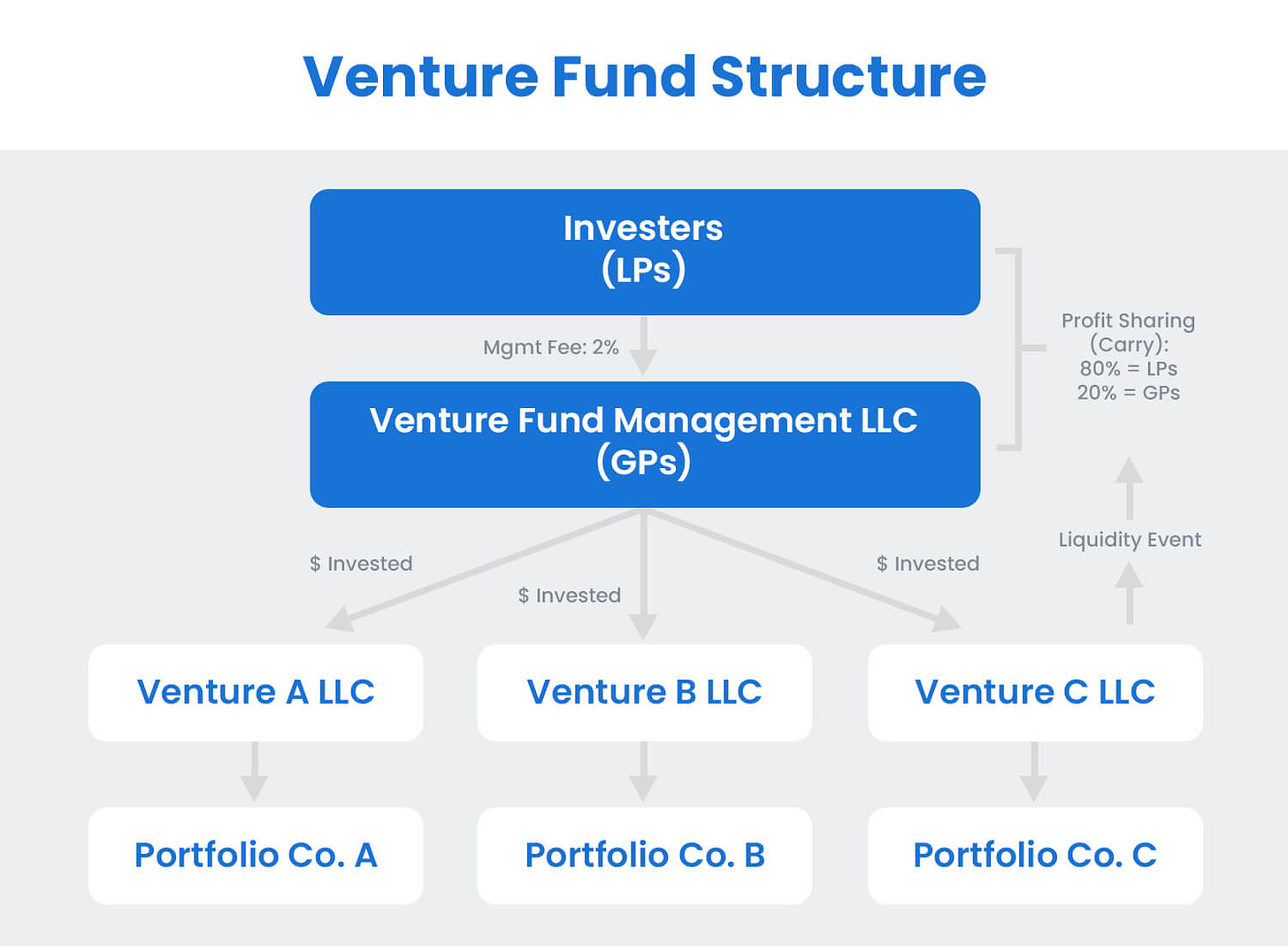

When pitching to investors, there are a couple of key terms to understand when it comes to a venture fund structure.

Look at the picture below and we will go through it in the following text.

A VC fund is a sum of money, that is used as the main investment vehicle for investing in startups. This capital, often referred to as “dry powder,” is meant to be deployed into startups.

Each fund is structured as a limited partnership governed by partnership agreement contracts usually over the span of 7-10 years.

The goal of the fund throughout that time period is singular: make money. Venture funds make money in 2 ways:

1. Carried interest on the fund’s return (about 20%)

2. Management fee (usually about 2%)

This is why you probably heard about people talking about the 2/20 model (well know you know what it is too).

The management company, or VC firm, conducts the actual business of the venture fund. It is not the same as the venture fund. The management company is the operations and people behind the fund. It serves as the business entity that is created by the firms’ general partners.

The management company uses the management fee it receives to pay overhead related to the venture firm’s operations such as rent, salaries of employees etc. Management companies receive the management fee to help deploy and grow their funds.

VC managers carry interest only after the Limited Partners have been paid.

A GP is the partner of the management company. Another way to define GP is someone who manages/oversees the venture fund. GP can be a partner at a large VC firm or an individual investor.

GP’s raise and manage venture funds, make investment decisions, analyze potential deals, hire on behalf of the fund, help their portfolio companies exit, and make the final call on what to do with the money they manage. Overall, a GP’s role narrows down to two key responsibilities: investing capital in high-quality companies and raising future capital.

GPs are paid from carry interest and management fees. For example, if carried interest is 20%, this means that 20% of a funds profits will be paid to the GP.

Where does the actual capital for a venture fund come from? This is where Limited Partners come in. They are the money behind the venture fund. Typically, LPs are institutional investors such as:

- University endowments

- Pension funds

- Sovereign funds

- Insurance companies

- Foundations

- Family offices

- High net worth individuals

The bread and butter of the venture fund structure is of course the portfolio companies. These startups receive financing from the venture fund in exchange for shares of preferred equity.

It depends on the individual fund, but to receive VC financing, portfolio companies must meet certain standards or requirements. Things like:

- They should operate in a large market

- Have product market fit

- Have a great product that customers love

- They must show promising economics and the ability to create a sizeable return for their investors

Here is a list of the biggest crypto VC companies:

https://coinlaunch.space/funds/venture/?per-page=50&page=1

Angel investing

On the other hand you have angel investing which usually means investing at earlier stages than VC + angels operate alone and therefore write smaller checks than VC companies. Angel investing is simply the act of investing in early stage companies. This usually happens at the “pre-seed” or “seed” stage of a business, meaning before a product or service has been built, or early in its life cycle. Angel investing is high risk because most companies fail, but it also offers high upside in the event a company ends up succeeding.

What I love about this space in general is that you can be a nobody, and after 1-3 year you can be one of the more important voices in the space if you put in the time, effort and consistency. The space is so new that even if you don’t have a degree from an elite university, you can become an expert in this field. It’s all about trial, error and curiosity.

So how did I start angel investing myself?

To answer this question we need to go back to where it all started. Before I got into crypto I was a stock market “bro” and my Twitter that I created in January 2019 was mostly focusing on this + life maxxing. Before Twitter I had a blog where I talked about investing, and I’ve also written a couple of newsletters (which I have now deleted). For me being full-time in crypto started in 2021 some months after I quit my 9-5. In the start I was just apeing NFTs, DeFi farms and random shitcoins on Binance. But after writing threads and thoughts about DeFi protocols for a while I was starting to get offered deal flow. In the start I simply rejected these deals because I felt inexperienced, but I gradually learned that there was many people who knew way less than me, that already was in the game.

As you know I am a KOL/influencer (hate the name, but it is what it is). And with a relatively large audience on Twitter (300k followers) and on Substack (30k subscribers), founders of projects reached out to me asking me if I wanted to invest in them, often with no strings attached. However, there is a gentleman’s rule that you should post something about the project, which makes 100% sense. The project gets exposure —> people get interested —> more people buy → price increases. Pretty self explaining really.

With that said I think this cycle has had more KOL rounds as well due to the fact that many founders feels that the VCs doesn’t contribute much. Yes, they have the network, but most often not a big audience. KOLs on the other hand has a huge audience and very often a solid network too. As a consequence many VCs have pivoted into semi-KOLs too so they can eat more of the cake. I don’t blame them tbh.

So basically what I have done is following my natural curiosity and I have dipped my foot into several fields in the crypto/web3 space. I won’t call myself an expert in any field, rather an all-round person who knows a lot about several subjects. And if I don’t have an answer myself, I use my brilliant network in the space to find the answers. Many opportunities have presented themselves just by people reaching out to me after they vibed with something I wrote or tweeted. However I do think there are areas I have some kind of strength in. Within DeFi I’d say I am personally mostly interested in trading DEXes, stablecoin protocols, yield narratives (think EigenLayer/Pendle/Gearbox, Mellow, Symbiotic+++). I am also very fascinated by trading (both on CEX and on DEX). My dream is to have a competitor to Binance/Bybit, and therefore I also love working with teams that have this as a goal. I also have a strength in marketing/growth, and now what works or not as an influencer myself.

About deal flow, how do you get it?

You should either have some kind of expertise in a niche field within crypto, or a big brand. The best combination is to have both (obviously).

The reason people with large personal brands or audiences do well as angels is because companies want them on their side for credibility and distribution. There is signal power in having trusted folks aligned with your business and they can spread the word about your product or service.

Also, when founders send out their pitch decks, they can use your name on the deck to signal that this is a great investment. Let’s say you see a deck and Cobie is on the cap table, I’m pretty sure that most people would invest in that project blindly without doing any due diligence at all. After all, if it’s good enough for Cobie, it should be good enough for you, right?

What do I look for when I decide to go for a deal?

Well, there is no secret that timing is an important factor here. And the terms of the deal are crucial for me when I take a decision to invest or not. What kind of market are we in? What is the outlook for the next 3, 6 and 12 months? What about in the next 2-3 years? Vesting schedules can be long, so it’s important to think about this.

Is the team building something interesting that can get product market fit? Do you see it as something sustainable? Which narratives will it cover? Which VCs are coming in? After that I talk with my network of trusted people. Why did some of my VC friends pass? Or why didn’t they ape more? Which competitors are there? Thoughts of the TVL today and in the future? Will the protocol be left rekt after incentive programs are finished? All these are valid questions.

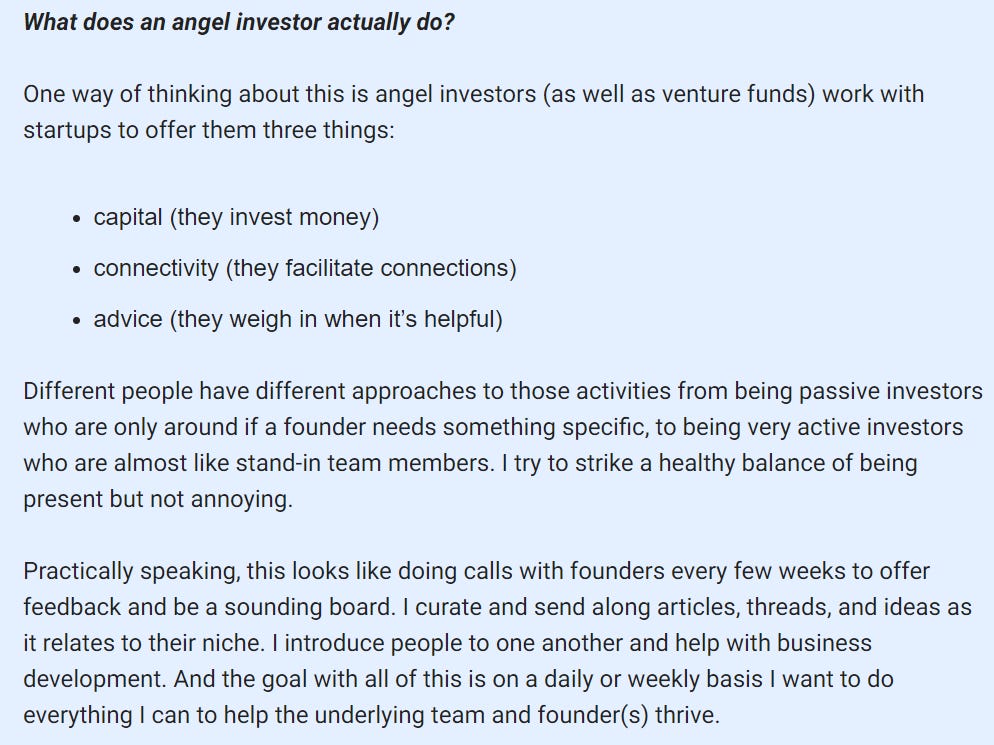

I already presented what a VC does, and briefly touched upon what angels do. Here is a longer explanation by Ben Roy:

And just to end this, here’s a snippet that I liked from a passage in @DCbuild3r latest article about angel investing.

"One key thing to notice is that social capital compounds just as much as your financial capital, if not more, and I believe that social capital is the biggest driver in professional success in any endeavor, whether sales, building technologies, doing research or philanthropy/volunteering.

It truly doesn't matter, having skilled friends in your networks who have other friends, they have capital, new insights, and wisdom, they are able to change things, and if you become friends, you can truly change the world together for the better".

…

That’s it for today, anon!

Hope you enjoyed this piece.